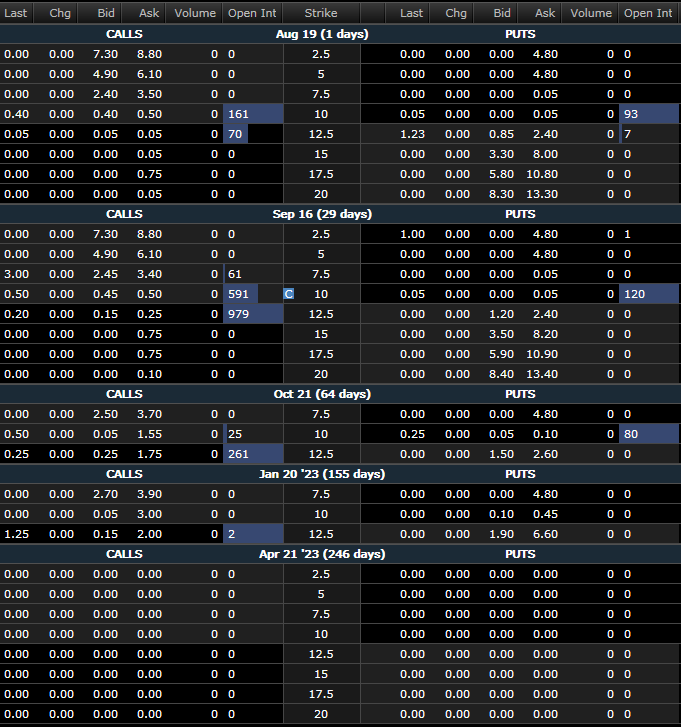

What’s the interest here? Looks like only 59 OI on 9/16 10c and 418 OI on 9/16 12.5c which aren’t even ITM. More volume today but this has a long way to go before it’s considered a setup?

Joined in with some September calls here as well. There’s a fair chance that nothing really happens here but I think it’s worth a small gamble with over a month left for this to play out.

I had scalped shares yesterday, but am back in with a share position at $10.41. Not looking for a home run, but wouldn’t be surprised by a run to around $11 at some point in the next month.

Also rolled my calls from Aug to Sept. A warning: Unlike ESSC and THCA, there doesn’t to be much of a market being made by MMs here. I had to sell by August for below intrinsic (0.35 fills mostly), so rolling to Sept (0.45 fills) cost me 0.10 per contract.

I’ll wait until next week at least to see if interest in the Septembers picks up.

Bid ask seems to be holding at 10.45-10.54 without a ton of volume which tells me the arbs may be out of this now.

We are essentially just waiting to see if 5 Rivers or some other P&D crew decides to stack some OI and try to run it. In that case I’d expect it, given the float or 2 million, to move similarly to ESSC in April/May and stall out and lose momentum around $11.00. Still a nice relatively low risk profit if you got in under 0.50 on 10c.

If float is ~2.3M then we’re looking for 2300 ITM OI for 100% of float right? We’re at 591 right now and still 29 days… Of course nothing might happen but we have time. Worst case we take a smallish hit rolling to the next month (or cashing out)

This isn’t exactly correct for total hedging coverage. Just because a contract is ITM doesn’t mean the whole 100 shares need to be hedged (it’s more likely than not). Safer to assume that the hedging requirement is 100xDelta for that contract

I think that is an important distinction to make that it’s based on the delta x 100, because then this also means that OTM calls have to be hedged as well. I’m not so sure that the MMs are just ‘waiting’ for calls to go ITM to start hedging them.

But as an option approaches ITM and goes deeper ITM, yes the delta of that contract will increase and increase hedging pressure.

Correct, now that we’re elevating the conversation to that understanding of a MM remaining in a neutral position. Taking into account the possibility of them seeing this mechanic whirring up, there may likely be a scenario where they buy those deep itm calls to hedge as well (if not as well selling puts or selling some calls in manner to open a call ratio backspread). There’s a lot of advanced leg mechanics I don’t think we take the time to consider and the implication of that on the hedging theory we throw around

Yeah it makes sense that it is very complicated or foolish to assume if we have X amount of ITM/OTM OI then the play is on. I would still like to explore maybe a range that would make sense though? 2300 ITM might be too simplified. So if we consider 100Xdelta for all strikes AND options strategies that MM can use to hedge, can we determine at least a range or safe range where MM would have to eventual hedge by purchasing stock?

Yeah so basically use 100Xdelta for all strikes and add a standard deviation closer to 3 to account for all of the options strategies that MM can use to hedge that we don’t know enough about. That could give you a “rough range”?