I’m crazy for even posting this, but here goes.

TLDR: Company is under-estimating net proceeds from liquidation. Represents possible value. High Risk.

LUB, Luby’s Inc. A once well-known multi-brand restaurant franchise. Last year, in the heat of the pandemic, the board proposed (and the shareholders agreed) to liquidate the company’s assets. This included multiple brands and properties.

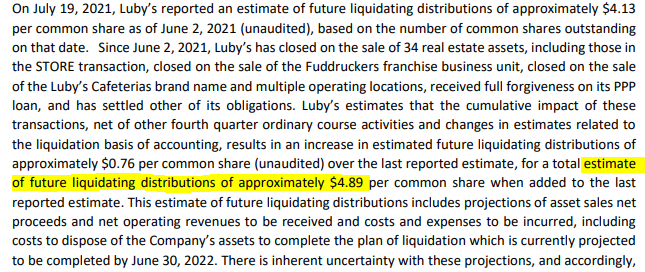

The original estimated net proceeds was estimated at $3-$4 per share. This estimate was given on Sept 8, 2020. Source linked here.

They were able to liquidate a portion of the assets and recently returned that to shareholders via a special dividend of $2 per share on Nov 2 (ex-div date). Afterwards, they’ve revised their estimate of total asset liquidating values minus expenses and liabilities to $4.89. Source linked here.

After the dividend, you can calculate the expected remaining asset value by subtracting the $4.89 per share value by the $2.00 per share dividend to get $2.89 per share, which, as of the writing of this post, is where the stock currently sits.

So why should you care?

The board originally undervalued the net value of assets as a maximum of $4, average of $3.50. If you take the latest estimate (4.89) and divide it by the average of 3.5, you get a 39.7% underestimation of asset value (net liabilities). If you take the max original estimate of $4, the underestimation shrinks to 22.25%.

Now, I’m not expecting the remaining assets net liabilities to be another 40% increase, but there are good reasons to believe that the board has under-estimated the value.

-

Insiders own 38.9% of shares. By under-estimating the value, they stand to benefit. Over the last 6 months, insiders have purchased a total of 97,500 shares. All of these purchases happened 3 days after the company announced the liquidation process.

-

The board has a vested, face-saving, interest to conservatively estimate asset value so they don’t look bad at their next job. Imagine they over-estimated the proceeds by 40% instead of under-estimating. They would look ridiculously stupid. Now, they can point at LUB and say, “look, I was able to squeeze significant value out of this company because I’m awesome.”

The company expects to liquidate all assets by June 2022. This could mean that if you find value in this DD, you will be holding on to this rotten stock for awhile before you see any return (if any).

I am not sure how to play this liquidation other than holding shares through company closure. But I do think that there could be some value here. I’m going to keep reading and digging and see if I come up with anything. Feel free to point and laugh at me all the way there.