This is a list I compiled for @Isaiah of numerous shipping companies (and related) I have on my watch list.

I’ve tried to break them up into groups since most companies only stick to one type of transport. If they do multiple I’m only putting in one group but will list everything.

Containers

DAC = Danos

GSL = Global Ship Lease - Leases container ships to other shipping companies

MATX = Matson - Pacific only

ZIM = ZIM - Container, Car Carriers

Ty for this , this stems from articles im seeing such as this. Again , take it with a grain of salt since its citing someone on a consultancy firm who could be saying things out of self interest. It could be a good play as something that will be more expensive regardless of escalation or descaltion of Russia/Ukraine war.

Just wanted to chime in by saying that our CEO sent out an email last week stating that the sales team needs to start setting expectations to prospects and clients about lead times this upcoming year (we receive our machines from Germany via ships and container). There’s no way, given the already backed up ports and now the war, that shipping is going to ease this year.

Nice job team. From personal experience as of Friday, precious commodities (gold/silver, etc) transport internationally jumped cost +20% including delay of shipping fee plus cost of fuel when state side. (This is specific to a deal I am on, just as example). Not from the Russian region and this transport is via air.

Would say that transport via air will also increase, along with ground shipping increases due to fuel getting higher.

Kinda short notice, but possible CRME play leading to earnings? They’re sitting at 14.18, up from 13.50 a few days ago. Spiked up Wednesday into Thursday and then came back down some Friday.

Gonna look again tomorrow PM.

edit: meant to say 13.50, not 3.50. just caught it.

A couple of those under the “tanker” category operate some LNG carriers. I probably should have denoted that, I’ll go back through and find them tomorrow. But I’ll add those two tickers to the list now.

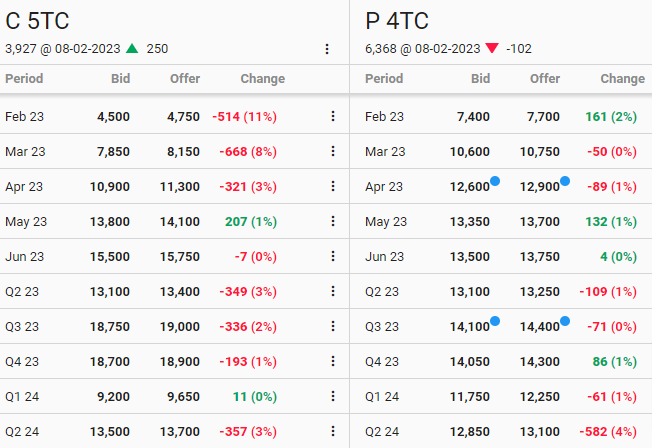

ZIM has earnings 3/9 PM. Would these news and futures prices be bullish for ZIM’s guidance? If so then maybe playing the run up along with the earnings might be a play

Prices are not quite at their 52-week high either.

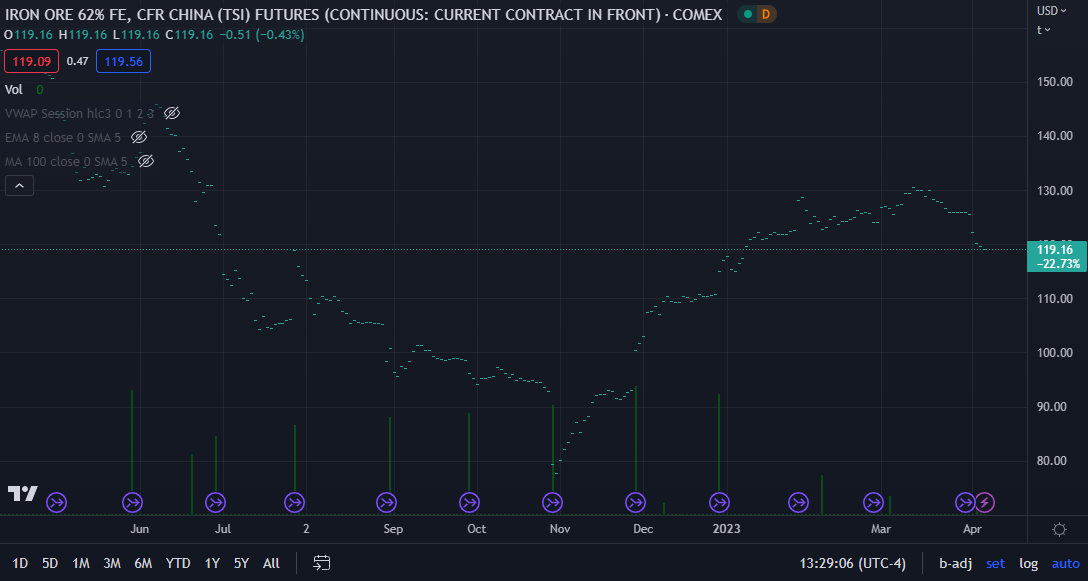

Now, the situation is a bit more murky compared to containerships as the Ukraine war situation does force inefficiencies into the dry bulk chains that has increased demand for iron and coal to be sourced from farther and take longer routes, but worth keeping an eye on given the ongoing concerns around global economic slowdown.

Might need to watch this for a bit to decide if this is a temporary dip (and therefore a chance to top-up) or if things will run mostly flat from here.

China lockdowns and seasonality effects have brought BDRY to its recent floor levels again. Will likely initiate positions with the first signs of lockdowns being lifted.

In the 8 months since the last post, dry bulk rates had fallen by half. It might be showing signs of recovery though, mostly based on the China reopening narrative.

BDRY is the ETF that tracks dry bulk fright futures.

This is the list of all the dry bulk carriers I’ve been tracking. Most of them are at or near ATLs. This does not mean they will go up now, but since they are all down by so much, a positive catalyst can move them nicely.

I’ll check on each of the companies in the next few days. Some of these are local to some routes only, others only run certain sized ships, and others yet only run certain types of bulk items.

Overall though, this could be a nice opportunity in 2023 as China opens up and starts guzzling raw materials again.

Initiated a BDRY position at $9 on Friday. Chinese New Years holiday seems to be all of next week, after which we’ll see if the much awaited “China reopening” was a thing, or a flop. Some chatter around iron ore prices picking up, and downside seems limited at this point. Fairly speculative position though.

All this suggests that we should recover sometime, but also that it might take a bit since Mar and Apr rates are also depressed. Anyone looking to get in will have to be willing to hold for months.

My cost average is currently $6.60, and am down 17%. Have entered in size, and have additional buy orders for $6 and $5. No options, will get those once China reopens, it stops raining in Brazil, or whatever other thing pivots that is holding BDRY down.

BDRY seems to be bumping up on the $10 line. It seems to track iron ore prices pretty closely and that is also going down. China just doesn’t seem to be pulling enough weight…

Given this, have liquidated all BDRY holdings for $9.93 (~ +24%). Will get interested again if it drops close to $6.

Incidentally, many dry bulk carrier stocks are at 52W lows except SB and PANL … these will be at play too on the other side of the global slowdown. The 2022 orderbook was weaker than necessary, and ship yards have significant backlog.

BDRY got close enough to the $7 line, and the 6/16 8P sell order I had up for $1.20 filled sometime today. Willing to own BDRY at $6.80, if I get assigned. But hoping prices bounce off this line again and over $8 over the next month.

Got assigned on them puts a few days before opex. Wasn’t paying attention and forgot to roll out… Cost basis $6.80. Setting staggered sell order for around $10 for now. Not enough juice by far for CCs.