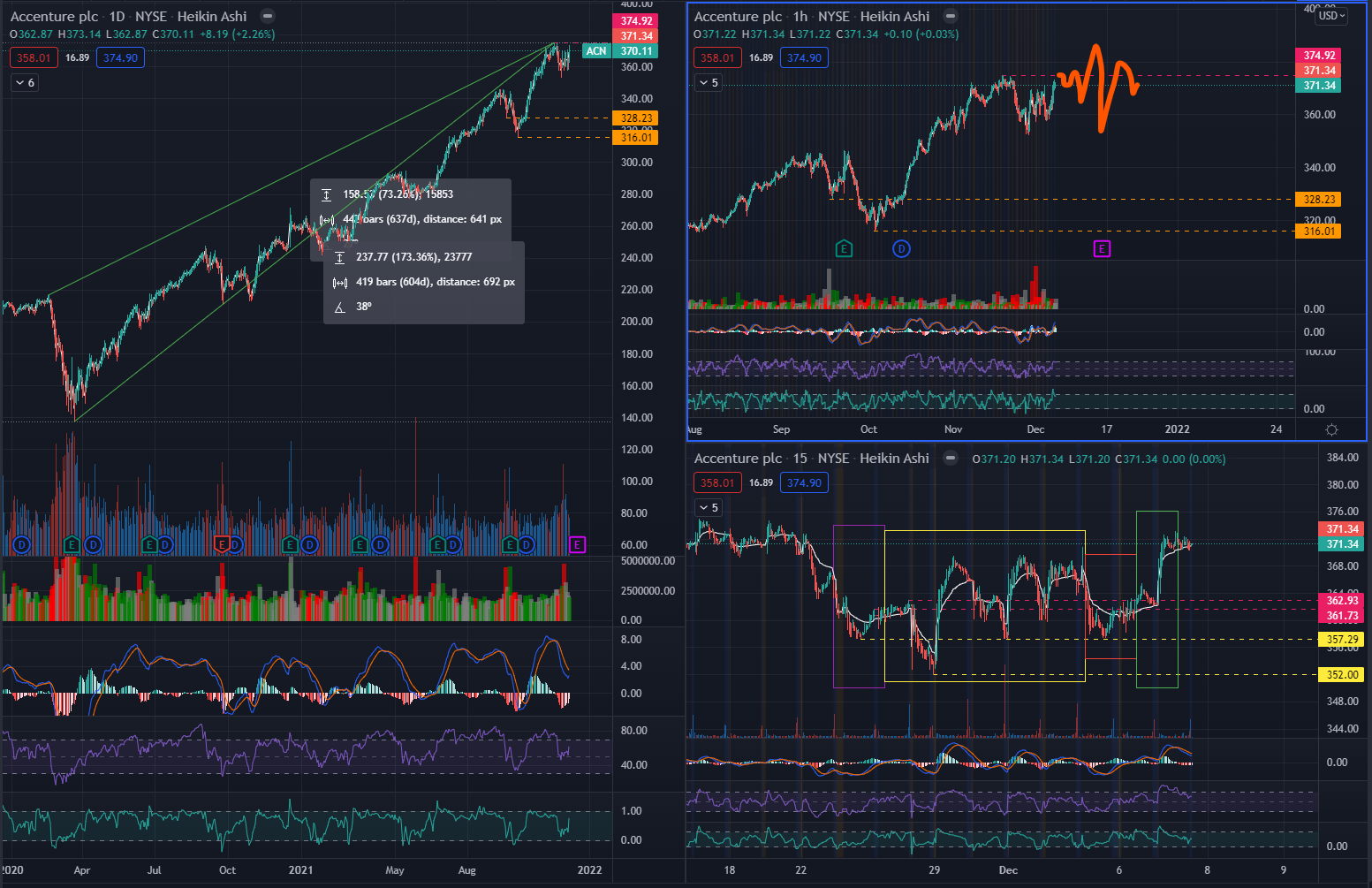

Quick 2 cents on why i’m slightly bearish on this play on the fundamentals, not technicals, of this play. Currently working at a major competitor of Accenture. Accenture likes to hire fresh-out-of-college (no disrespect, I started their too), however clients are beginning to want more mid-senior level consultants to work on their projects. There is a large shortage of these higher skilled/experienced consultants in the job market. My company is facing similar recruiting issues. Accenture also has a high turnover rate with these entry level consultants exiting near their 2nd year with the company. This is ultimately due to their below-market compensation plans.

To note, most consulting firms had their best year during COVID due to an increased demand for tech upgrades, ERP implementations, and overall revamping company strategies. Thus, professional and advisory service firms faced labor shortages to accommodate client demand. I cannot confidently say that this is one of those “hyper-inflated COVID stocks” (like DOCU, ZM, etc.). The industry is beginning to see a decline in the demand for entry level consultants when COVID-work from home was taking place. The shortage of experienced labor could lead to lower sales/revenue, clients often partner with smaller firms that offer a better price with more experienced consultants (Smaller firms are beginning to lure consultants away from larger firms with better compensation and benefits).

I doubt that Accenture can maintain their “stellar” growth that they’ve seen in the past year.

Like @SuckyMayor noted, Accenture is a major partner with Salesforce ($CRM) which has still yet to recover since it’s earnings report on 11/30.

Bull Case:

Accenture/Microsoft owned, Avanade, has $2b is sales with a 20% YoY growth since 2000. $MSFT killed earnings and is up nearly 9% since their earnings report.

The work from home has significantly reduced expenses and clients are no longer requiring on site consulting. This seems to be the norm since COVID and will likely continue to have reduced on-site client travel.

Also many tech offerings are being sold on a subscription based service. The investments in building/retaining long term customers may have long term growth potentials as it poses an increased reoccurring revenue stream for Accenture.

One direction consulting companies use to reduce costs while maintaining employee compensation is by hiring offshore workers. If the necessary layoffs were replaced by these offshore workers, this could further reduce employment costs while maintaining a high billable rate and keeping employee comps at competitive rates.

Will add to this more if I think of any points that are bearish/bullish.

Here are some links that may be useful for those looking to play this:

-

https://www.fishbowlapp.com/company/accenture

-Social media app that many consultants use. Can be used to track sentiment at Accenture (compensation topics, job questions, project talk, etc.)

-

COVID-19 impact: Accenture to lay off 25K employees, Indians set to lose jobs

-

https://www.glassdoor.com/Reviews/Accenture-Reviews-E4138.htm