TTWO has earnings post-market on Monday, 5/16.

Like all other tech, their share price has been punished with a 50% markdown.

Their current market cap is $11B; est 2022 revenue is ~$3.5B. Yet PE is still 20 and growth is in the single digits. Unless they have stellar earnings, difficult to see this rallying post-earnings. However, options are quite expensive, understandably, with IV at 78%.

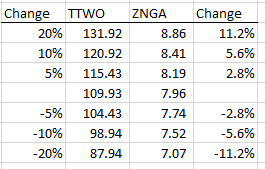

This is where ZNGA comes in. ZNGA is supposed to be bought out by TTWO using a price that is this formula:

$3.50+(0.0406*$TTWO)

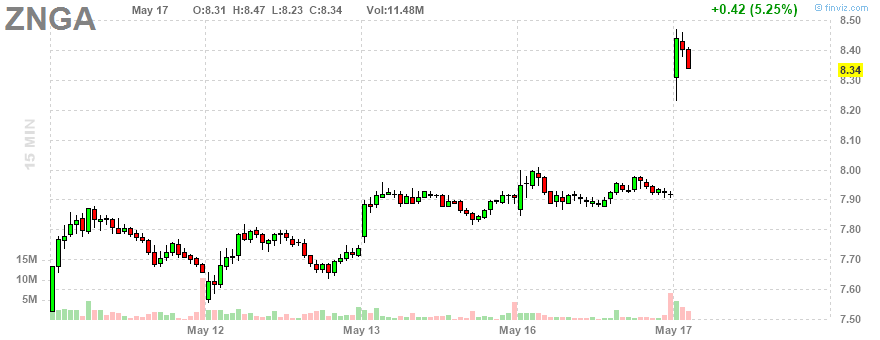

The current $TTWO of $109.93 maps to $7.96 for ZNGA; ZNGA is trading at $7.91 because of merger-not-happening risk.

That 0.0406 multiplier dampens the movement of ZNGA stock compared to TTWO:

And this is also reflected in seemingly cheaper options - IV is 47%. Note that it’s not really cheap, given that dampening effect above - it’s just more … affordable.

So will probably get some ZNGA lottos tomorrow for the downside. Anticipating downside because of the current environment and because ZNGA had rather crappy earnings last week too and they are solidly in the same industry.

Btw ZNGA shareholders are expected to vote on the merger on May 19. It would be shocking if they voted No, since TTWO paid a 64% premium and ZNGA has always struggled with cashflow and is in a difficult business. But it does mean IV may remain higher than normal post earnings of TTWO, which makes straddles/strangles just that little bit more interesting.