Ticker: BTBT

Description of why you are requesting DD: Could be missing something really stupid, but mostly just want to share my thoughts/analysis

This isn’t a call to action, just a call for another set of eyes to look at this. I don’t have timing or catalysts, and everything related to cryptocurrency is a giant schizophrenic question mark.

Bitcoin is going through an anemic phase which, though they don’t track perfectly, do affect mining companies. BTBT has been struggling after a significant burst on October 29 that appears to be tied to the general pattern of BTCUSD pairs.

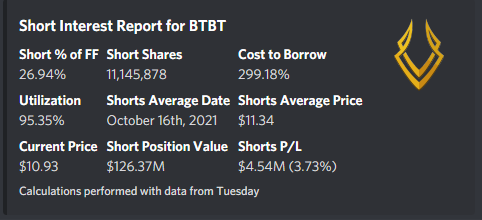

What has caught my eyes about this particular ticker is the average short price of $11.34 (representing a 3.7% delta at close today), the cost to borrow of 299%, and the free float to short percentage of 27%.

I broke out my charts and have the opinion that BTC just wrapped up a wave 3 which signals correction (and has been seen) followed shortly thereafter by some more growth. Specifically it looks like it may be wrapping up the first leg of a complex correction wave which, if correct, signals a short period of time in which mining companies may benefit.

Overlaying the performance of Bitcoin for comparative purposes on BTBT, we can see that the two don’t track perfectly but we can see some correlation between the performance of the two (with stronger correlation occurring in the Spring and Summer of 2021).

Looking to immediate OI, this upcoming Friday, the vast majority of it lays just out of the money, however as noted above a good BTC day could signal the difference between OTM and ITM for the largest chunk of OI.

Expiration Date

Type

Strike Price

Price

Volume

OI

11/19/2021

Call

$12.50

$0.07

2121

35938

11/19/2021

Call

$15.00

$0.05

567

24229

11/19/2021

Call

$20.00

$0.05

174

12148

11/19/2021

Call

$10.00

$1.00

373

11863

11/19/2021

Put

$20.00

$9.00

4

10403

If we are truly in a Wave 4 following EWT, this could be a short window. I think it merits watching the performance of BTC for the next couple of weeks and monitoring the SI and OI to figure out if this could be an opportunity.

I’m going to update this from the Request Category to a full blown DD, however will also be labeling this in the boomer/swing category. Earnings for Q3 are scheduled somewhere between November 30 and December 20 and while swings related to changes in BTCUSD value seem to cause waves in this stock and others

A few elements I want to capture in this write up:

TLDR Thesis

Historical Catalysts

What are we expecting from Q3 Earnings?

How did this compare to previous earnings?

What major initiatives are underway?

Why should we consider this for a long hold?

TLDR Thesis

With rapid fluctuations in cryptocurrency, specifically Bitcoin, value, minor fluctuations in stock prices will be inevitable. This industry’s revenue is predicated on their ability to mine cryptocurrency which is a double edged sword - we are aware of the value of their assets at any given time for better or worse, however we may not be aware of the production of their miners.

Near-term price increases in BTC can trigger some pain for the registered shorts on this stock (which are currently ITM), however I believe the more valuable play for this particular stock actually looks as far as March 2022 after typical seasonal increases in cryptocurrency values, and stronger performances beyond Q3 as power supplies and miners stablize after inter-contintental migration.

Historical Catalysts

As noted in the initial write up, swings in mining company stock price loosely correlates to the value of Bitcoin and other cryptocurrencies. As BTC increases in value, we can see spikes in not only BTBT’s stock price, but also each of their competitors. Each line is labeled below and represents % price change over time, but shows performance of BTBT, HUT, MARA, and BTC. Vertical lines represent spikes in stock prices, and one can observe that many of these spikes occur simultaneously:

When BTBT partnered with Digihost Technologies to increase their collective hashrate, the stock exploded and with good reason. Higher hashrates increases the likelihood of successfully mining coins in a Proof of Work (PoW) frameworks like Bitcoin. Quite simply, more hashrate = more Bitcoin = more revenue = higher stock price.

Increase of hashrates through partnerships and purchase of miners is one of the primary means by which these mining companies make their money, so any news of increased resources will be bullish in the short term.

What are we expecting from Q3 earnings?

Well, we don’t have to try to hard to find the answer to that question, but allow me to digest it for you.

They moved their operations completely out of China due to cryptocurrency crackdowns. As a result their mining operations suffered and they produced roughly 50% of what they did in Q2.

248.36 bitcoins were mined in Q3, translating to $15million currently but $10million at the end of Q3

Hashrate was reduced by 0.308 EH/s, which does affect their output as well

Additional power supplies needed to bolster production have been delayed into Q4 2021 and Q1 2022

The Better News

The company remains laser focused on powering their mining resources using renewable or zero carbon resources, with their American operations being 47% zero carbon facilitates, and 100% of their Canadian facilities powered by recovered natural gas. This provides some level of protection from potential legislation that could target high carbon producing Bitcoin farms.

With power supply deals already in place, as they come into place in Q4 2021 and Q1 2022, production within these facilities will improve

Through June 2022 they will be incrementally adding an additional 10,000 miners, which will supplement those lost between Q2 and Q3

Appointed Brock Pierce, Chairman of the Bitcoin Foundation, to their board of directors which took effect on October 31, 2021. Having strong, seasoned guidance on their board of directors bodes well for this organization.

How does this compare to previous earnings?

The elephant in the room was the significant reduction in Bitcoin production by Bit Digital. Q2 product 562.9 BTC, whereas Q3 produced 248.36. This > 50% reduction was largely uncontrollable due to full operational relocation and loss of mining resources, however it may not resonate well with shareholders paired with recent BTC corrections.

What major initiatives are underway?

Perhaps the most intriguing part of this company is their commitment to sustainable mining, offsetting some of the more recent concerns regarding the carbon footprint tied to crypto mining. As noted above:

47% of the energy used by three US facilities are 0-carbon emissions

100% of the energy used by one Canadian facility is recovered natural gas

Bit Digital is also currently working with an independent ESG consultant (APEX) to become one of the first publicly listed bitcoin miners with an independent ESG rating.

Why should we consider a long hold?

Compounding the above, it seems that the allure of BTC fluctuations may encourage you to play this as a scalp and you would not be wrong to do so. However, with so many positive initiatives planned between now and summer 2022, it seems that this organization is going to accomplish two things by the end of the 2022:

Increase production by adding more power and more miners as they continue to build their footprint in North America

Decrease emissions by sourcing competitive renewable/zero carbon energy providers

Those are my thoughts. Please feel free to add your thoughts as you see fit! I thought I saw a high short situation here but I think this time the shorts may be profitable if BTC doesn’t have a sudden upswing.