As a lot of you guys are seeing this earnings season, stocks that miss are being decimated. The one I think still has room to drop is Docusign ($DOCU). It was a Covid boomer stock that shot up to over $300 a share during the pandemic. It has definitely gone down considerably (currently sitting around $70) but I personally think this is still overvalued for the company.

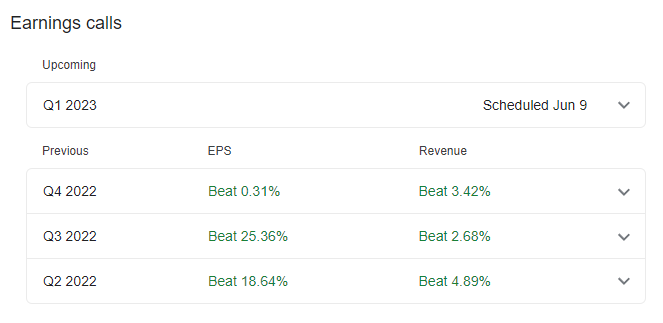

Based on the image below, it seems like quarter after quarter, they report a lower eps than the last. With Covid restrictions not really enforced anymore, I don’t see how they could have increased their profits during the last quarter.

Wouldn’t it be better to go further out into expiry (assuming you’re holding the contracts through earnings)? Theta will really eat into the value of the contract since June 3rd is a Friday.

I have been watching this for a few weeks as I plan to play it leading up to earnings. Spreads on the options are starting to tighten but still not great. I will likely look to play the week or two after earnings.

Keeping an eye on this leading up to earnings. Haven’t opened a position yet but I’m looking at the monthly for June so that the theta still has some chonk on it after earnings June 9th.

Thanks for posting this.

Looked at the last few quarters financials, and they aren’t great, they have been getting hammered by expenses the last few quarters. Free cash flow is tightening. Rising expenses is something we have consistently seen this earnings season, so I would assume docu will be reporting similar headwinds June 9th. Ive used Docusign a handful of times and I happen to like them, it seemed to work as designed for me. Ive just never understood the secret sauce. And thats coming from a place of ignorance, I need to do some reading. But at the very least, there is a reality where docusign can have a great service, but rising expenses force them to make tough descisions like raising prices to their customer or watering down their experience. Think Netflix. This ER will give us clues if we are possibly heading in that direction imo. Im adding it to my shit list and will post anything potentiality valuable.

Thanks again !

Hopped into a DOCU 80 Put for June 3rd just a few minutes ago. Hourly chart is at a high point respective of patterns from the last week or so, so expecting some downward momentum in the next two days. Will cut anywhere from +10% to infinity. Depends on when I login to my account

Earnings are this Friday and this stock has been pumped up quite a bit. I’m not very familiar with this space, but I don’t see how this stock is trading this high even with a partnership with a large tech company.

Even with beating earnings consistently, the stock has fallen a good amount the next trading day, over -20% and -42% the past two earnings.

DOCU did manage to trade up 5% to its ATH back in September, but we are arguably in a bear market with a lot of eyes on high tech valuations.

It would be also important to note FOMC meeting is next week. Markets have been on a tear for about a week and a half and I highly suspect a lot of volatility next week. If you are not playing this for earnings, it may be worth it to wait out IV crush and open a position next week when markets start to really move.

Given the AH movement from the MSFT news, I will be trying to open a position tomorrow as I still think the stock will dump.

Idk if it helps but etrade says +- 15.62% implied move and a decent amount of june and july straddles at 75 and 85 hit the tape today along with 1/24 95p. Idk if they selling pre earnings day for a volatility scalp or not but those were the biggest transactions i see on it today. Docu seems like a good short target but if cpi is somehow bullish it may get swept up in the market run so keep that in mind and msft news may get the bulls hard on the stock again depending on what they say in the call. Good luck!

Look at the estimates, last quarter’s revenue was 580MM and this quarter’s estimate is only 581MM, that’s an EASY beat considering this is the kind of business that doesn’t get a lot of unsubscriptions. If you have a docusign subscription for your company, that means you need people to sign documents, and that demand doesn’t typically change or go away. Next quarter’s estimate is only 602MM, which they probably get close to THIS quarter, it’s not that hard for them to guide above that either.

Remember that earnings moves are based around actual vs expectations, and it seems that the expectations are very low here. I didn’t really evaluate EPS because this company trades on revenue.