The strategy behind this is simple. Every week I will sell 1 MSFT ATM put expiring the next week. If it ends up ITM, I will roll it out by doubling (or tripling) the number of contracts and moving it to a lower strike. Any flat or up week will make all short puts expire worthless.

1 contract @ 265 strike = 26.5K notional exposure. I will set the limit for this trade at 250K notional exposure which allows for 3 - 4 double downs depending on how much the strike moves each time. I will also set the max strike at 300P as I believe at that level we can see a drop sharp enough on MSFT that’s too difficult to double down out of.

I tripled down on this today as it went ITM, trading in -1 252.5P for -3 240P at a 45 cent credit. Did this before earnings because the high IV gets a favorable roll.

Though it appears this move was unnecessary as MSFT popped on the earnings call.

Remember that a covered call is the same position as a naked put, so since I had available cash in the account, I just took assignment of the puts in a couple of the week and sold an ITM covered call and corresponding OTM put(s) to simulate rolling and doubling down on the puts.

So far the total cash outflow from this is -50,710, and I’m currently bagholding 200 shares of MSFT which at today’s close of 264.46 are worth 52,892. Total PnL up until this point is 2,182, and max total notional so far was 265 * 8 contracts, for 212K max notional exposure.

Sold 100 shares of MSFT @ 265.66 and 1 9/16 265C @ 4.15 this morning (so current position is a 265 strike covered call), this strategy is now deleveraged and is back to a single contract. This is the goal when you get a flat/up period, to have the leveraged up short put position expire worthless.

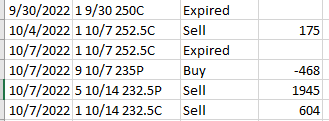

Kicked the 9 9/23 242.5Ps to 10/7 235Ps for a 34 cent net credit. Fortunately this is declining slowly enough to be able to kick the strikes down in a fairly reasonable way to trade intrinsic value for extrinsic value which will decay. Remember that this is basically a theta gang strategy on steroids.

Total cash flow: -19462

Current position value: 20769

Current PnL: +1307

Current PnL of buying and holding 100 shares of msft from Jul 8 (when I started this): -3342

While the market has moved against me substantially during this time, there is a lot of theta value accrued as well. Keep in mind that even though I had to pay to close out this week’s puts, they were originally sold for dollars and they were closed out for cents.

Doubling down makes it a lot easier to get the position to expire out. And it usually works pretty well since the stock has some kind of floor. MSFT is a cash flow machine.

Obviously, if you do this on some crap stock there’s a very real chance they’ll go bankrupt and you’ll lose it all.

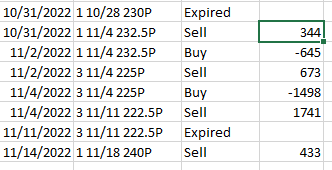

Anyway, an update on this. So on 10/14 I kicked the whole position down to 227.5 strikes for the following week which expired (and I got called out of the shares I was bagholding. As this was earnings week I did not put on a new position since there was a big rally the previous week and I didn’t feel the premiums justified the risk of earnings going to shit. I did sell a put today post earnings