Original thread here: AGC, Gamma Squeeze play + possible Short Squeeze - #260

Ok, so… the long tired journey of AGC has come to an end… but now we get to stare at GRAB. Now I’m going to clarify something that I don’t think a lot of people understood the first go around:

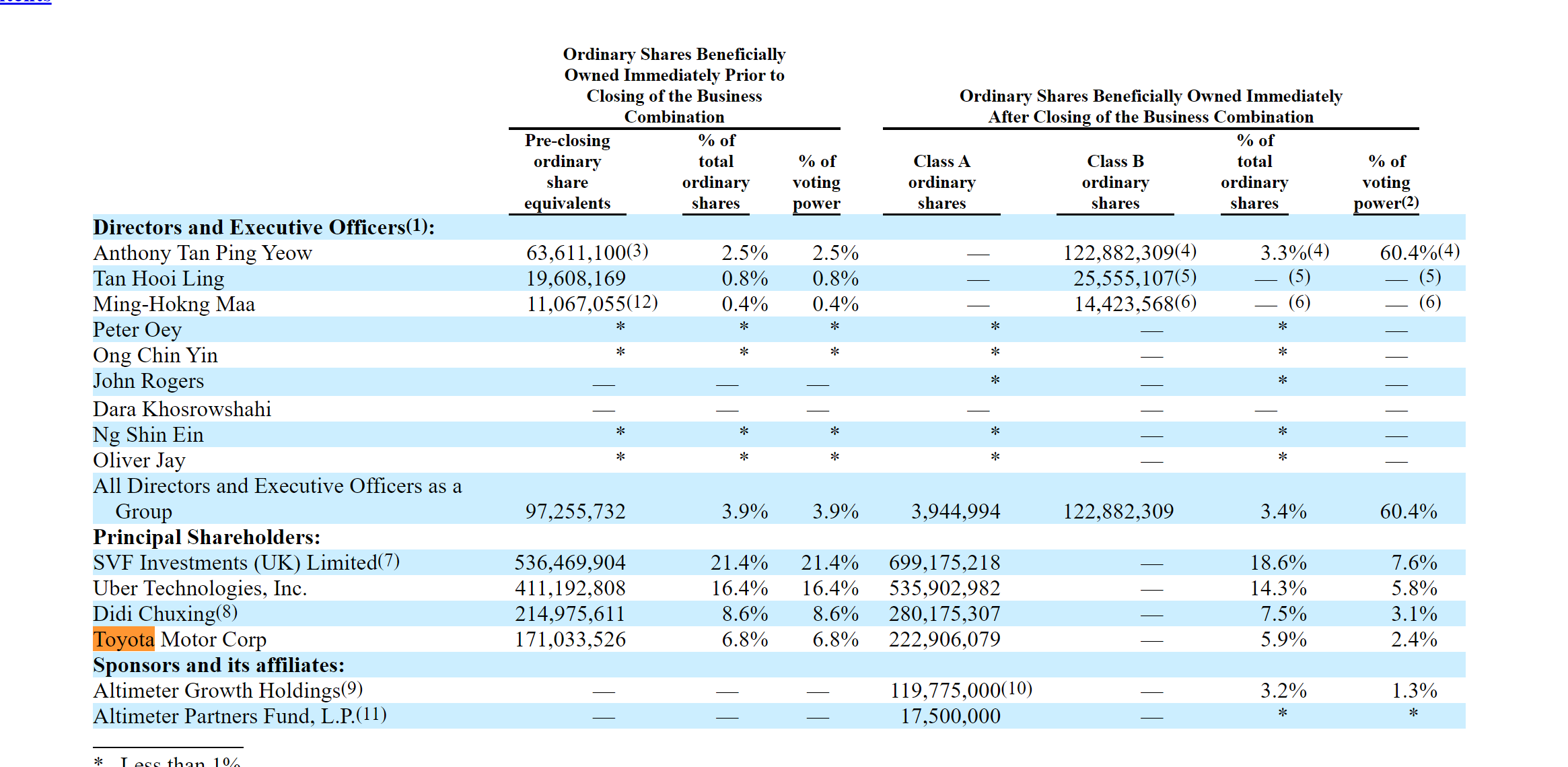

GRAB IS OVERVALUED

Fundamentally speaking, it’s right where it should be after everything is all unlocked. The company isn’t quite worth it’s $40B valuation… yet. However, they are a tech company and tech companies often aren’t valued anything like they should be. So with that said, this is simply a setup, something that could move. It’s not something to put your life savings into, it’s not something to watch endlessly, it’s just an option… and there are probably far better options out there.

However, in the short term, there is a chance for some movement on this as a deSPAC play. I’m busy today so I’m going to cliff notes some research I did last night and expand on it later, however, the conclusion is that “good SPACs”, or rather, SPACs that target companies the market actually gives two flying fucks about generally run a little after merger. This is true for: SPCE, LCID, DKNG, SOFI, QS & OPEN and I’m sure others. Now, what I think is going on, is the same thing going on with GRAB right now… they initially cannot be traded across the market. So what happens I think, is you get a day - couple day timeframe where the stock just drifts where it is as sellers unwind slowly without much buy side support (this is also true for all those tickers, they generally drifted for a couple days and then shot up). Then, when the ticker becomes trade-able, the dynamic quickly inverses and you’re left with a fresh stock without a lot of resistance points as most everyone that wanted out is likely already out.

This thread is basically created because I know people have positions in this play and I want to keep them informed of what we’re thinking on it.

Now there is one other factor that could come into play here: The Cramer pump. Cramer has said repeatedly that he’s bullish on GRAB. To my knowledge, he has not really addressed it at this point and he’ll probably wait a couple days to do so I think, but, as that Reddit study concluded… your mans has pump power and those Boomers would love to get their hands on Asian UberEats before it becomes UberEats. Just a thought. Trade responsibly.