Opening a post per Conq’s recommendation to clean up trading floor.

Lulu is the clothing brand that our wives want us to buy instead of trading.

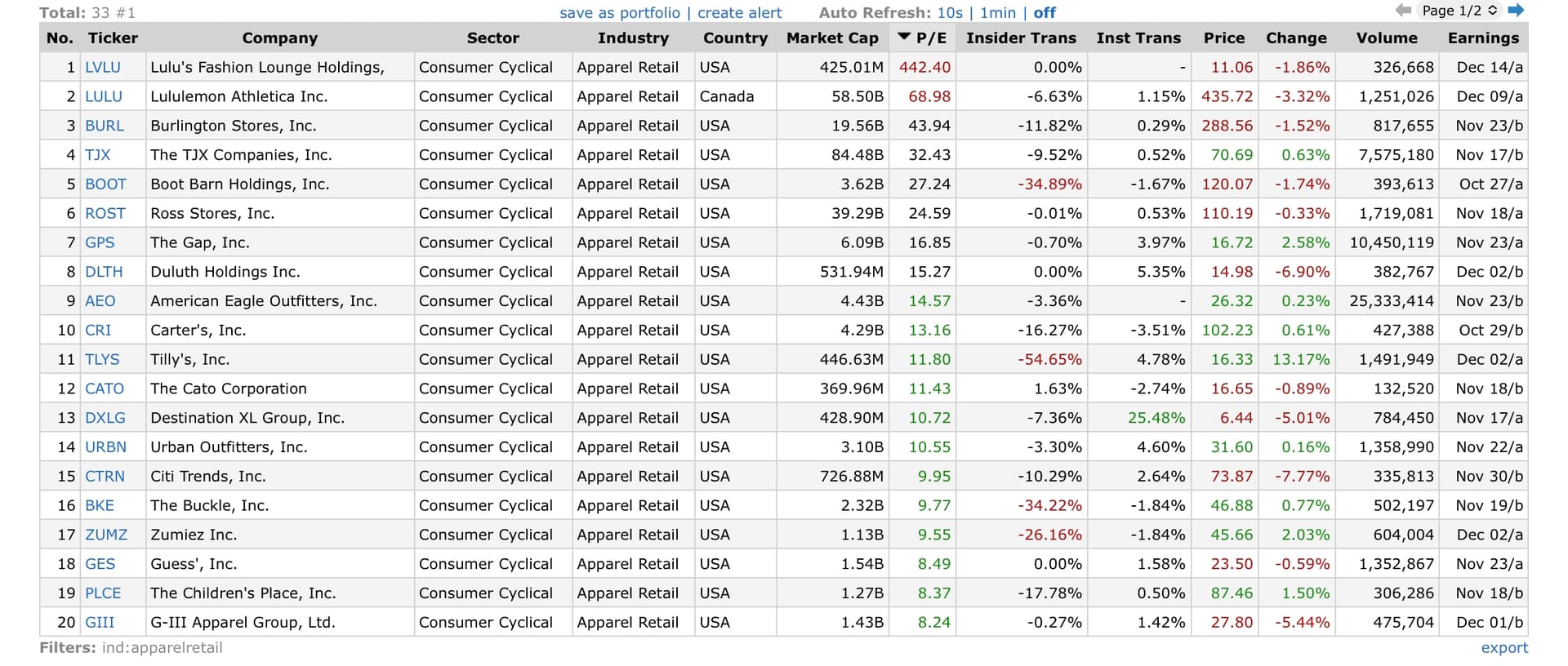

Growing fame in the pandemic due to people not working out, rocking a business mullet with casual clothes and scoring the coveted motley fool recommendation, they’ve been on fire with growth.

After recent retail guhs might be worth a look at puts for their 12.9 earnings.

Topics to discuss:

remarks in q2 guidance for q3

supply chain manufacturer problems (see gap’s line athleta or lgvn)

return to normal

Covid stock busts (peloton, zoom, docusign)

Reasons it might not guh:

zumiez did ok on earnings

wfh may be here to stay

gyms have reopened (but let’s be honest people buying lulu aren’t really going to the gym)

Mens clothing taking off (more than just for the ladies)

This link hopefully brings you to where we started talking about LULU on trading floor for pulling the research everyone was doing. Let me know if it doesnt work.

Lulu just had a share buy back in october, beilieve it was something of 600m. Then as of the 3rd, their director informed them that she will be resigning sometime in 2022. Believe the 600m buyback would be bullish but seems as though thats what created the run in october, maybe its loosing steam?

I don’t agree with this, and something to note is LULU is the Apple of gym wear. As a frequent gym goer, it’s normal to see it’s the go-to leggings/bottoms for any woman that’s in there, fit or not.

LULU also has extremely high-quality clothing, and before covid, this was known and a driver of their brand and sales. I think they do an extremely great job of hook and sinker, meaning, once anyone buys a single piece of LULU clothing, they enjoy it to the point where they invest more. I personally fit into this category, and so is my gf. We both very much love the quality of our stuff that we’ve had for years, and continually add. I’d find it difficult to find anyone that’s unhappy with their clothing.

Something that might be worth looking into is the growth of LULU purchasers through their app data vs other sports apparel. I am on the side that they have to not only show growth in revenue, but grabbing more of the total addressable market of the fitness apparel sector.

There is almost no case to be made for that valuation given their revenues EVEN IF they are killing it. If we look at the chart, the source of the current insane valuation is, you guessed it, April 2020:

This is why I’m not very excited about this play, I’m not sure the ER is going to be bad and catalyze any sort of correction.

It seems like the things that have to happen to have a drop like Gap are -

Miss earnings overall

Reduce guidance

But we can’t really equate Lulu 1:1 with Gap. They may hit similar supply chain issues but Gap’s Athleta brand actually did quite well in sales performance. Gap also reduced guidance (from what I can gather from the Q2 to Q3 transcripts below) like 50%, which probably contributed to the tank.

Missed guidance for Gap was due to 2021 supply chain issues causing inventory issues as well as them needing to pay extra for freight. They said Old Navy was disproportionately affected by this and that’s their #1 seller and a different market segment than Athleta.

Again, for Gap (the reference I’ve been using for my Lulu DD), Athleta actually seemed to be performing quite well. That means that it’s not a slam dunk that Lulu misses earnings, and even if guidance is lowered, I’m not sure it’d be the 50% slash that Gap revised because their Old Navy label was disproportionately affected by supply chain problems and their number 1 revenue generator. IV is also super high on these.

I think I may sit this out. I agree with Conq that Lulu is way overvalued but I don’t see this being the event to start correcting them.

This to me, looks like a hard gamble atm.

Seems like a bullish loading transition towards a higher peak.

Supply has remained low since the buying rally last ER, but selling pressure has been gaining.

MACD remains above the middle line, thought the macd and signal lines have crossed and diverged clearly enough.

RSI is weak at 42, and BB%b is signaling a possible buy area.

SHORT Term:

You’ll want to ride the trend, then set Stop Loss Limit once you see gain.

To help confirm a further bear case, I want it to break down past the support lines marked in green–401.68 as last pivotal point.

IF it suddenly stops or bounces hard on any of those support lines, I would check the Options Chain Oi minutes before market close–especially prior to ER.

Options Premiums are crazy high, so I won’t be playing this, anyway.

Anecdotal but my sister mentioned that malls around her area saw a resurgence but with high end retail. According to her it’s all the wealthier consumers spending more on high end retail because they can’t spend on other things due to covid (no travel being the big one).