Roivant offers investigational drugs in development for therapeutic areas such as dermatology, immunology, and respiratory diseases, as well as provides healthcare technologies which help healthcare institutions share and aggregate data.

Two potentially best-inclass anti-FcRn antibodies with deeper IgG reduction and simple subQ dosing give flexibility to maximize value across indications

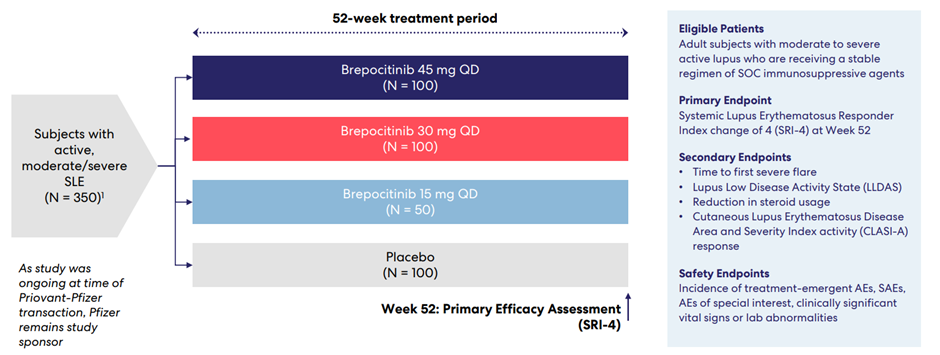

2023: Brepocitinib (TYK2/JAK1) Pivotal Trial Readout in SLE ( A Heterogeneous Connective Tissue Disease)**

Financials

$1.5BN cash at Dec.31; $1.7BN giving effect to anticipated proceeds from sale of Myovant minority to Sumitomo 3. Runway expected into the second half of calendar year 2025, and still ROIV announced public offering to raise $150m+.

Position: Shares (announced in the position system)

VTAMA is the only thing that has worked on my psoriasis - unfortunately, I only had some samples from my dermatologist and couldn’t get it filled because it was so new (and I don’t know if it’s on my insurance formulary.) Tried to find it here earlier today at a pharmacy in Argentina and they also said it’s very new (and not available here yet.)

Thanks for the write up - going to look into it a bit more before I make a decision.

Roivant Sciences (NASDAQ: ROIV) reported fourth quarter EPS of $-0.420, $0.05 worse than the analyst estimate of $-0.370. Revenue for the quarter came in at $17.05M versus the consensus estimate of $14.11M.

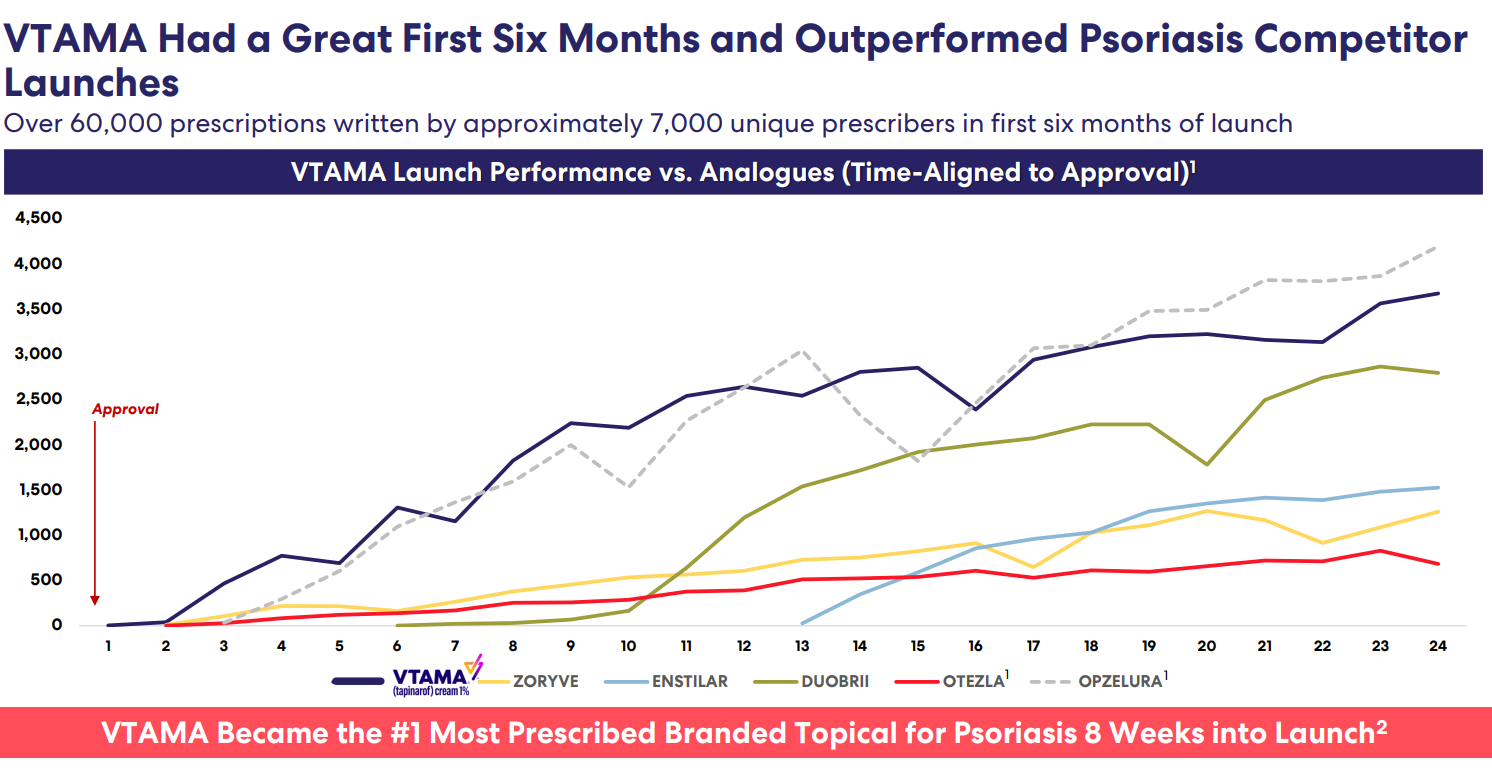

$9.2M in net product revenue from VTAMA reported for the quarter ended December 31, 2022, with nearly 100,000 VTAMA prescriptions written by approximately 8,600 unique prescribers since launch

VTAMA payor coverage significantly expanded, with 57% of commercial lives now covered

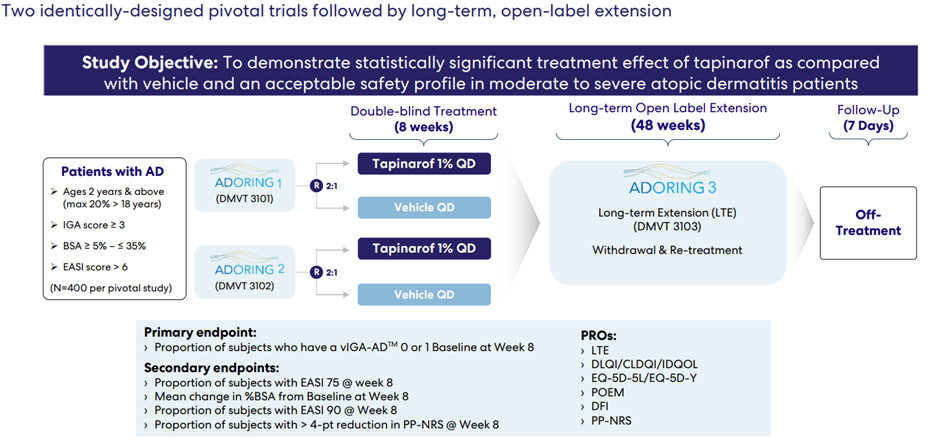

ADORING 1 and 2 trials evaluating tapinarof in atopic dermatitis fully enrolled, with topline data expected from the first study in March 2023 and the second study in May 2023

Partnership established with Pfizer to develop RVT-3101, a potentially first-in-class, fully human monoclonal antibody that blocks tumor necrosis factor-like ligand 1A (TL1A)

Statistically significant and clinically meaningful efficacy results reported at each dose tested in TUSCANY-2, a 245-patient global Phase 2b study evaluating RVT-3101 for the treatment of ulcerative colitis

Data from the chronic therapy period of the TUSCANY-2 study of RVT-3101 for ulcerative colitis expected in 1H 2023

Primary equity offering upsized to $230M in gross proceeds following strong investor demand with Roivant cash runway into 2H 2025

I believe we will see a drop as there was some expectations data potentially will be released as part of ER

…today announced that it will host a live investor call and webcast at 8:00 AM ET on Wednesday, March 15 to review topline results from the ADORING 2 study, one of two replicate Phase 3 studies in atopic dermatitis.

I dont like the short-notice of this as it doesn’t allow for a run-up, at least we know tomorrow morning.

To me it confirms the company is on the right clinical research path. Next milestone/catalyst is the topline data from the identically designed ADORING 1 trial in May 2023.