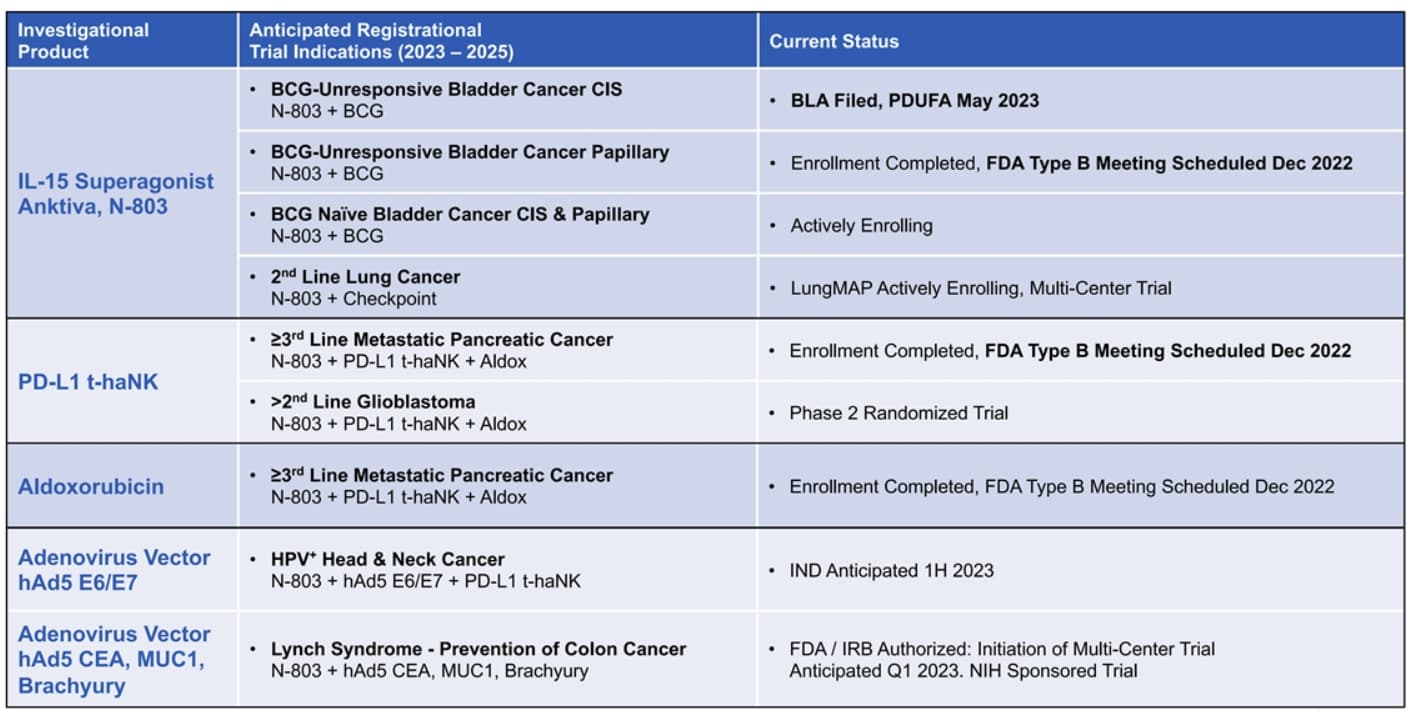

ImmunityBio’s clinical pipeline consists of 27 clinical trials—18 of which are in Phase 2 or 3 development—across 13 indications in liquid and solid tumors (including bladder, pancreatic, and lung cancers) and infectious diseases (including SARS-CoV-2 and HIV)

positive data from the company’s pivotal Phase 2/3 trial for BCG-unresponsive non-muscle invasive bladder cancer (NMIBC) carcinoma in situ (QUILT 3032) and Phase 2 trial in advanced pancreatic cancer (QUILT 88).

Data showed better efficacy and adverse events profile vs. competitors (instiladrin, pembrolizumab, …)

IBRX made already the investment the to build the complex/cost-intense manufacturing platform, hence my assumption that they are confident about the approval

biologics license application (BLA) has been filed (May, 23rd) for N-803(Anktiva) for use in combination with Bacillus Calmette-Guérin (BCG) for the treatment of patients with BCG-unresponsive non–muscle-invasive bladder cancer (NMIBC) carcinoma in situ (CIS) with or without Ta or T1 disease

FDA previously granted N-803 Breakthrough Therapy and Fast Track designations when used in other combinations/indications

The Food and Drug Administration (FDA) is currently reviewing the Biologics License Application (BLA) for N-803 plus BCG for the treatment of NMIBC CIS with a Prescription Drug User Fee Act (PDUFA) date of *May 23, 2023

Positive data as well on high-risk carcinoma in situ (CIS) and papillary non-muscle invasive bladder cancer (NMIBC)

Big Pharma are facing a lot of LOE the next years (see graph below), so i believe we see a lot of M&A acitivites. QUILT 3.032 trial met its endpoints for both indications

My Positoon: IBRX DEC23 5C avg. 1.98). I plan to sell the peaks to cover cost until FDA approval, recommended entry point is below 2.1 for the IBRX DEC23 5C

Edit: i am focused purley on the “Cancer” play, data releases of research in other TA such as C19 will impact the price the next months as well.

“The peer review and publication of data in NEJM Evidence highlights the significance of the positive results of the QUILT 3.032 trial in patients with BCG-unresponsive NMIBC,” said Patrick Soon-Shiong, M.D., Executive Chairman and Global Chief Scientific and Medical Officer at ImmunityBio.

As the results of this phase 2/3 study are currently being reviewed by the FDA because they are basis of the FDA submussion, we see a nice up trend the last days (the overall market helped as well)

On November 15, 2022, Dr. Patrick Soon-Shiong, the Executive Chairman and Global Chief Scientific and Medical Officer of ImmunityBio, Inc., a Delaware corporation (the “Company” or “ImmunityBio”) will participate in the 2022 Jefferies London Healthcare Conference (the “Conference”), which is taking place in London from November 15-17, 2022.

IBRX is very transparent in terms of progress, data has been peer reviewed, trend is positive…at the same time with every FDA approval play there are high risks involved.

Up today 35%, a common thinking is that labeling discussions are bullish indicator for approval. In reality it depends on how deep these conversations are. Stock was heavily beaten up in the last weeks, so i dont mind this small run.

So the share price is back where it was in Dec 2022 thanks to 215% run up the last month. This play gave me the most grey hairs of all biopharma plays. Saying this i totally de-risked this position and was even able to take profit.

received a complete response letter (CRL = rejection) from the FDA

deficiencies relate to the FDA’s pre-license inspection of the Company’s third-party contract manufacturing organization

No new preclinical studies or Phase 3 clinical trials to evaluate safety or efficacy were requested by the FDA

The wild ride continues, down 60% in pre-market. We are looking at a 9-18 months horizon for a new PDUFA date

Position: Will close my remaining calls to take some profit You all can imagine how happy i am right now that i covered CB and already took some profit. Good Reminder to stay true to our strategy !