Spotify is reporting Q4 2021 earnings afterhours tomorrow on February 2.

Does anyone think they could dump like $NFLX on slowing user growth or Monthly Average Users? Seems like eventually there will be a point where nearly everyone who wants Spotify should have it.

However, in their previous ER, they seemed to indicate strength in international growth.

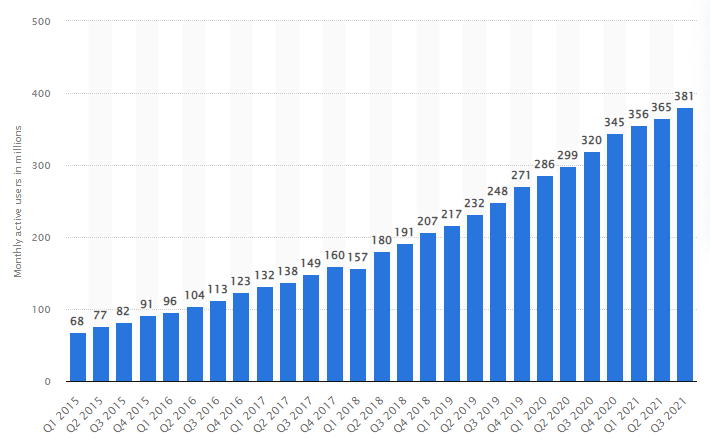

MONTHLY ACTIVE USERS (“MAUs”)

Total MAUs grew 19% Y/Y to 381 million in the quarter, up from 365 million last quarter and near the top end of our guidance range. We experienced double digit Y/Y growth in all regions with particular strength in Rest of World where performance was aided by the resumption of marketing activity in India along with above-plan growth in the Philippines and Indonesia. We also saw improved momentum across the 86 markets launched earlier this year, with outperformance led by South Korea, Bangladesh, and Pakistan.

Here’s their Q4 2021 Guidance:

We have maintained our prior Q4 guidance for Total MAUs, Total Premium Subscribers, and Operating Profit/Loss, and have increased the bottom end of the range for Total Revenue and Gross Margin.

Total MAUs : 400-407 million

Total Premium Subscribers: 177-181 million

Total Revenue: €2.54-€2.68 billion

Assumes approximately 250 bps tailwind to growth Y/Y due to movements in foreign exchange rates

Gross Margin: 25.1-26.1%

Operating Profit/Loss: €(152)-€(72) million

This is by no means a “DD on Spotify puts” and is meant to be a discussion space for Spotify ER as trading-floor gets a little off-topic afterhours

Pretty much linear growth with no signs of tapering off (which is what I’d expect to see if they had saturated their market the way Netflix has).

One big differentiator between Spotify and Netflix is that Netflix has no free option which means that anyone who wants Netflix already has a paid account. A large portion of Spotify users (more than half) are not premium subscribers so there is still room for them to grow on this front. You can see from this graph of their monthly active listeners (again by the millions) and compare this to their premium subscriber numbers:

Spotify is doing a great job at integrating itself with other platforms (for example it’s one of the default music players on Tesla cars, smart home hubs like Alexa / Google Home, etc.), for many of which I can see people paying premiums to experience ad free. As society continues to get “smarter”, Spotify’s presence will only get more ubiquitous.

Another big differentiator from Netflix is that Spotify is usable pretty much anywhere you need it. With Netflix, someone who doesn’t have the time to watch TV may simply cancel their subscription. But music can be listened to at the gym, while working, driving, on the subway. You get the point.

I am leaning slightly bullish here but waiting to see what other information others may have.

I’m inclined to agree with the bull case - Sirius mentioned strong advertising revenue in their earnings so I think that - along with subscriber growth - could bolster Spotify’s bottom line. I also think Spotify brand and retention is really strong so I’m excited to see how they discuss it this evening.

Yeeeaaaalp, me too. I just didn’t know that FB tanking after earnings and dragging SPY down would be the reason.

More artists are bailing on the platform, but not enough to have any meaningful effect on the stock price. I’ve read that podcast listeners and ad revenue have been up since Neil Young opted out.