I’ve seen APPH mentioned a lot in trading floor recently, so I decided to look into it. I currently do not have any position.

Today, APPH had a 26% run on the coattails of strong earnings and some leadership shakeups. I think there is room for this to go higher. I’m going to look for a dip and pick up a few calls.

The company is looking interesting and the ticker price is cheap and trading at all time lows. I don’t think this ticker will see $20 any time soon but it feels underpriced at $5 as well.

Thanks for getting this up. Apologies for everyone I had been bugging about checking this out in trading floor without a thread.

To add to this, this recent interview with the CEO on Bloomberg is a great overview of what 2022 is looking like. I’m in APPH long term, but for the short term the last few days - it’s been well to me. I’ve condensed the audio down to the important snippets and the general gist of the business.

Year round indoor farming facility in a controlled environment that is currently growing tomatoes - later this year they will diversify crops and expand into berries, leafy greens, salad greens, more varieties of tomatoes, etc. More farms, more crops to market and higher quality.

Currently aimed at east coast, mid-west and southeast grocers.

Largest CEA facilities on the planet (controlled environment agriculture) which doesn’t rely on questionable water tables, uses less land and rids the need of harmful pesticides and chemicals. Quality and reliability of crop in a controlled environment that is also not reliant on import issues. Current facility is the size of 50 football fields.

New facilities are aimed at opening later this year.

Current revenue targets are aimed at 300% growth 2021-2022.

2021 was first year of operation - no prior operating history but landed 1,000 grocery stores from Kroger, Walmart, Publix and Costco.

Uses 90% less water then an open field, with roughly 30x yield per acre. Runs on recycled rain water, in a water rich region based in eastern Kentucky. Not reliant on city water.

Produce can be moved to 70% of the U.S market and population with a single day transit, rather then days. No need to ship produce thousands of miles when it can be grown in controlled environments. Not reliant on geopolitical risks. (Based on current events I’d argue this is a big plus. Imagine being able to grow crops that would have needed other climates to achieve, but can now be done here)

Current discussions in place to potentially expand to additional nations. National footprint needs to be in place here first before that.

My initial positions were $4.5 calls March 4th. My current positions are $7 calls March 11th. I’m holding shares long term.

I’m sure the ticker could keep running on sentiment, I remember it gaining traction in Reddit a year or two ago.

But even at $5/share, that’s a ~$500M market cap on $9M Revenue for the year, with substantial losses. They could triple revenue and still be losing tons of money, and hearing they will be doubling staff means costs will be rising too.

Interesting company for sure, but this is a hot potato IMO.

Net sales of $24 to $32M vs. consensus of $39.15M, more than double the net sales from last year, Adj. EBITDA loss expectation is in the range of $70 to $80M, modestly higher than the $69.9M last year despite the expected quadrupling of the farm network and significant inflation.

I didn’t find the caveats particularly convincing - they explain weaker performance, but it’s still weaker performance.

Assuming that pre-earnings price action incorporated this information, and future guidance is lower than expected, I don’t understand how prices increase. Or are one or more things in @ChiefSloth’s list overwhelmingly positive and likely to happen that more than makes up for things?

By the way, is there a possibility of a Russia-related bump? There was an increase after the Feb 24 earnings but the real rise came in March, when talk of sanctions and export restrictions kicked in. Indoor farms may appeal to some as substitutes for whatever is being imported from Europe, and even Ukraine or Russia.

I think this one may be done and over with I do not trust the ortex numbers right now, as the cost to borrow has been decreasing and it’s risen a lot, I personally think some of the short interest was hedged and reset on Friday when it hit 6.67, then immediately dropped to 6.24. Just my opinion

I’ve been starting doing some research on vertical farming companies for a long term hold. This came up in my search. Glad to have found this thread.

I think vertical farming is the future. Less fertilizer, greater yield per acre. It loses on energy cost (no one has figured out how to tax sunlight, yet), but with the proliferation of renewable energy solutions maybe that disadvantage is shrinking? Big upfront cost but manageable. Food can be grown closer to market, reducing transportation costs and logistic concerns. There isn’t a large variety of fruits and vegetables that can be grown indoors, yet, but they are figuring it out. I read an article the other day that a couple of companies just started doing strawberries. Fresh strawberries, year round…

But I know we like to play short term here. I think that rising food costs are a legitimate catalyst. This stock hasn’t really slowed down since the war started. Does it still have legs.

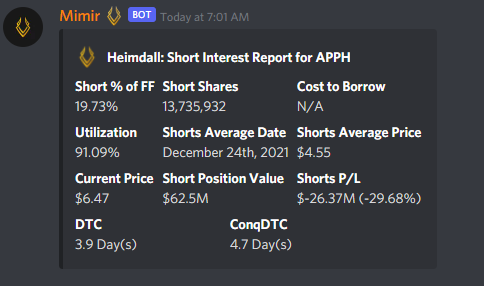

There’s also the matter of short interest. Mimir says shorts are getting sweaty:

If this reaches $6.75, the Shorts P/L will be at (-50%+). It hit $7 intraday yesterday. Wish it was giving a CTB number. Utilization is high, and DTC is high too.

I’m going to watch this today, maybe take a small entry. Just a sentiment/speculative entry to compel myself to do some more DD. I have not read their financials or guidance yet