I’m not really sure why this is a COVID stock and not just a pure growth company? As others have mentioned, RH is positioning itself as a lifestyle brand. Covid has only increased the wealth gap between the middle class and upper middle class which RH caters towards. Think professionals who make well into the 6 fig range shop here. These same people have bought houses, received raises, and been able to jump around companies increasing their income. They’ve also benefitted greatly from a long bull run and now have a lot of buying power. It’s why home prices have gone up astronomically.

The financials also don’t look terrible, I’m not sure I would equate them to a PTON or DOCU.

Chart them comparing revenue and income, they do not compare. Financially and fundamentally they could not be more different. DOCU and ZM were great plays as their businesses and growth were directly affected by COVID. I just don’t see the same for RH. Wayfair isn’t exactly a perfect comparison to RH as RH caters towards luxury furniture whereas Wayfair caters to your average consumer. Williams Sonoma is a much better comparison. They just had an earnings call and the stock did drop in the weeks following, but you could argue that was due to overall market movement.

They are positioning themselves as the place to go and buy from for professionals making bank. Go look at their locations and check the housing prices in the area. They have either risen 30%-50% or were already in the $1M+ range. Think LVMH for furniture buying. As mentioned above they are also making moves into the hospitality space and design area. Personally, I would be bullish on this company given their recent moves, their consumer sentiment, and financials.

I would give, a possible good bear argument is they have had a frenzy of sales in the past 2 years due to pandemic home buying which has been slowing for the past couple of months. It won’t nearly be as bad as DOCU or ZM though.

I hope you guys make money, but this is too risky and expensive for me and does not have the right ingredients to properly define movement.

Williams Sonoma had their earnings AH on the 18th and their stock only dropped 1.5%. They are down 15% since then, but this could be overall market conditions.

For whatever it’s worth, I still have not re-entered this play however I do have cash on hand ready to do so. What I believe we’re seeing now is less waves, more parabolas. What gives me hope that this will reverse is the fairly high RSI that we’re also seeing at this level.

Should this continue to rise to the $600 level as I previously noted, though, we have two possible outcomes:

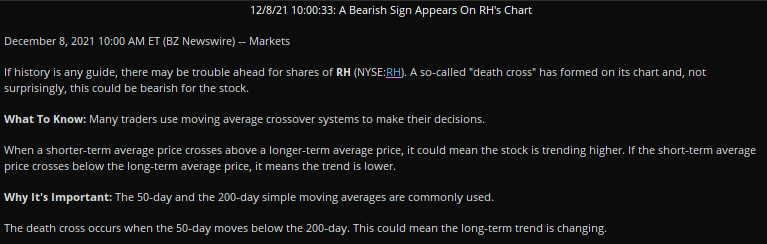

Double top just in time for earnings followed by what we’re hoping for - a monumental correction to pre-COVID levels

Double top just in time for earnings followed by what we’re not hoping for which triggers a cup and handle

One of the lessons learned from previous earnings is that holding positions through the earnings call itself is risky. My only caution to everyone is to make sure you manage risk by managing your position sizes and not overexposing yourselves.

Hindsight showed that DOCU had clear sell volume shortly before earnings were announced. I would watch volume as much as possible heading into earnings to try to feel out the room within the last 15 minutes of trading before earnings:

Edit: Additional research and clarification. I am watching both the 587 resistance established November 30th that it has already been rejected off of, and the December 1st 600 resistance level it has not yet hit. This may double top off of 587 today.

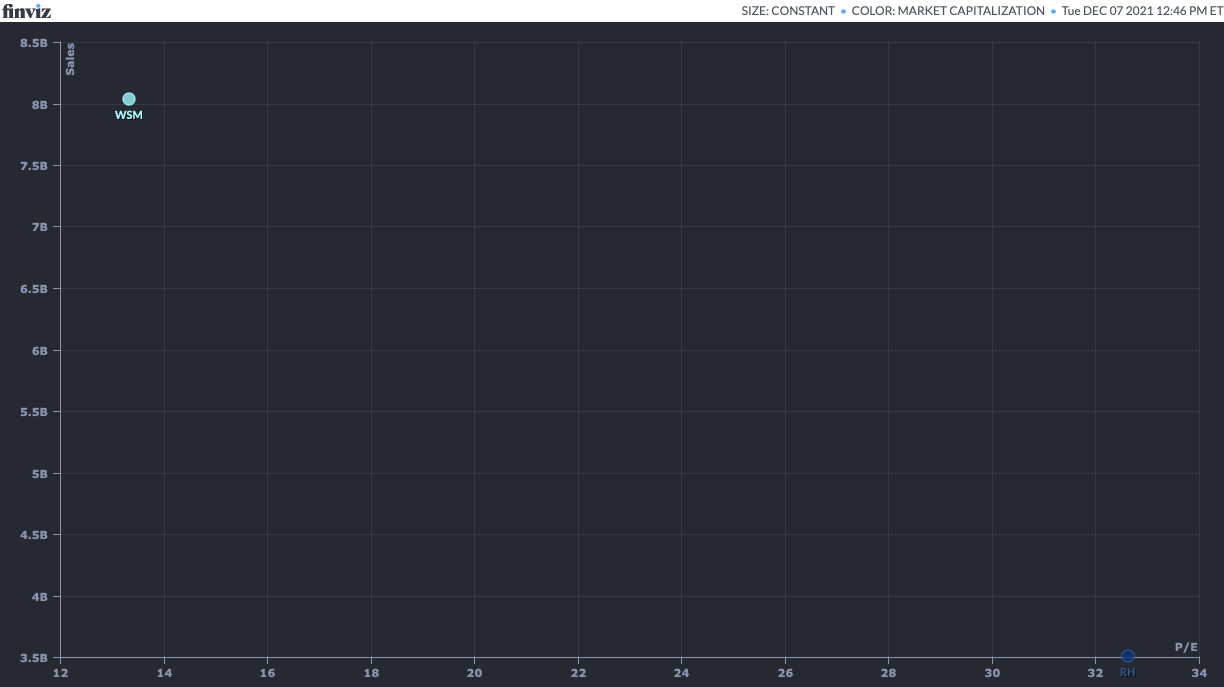

WSM, which I agree is the best comparison for RH, trades at 12 P/E while RH is trading at 32. Both have a 13B market capitalization while RH has half the sales.

As with all these plays though, it’s not really about how they’re doing. DOCU beat earnings by a lot. It’s more about correcting their valuation. WSM did not receive the same COVID pump that RH did for whatever reason. If it had, we would’ve had the same discussion about them.

All in all, I’m not bearish on RH as a company, I’m bearish on their stock because it’s trading for more than it’s worth to a significant degree. But, as with everything, this is just what we think. The market may have other plans.

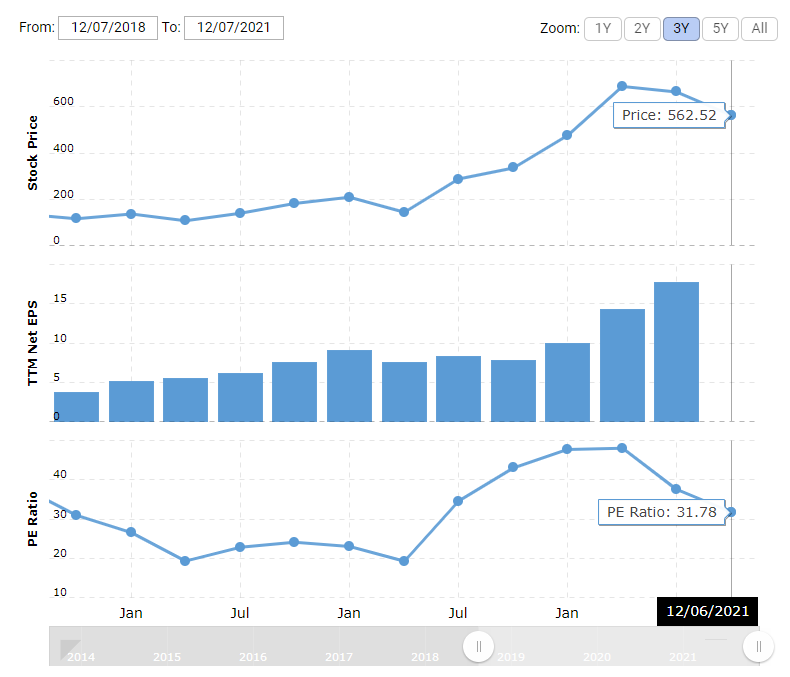

Looking at it again, I think there could be room for it drop, but looking at RH historically, it’s always had a high PE ratio compared to its industry, I’m not sure what would change now:

It does seem like a correction could take place, but I feel as the markets are forward looking, investors may be excited about the moves RH is making to justify its valuation. I mean we have Tesla for gods sake.

Yeah, but do you really believe that RH has the same retard strength as TSLA? TSLA is hugely sentiment. I’m not sure that the same sentiment exists here.

I agree with this. Considering the fact that RH is mainly owned by institutions, positive and strong sentiment is not a good reason for me why RH would continue to maintain its valuation.

As we come up to the call, don’t forget that earnings plays are typically more profitable if you cut before the call and place the drop afterward. Earnings are a gamble. We’re trying to make an educated guess at direction, but we could be wrong. If you have profit that is meaningful to you, cut it and live to trade another day.

I will be holding a gamble size through earnings and will be in VC for the results.

Plays like this are why I always state the above. Take profit because earnings are a gamble.

The Bad

They did end up beating EPS estimates and revenue and increased the lower end of their guidance. They announced growth and didn’t really talk about a whole lot of bad in the report. The markets initial reaction was to buy the stock and it’s now up 11% in AH.

The Good

This call was a shitshow. I’m not being dramatic, I’m not giving hopium, I’m being honest, this call is awful. If the goal were to convey that this company is in a place of strength, that was not only not conveyed at all, the exact opposite was communicated clearly. This is a company that has no clue what in the world it’s going to do to justify it’s current valuation. The CEO at one point said to not buy their stock, the most details he offered were about the trips he’d taken on the company yacht. Stores are not coming anytime soon, they don’t know what they’re naming their restaurants, no guidance at all, customer backlogs are still large and they insinuated that there is no “end” to the backlogs coming any time soon. They ended with the admission that they are behind on growth.

This company is owned in large part in 10% chunks by large institutions. I’m thinking at this point we may have a ZM scenario where they’ll die by analyst downgrades and selloffs possibly starting tomorrow. But we shall see.

The thesis of this play is correct. This company is overvalued and that was confirmed by the earnings report and call. Unfortunately the market did not correct it immediately upon earnings. I’ll be watching this play tomorrow as I don’t think that they’re out of the woods yet. Either way, there are more plays and more opportunities in the market and we march forward.

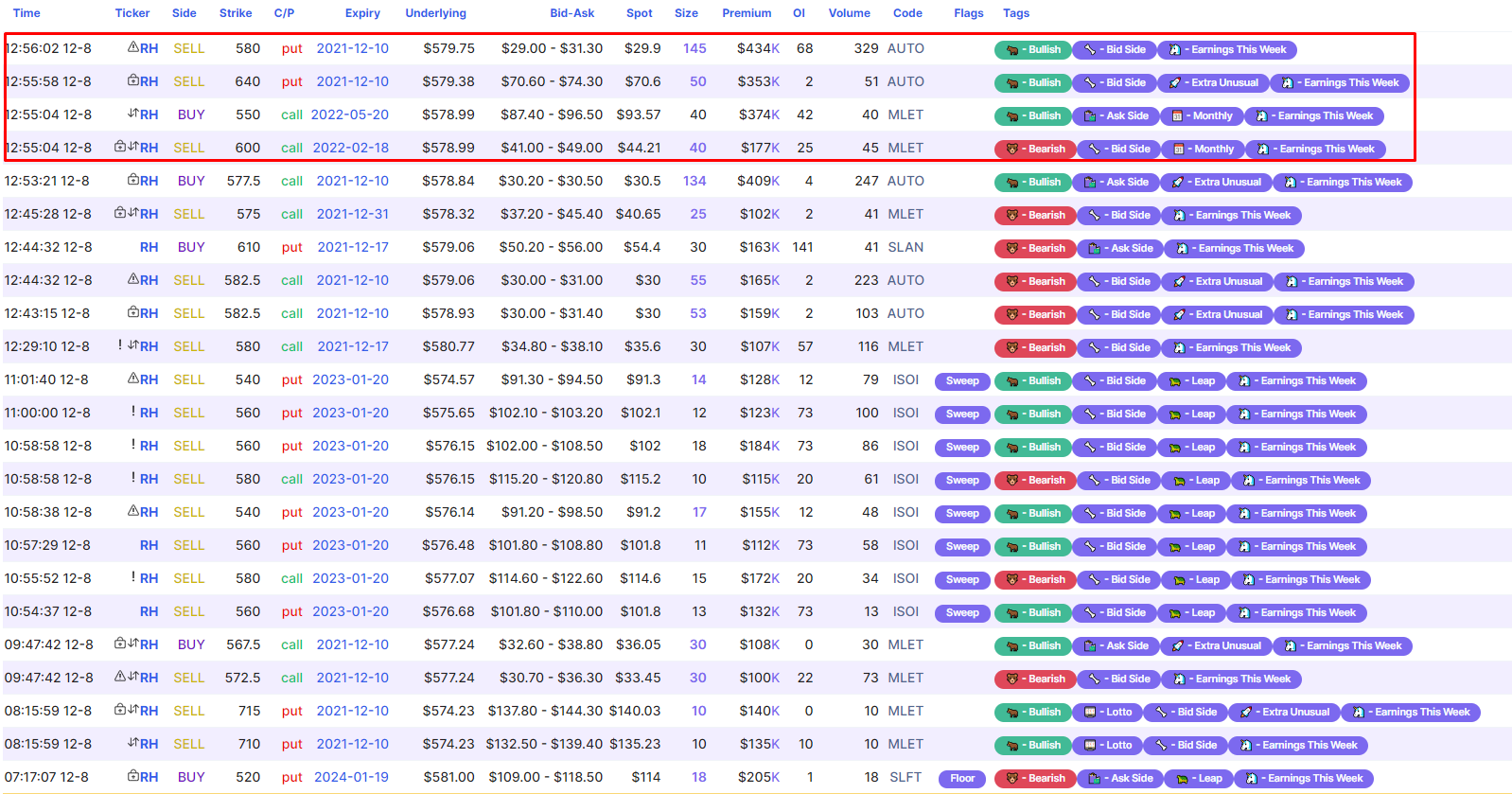

Someone in the Discord casually mentioned checking for flows right as market closes on ER day, as an attempt to spot insider trading. So on Unusual Whales around 5 min before close I set the filter to $100K+ premiums only and look what occurred in the final moments.

All option trades >$100K managed to fit in a single screenshot. I boxed in red the last 5 minutes. In the last 5 minutes were where the largest trades occurred and were dominantly bullish. Were these potentially trades made with insider info on the ER numbers?

FYI the ‘lock’ symbol at the left under the Ticker column means it is a confirmed BTO/STO order. No lock symbol means unknown whether they were to Open or Close.