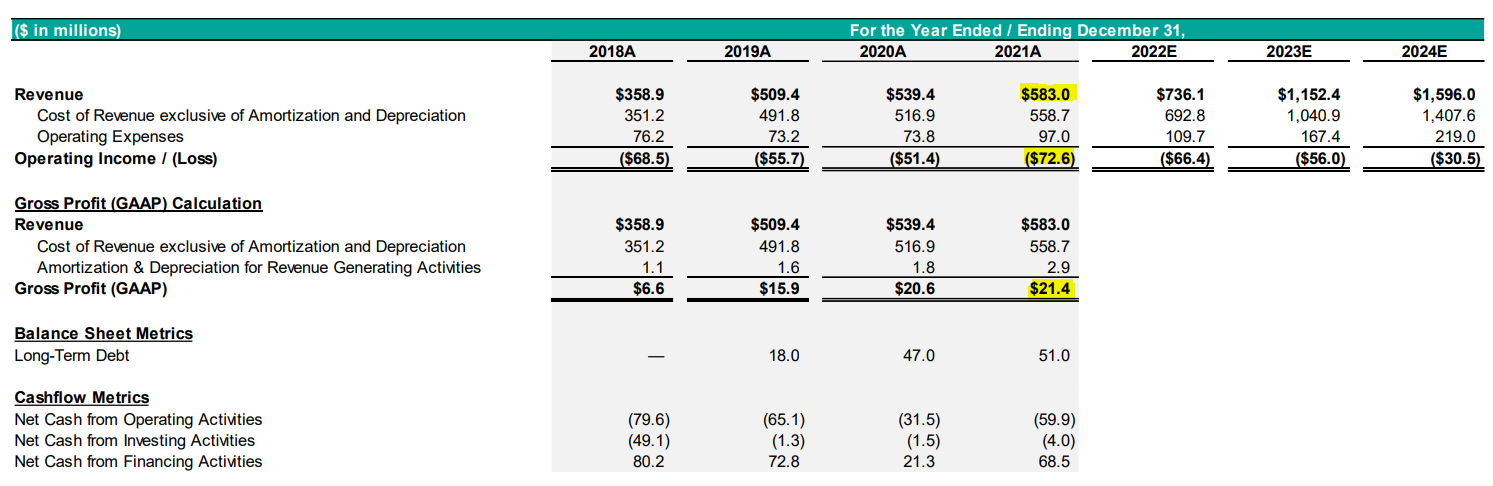

Trash brokerage! This is literally my neck of the woods. While we’re playing the despac element of this deal, there is some information you need to know about this organization. If they pop, by nature of being who they are they may present significant puts opportunities in the future.

Trash is already difficult because of three major players also in the industry:

- Waste Management (WM)

- Republic Services (RSG)

- Waste Connections (WCN)

Over half of the landfills in the US are privately owned, and these three own the lion’s share of them. They also own the most trucks, the most equipment, and a huge portion of the market share for residential, commercial, and construction and demolition segments. That then puts trash companies into two categories:

- Asset Light - like Rubicon, they own little to no actual trash equipment

- Asset Heavy - like the big boys who own much of the infrastructure needed to run a trash company

Rubicon’s primary focus as a business is in the SMB (small to medium sized business) and residential sectors. They provide “technologies” (that are in essence, broker agreements) to call on trash haulers who are already in a geographic area to provide services to their customers. This allows them to dispatch even potentially Waste Management or Republic to pick up your trash, all under a Rubicon Contract. They in turn provide a markup such that you only need to call them. This is a great model when you’re a corporate environmental or facilities executive who has to manage the waste for thousands of locations, but introduces an unnecessary middleman and markup when you’re just trying to get trash picked up at your house.

This concept of brokerage isn’t new. WM, RSG, and WCN all have their own brokerage divisions where they manage national chains or the relationships which each other’s broker team. Those broker teams also deal with Rubicon, facilitating their one-off contracts with these SMB clients. This allows all of the big name brokers to review the types of work that Rubicon is doing and effectively RFP with the larger portion of the base at time of contract expiration (which they also have visibility into).

Imagine trying to be a disrupter in an industry where all of your massive competitors have perfect visibility into every step you take, when your contracts expire, who your customers are, and they are dependent upon you to perform. This is the position that Rubicon is in.

They are delivering an exception digital experience in an industry that is largely untouched by it, but they are in a constant state of vulnerability because of how they do business. Given that they switched from trash brokerage to technology as their primary selling grounds, it is my belief that they are trying to be acquired by one of the big three listed above. However, their true value will only be as much as their technology, and all of the big three above are in the throes of significant multi-million dollar digitalization initiatives.

The allure of Rubicon as an aquisition target down the line will start to diminish as these companies’ digitalization efforts mature, their more lucrative contracts will likely be scooped up by the big guys at a significant discount, and their value will drop quickly.

I have little to no faith in the outlook of this company. The big three trash haulers in the United States are nothing to play around with.