Overview

SEAH is a SPAC which is seeking to acquire Super Group, a leading global online sports betting / casino player:

- 2.5+m monthly active customers

- $44+bn in wagers in last 12 mths

- Licensed in 23 jurisdictions (excl. the US which it is expanding into) across the Americas, Europe, Africa and the rest of the world

Why I like it

https://twitter.com/stocktalkweekly/status/1453373389691932672

The tweet above offers quite a nice summary of the highlights but my take on why it’s an interesting opportunity:

- Global player in the online betting/casino space which has been quite hot

- Already profitable with strong financials (2021E Revenue of $1.5bn; EBITDA of $350+m)

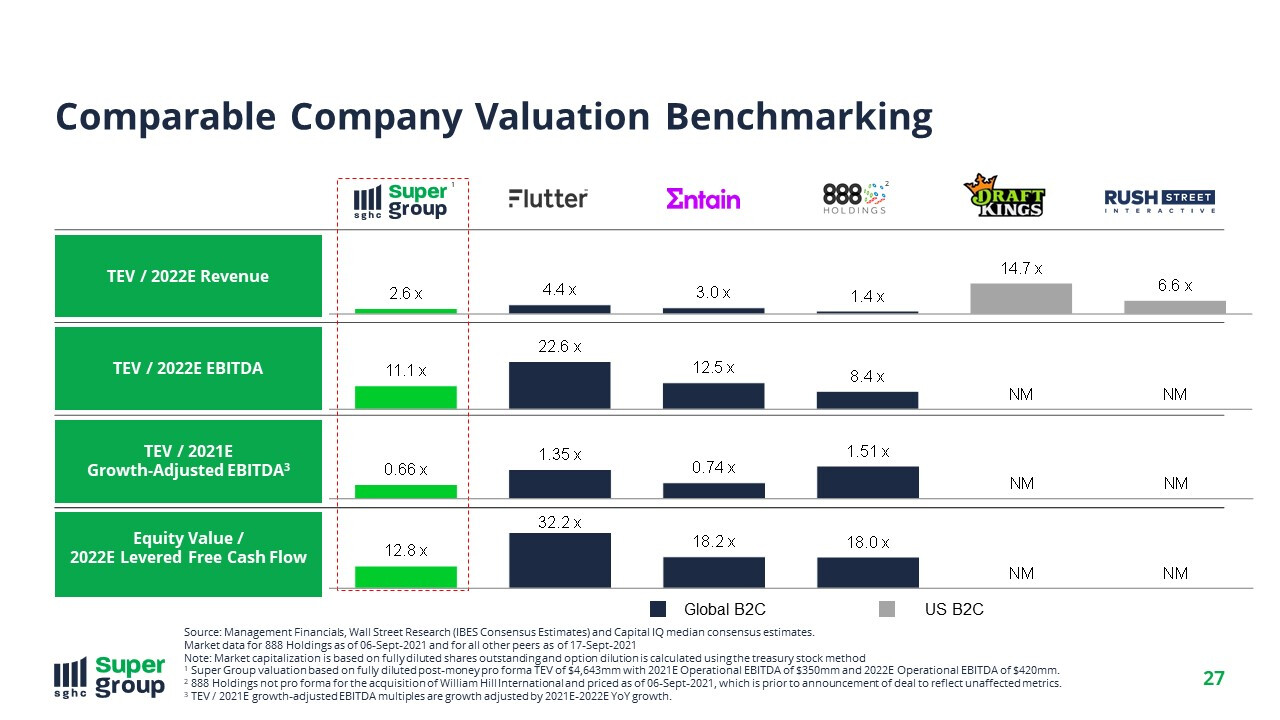

- Reasonably valued vs. peers (Undemanding 2022 EV/Rev of 2.6x and EV/EBITDA of 11.1x at $10 share price)

- Company executing well on its growth plans - Added a 5th live market in the US and new license in Poland (https://www.businesswire.com/news/home/20211020005681/en/Super-Group’s-Betway-Continues-New-Market-Expansion)

- Merger expected to close in 4Q 2021

- No PIPE, with the original Super Group and Sponsor retaining c.90% in the entity post-merger

How I’m playing it

Price has run up a bit and I like the stock at a price closer to $10 so I am running a buy/write on this, buying the stock at c.$11+ and selling calls expiring Dec '21 with a strike of $12.5 to collect c.$1 of premium. This allows me to reduce my cost basis to c.$10 if the stock doesn’t run, but caps my upside at just over 20% if it surges and blows past $12.5 by Dec.

If you like the stock and want to be more aggressive, you can choose to buy shares or calls instead.

Reference materials for bedtime reading

- Investor presentations:

https://storage.googleapis.com/supergroup-cms-production/2021_09_SGHC_Investor_Presentation_Part2v_Final_0649e45b5b/2021_09_SGHC_Investor_Presentation_Part2v_Final_0649e45b5b.pdf

https://storage.googleapis.com/supergroup-cms-production/SGHC_Investor_Presentation_2021_04_23_IB_v_FF_3fe7d4f95d/SGHC_Investor_Presentation_2021_04_23_IB_v_FF_3fe7d4f95d.pdf