Didn’t get to play this idea of AAPL calls on a not-that-hot core PCE, as I live on the west coast and the market opens at 6:30 AM for me so I’ve been sleeping in the open every day.

Anyways — I think the market is setting up for risk to the downside on a potential rug pull by the fed next week if they shut down pivot expectations at the JPow conference on Wednesday. After the usual FOMC green spike play, I’m thinking of leaning puts for the conference, with stop loss at JPow confirming dovishness.

Translation: “Jpow says: Pivot my a**, you overoptimistic lot; I’m coming for you. Have a restless weekend!”

Wages and prices continued to rise rapidly in the late summer, keeping the Federal Reserve on track for more interest-rate increases as it attempts to cool economic growth and bring down high inflation.

The latest figures add to a picture of an economy losing some momentum but still growing as the labor market, consumer spending and price pressures remain strong.

The employment-cost index, a measure of worker wages and benefits, rose 5% in the third quarter from the same period a year earlier, the Labor Department said Friday, as employers competed for workers in a tight labor market. The gain marked a slight cooling from the second quarter when the index rose at its fastest annual pace in records dating to 2001.

Household spending also rose briskly in September, according to a separate Commerce Department report Friday. Consumers have continued opening their wallet despite income gains that haven’t kept pace with inflation, which is near a four-decade high.

The Fed’s preferred measure of inflation—the personal-consumption expenditures price index—rose 6.2% in September from a year earlier, the Commerce Department said. When stripped of volatile food and energy prices, the so-called core index rose 5.1%, up from 4.9% in August—the strongest pace since March.

The new data didn’t change the overall inflation picture, leaving Fed officials on course to raise interest rates by 0.75 percentage point at their meeting next week and possibly entertain a half-percentage-point increase in December.

Haha sounds about right

Poor guy writes an article about the possibility of a smaller hike in Dec and the world hears pivot. J Pow, please choose your words carefully.

It’s strangely accurate to watch these numbers come out. Especially from the wage employment numbers. As since 2020 I have struggled to hire entry level positions. So what we did when we saw the signs on the marquee at Taco Bell advertising 15 bucks an hour to hand tacos out the drive through window was increase our starting pay. I’m strictly referring to entry level jobs. Washing cars parking then etc. we still to this day can’t hire enough people. Even out pacing fast food jobs and now becoming not so entry level wages.

In large part this was a reprocussion of Covid stimulus and having to essentially entice people to get a job.

However I am of belief that the tightening that has been partaking could get a glimpse of relief. We have seen .75 rate increases consecutively. We should be cogniscant that this was previously unprecedented. So for a shift back to the normal .25 .5 hikes would be largely considered as a pivot. Not sure it’s the right thing to do. Nor do I think it’s going to be effective. But I think with the slightly more dovish tone that’s been taken by the Old head Feds. If JPOW even hints at slowing of increases or not necessarily pivots but simple takes like a 45 degree turn. It could lead to some kind of insanely rip rally fueled by hopium and money on the sidelines.

This week is softer on ERs and primed on Econ news most of us believed that ERs would lead to next leg down. I think next quarter is when we see the real hurt coming. I’ll be watching for 400 level. To target January puts. But for foreseeable future we go up. Unless JPow pulls a full Jackson hole again.

I think if J Pow really wants to shut the dumb “pivot” crowd up he needs to throw them a curve ball they never saw coming (because everyone is hyper-focused on the interest rate increases) and say that they are going to increase the amount they are rolling off their books from 95B/mo to 150B/mo, with the possibly to increase even more. They have that tool at their disposal and they should use it, especially considering how overly bloated their balance sheet is.

That would be something! Would make the long end of bonds immediately flare up, even causing a gap down. May be a bit too harsh though, especially with midterms around the corner.

Perhaps he could say something like, “We’re removing forward guidance on terminal rate, from the current ~4.6%. It’ll go as high as it needs to.”? That will also signal that they don’t think inflation will slow anytime soon.

Honestly I don’t think they will mess with their balance sheet right now, even though I think they should.

Just saw this article on Bloomberg this morning (copy & paste since it’s short):

Goldman Sachs Now Sees Fed Rates Peaking at 5% in March

October 30, 2022 at 12:54 AM CDT

Goldman Sachs Group Inc. economists said they now expect the US Federal Reserve to raise interest rates to 5%, higher than previously predicted.

The central bank will lift its benchmark rate to a range of 4.75% to 5% in March, 25 basis points more than earlier expected, economists led by Jan Hatzius wrote in a research report.

The route to the new peak includes increases of 75 basis points this week, 50 basis points in December and 25 basis points in February and March, they said.

The economists cited three reasons for expecting the Fed to hike beyond February: “uncomfortably high” inflation, the need to cool the economy as fiscal tightening ends and price-adjusted incomes climb, and to avoid a premature easing of financial conditions.

I don’t think people really look at the fine print at what the fed publishes… There is still the 70% upper confidence number of around 6.2% I think… Obviously nobody thinks we are going that high, but that still gives ~1.5% of wiggle room before they do something beyond what they have been planning for. Obviously with inflation & unemployment not doing squat to help, they are certainly not going to stop short of the median target.

News has started to pick up more on the diesel shortage. This is a perilous time right now as demand is high while farmers harvest crops, not to mention going into the holidays there is an uptick in usage from all the goods to travel around from ports to people’s front doors.

On a similar note, heating oil costs have gone up quite a bit from what I have read people posting prices between last year and this year fill-ups. I wish I could find the page but I no luck going through my history.

I also got a letter in my natural gas bill the other day saying that they are forecasting prices this winter to be even HIGHER than last winter (shocker, I know). Keep in mind they increased prices last winter SIXTY FUCKING PERCENT from the previous winter (that’s not a number I’m pulling out of my ass, I actually ran calculations for my peak usage months Nov-Feb). They weren’t very specific on how to apply the number they gave to the line items on the bill, but it looks like probably a 25% increase over last year’s prices (if not more)…

The big question heading into the Fed meeting is about what, if anything, Powell will say about December.

Economists say that is in part because of some ambiguity over the Fed’s reaction function around any step down to 50 bps—even if the estimated terminal rate is rising.

“Any step down” for Dec suggests 75bps is the default, and he goes on to clearly note that the terminal rate is rising - a first, I think, from him.

Love this important conversation here on this thread. Lots of great perspectives.

Im not sure what to think of this guy yet, he seems to change his tone quite a bit, maybe he really is a fed whisperer.

Regardless, I think he made a fair point this morning on face the nation about the lagging effects of monetary policy.

FWIW, not to make this overly political, but as election night approaches I’m not terribly surprised to see lots more semi-informed clickbaity articles re: domestic energy production, SPR releases, and similar.

It wasn’t meant like we will run out in 25 days. It’s just pointing to the fact that supplies continue to tighten, demand continues to be strong, and hence why prices keep going up. Yes, distribution channels are borked right now, and any further disruptions / delays only will make things worse.

CEO of UPST speaking about rising defaults in yesterday’s ER.

“The most recent index level of around 1.7 tells us that Q3 environment produced 70% more defaults than we would expect from our barrower base in a long run normal macro environment”

“This number is approximately 20% higher than we observed when we last reported earnings in August”

I want to share my trading strategy and circle back around to an opinion I shared in Aug about a smaller CPI print and how the market would most likely react. In that same post below I also shared some thoughts on how a recession has more to do with consumers financial health, credit impulse, and company evaluations vs “peak inflation”.

My opinion hasn’t changed and think we may be currently sitting in that dislocation. The issue with the hyper fixation on the fed is that they serve a large part of the economic equation but not necessarily from the ways you may expect.

IMO the fed is not the main character of this story. They do play a significant role in bringing down inflation and inflation does help then hurt the economy but elevated inflation alone is not responsible for the all of the economic challenges we face. Take a look at inflation in the last 2 recessions.

Peak inflation Dot Com recession

Mar 2000 @ 3.8%,

Official start of the recession Mar 2001

CPI @ 2.9%

Offical end of the recession Nov 2001

CPI @ 1.9%

Peak inflation GFC recession

July 2008 @ 5.6%

Official start of recession Dec 2007 (Announced Dec 2008)

CPI @ 4.1%

Official end of recession

CPI @ -1.4%

In both examples inflation was at play but not the main driver of the economic contractions. Inflation in both cases peaked and a recession followed. Just like every recession in the last 100 years. 2022 isnt any different in real economy as far as headwinds go, Id actually argue they are worse but inflation this go around is and has been a bigger problem.

We dont know how sticky inflation will be or if we have actually seen it peak. IMO it probably has, but that obviously doesnt make me long term bullish for the broader market in the slightest. Outside of select sectors ill be thinking about going long when 3 things happen.

#1- Fed Pivot (not this smaller hike/pause bullshit) a real pivot meaning cutting rates.

#2- Earnings - Ill only be going long in companies that are trending in the right direction fundamentally. Cant have one without the other.

#3- Economic indicators move bullish.

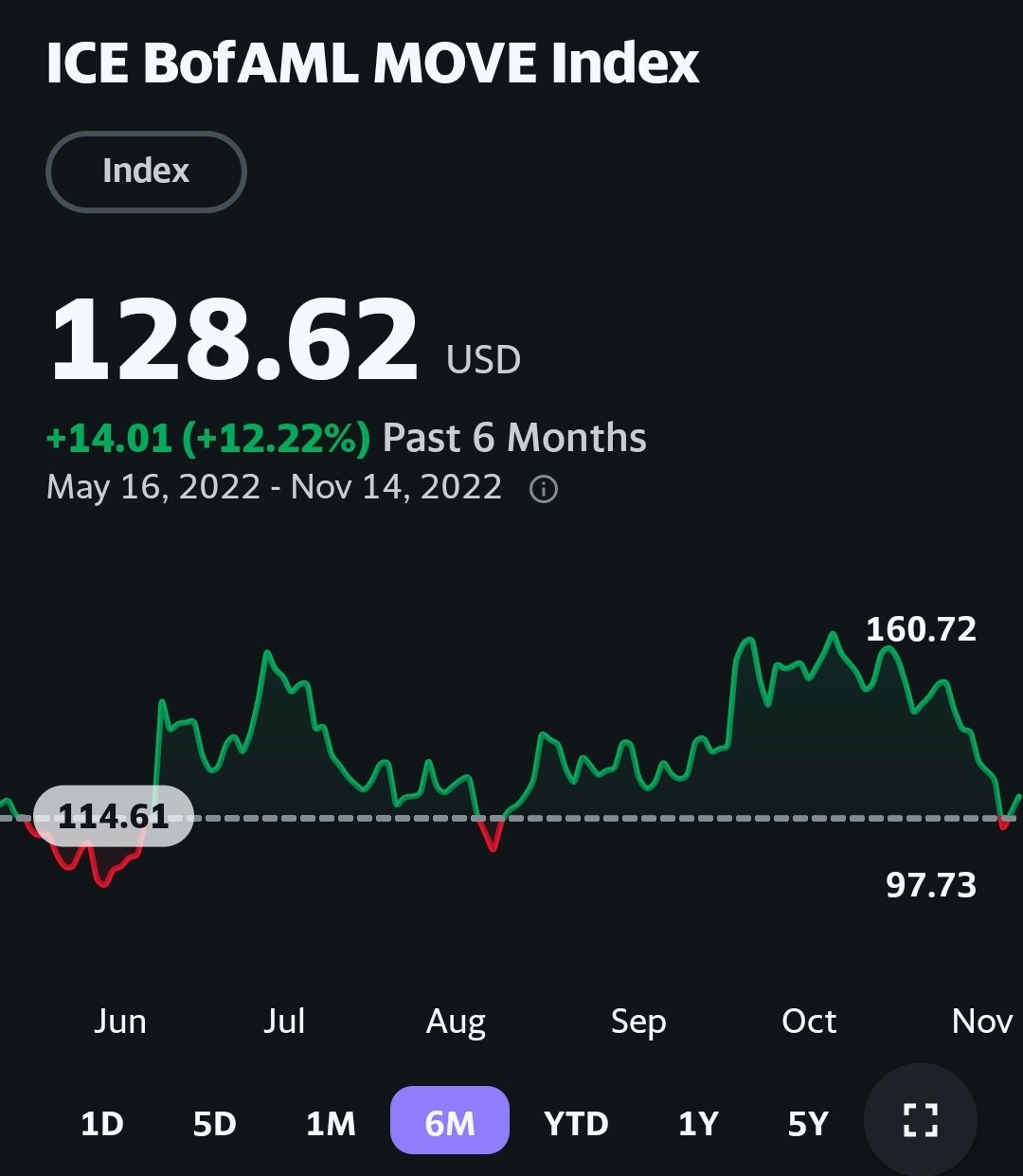

Until then, the strategy I posted in TF is designed to move with the market. Taking advantage of big moves. SPY, QQQ, HYG, GOLD, & SLB are my main tickers and I chart them daily. Im always in both directions meaning Im always hedged. As the market moves I move positions around (ideally this means taking profits) based on trend, individual movements, and my key indicators. Yields, DXY, VIX, HYG, & AAPL.

Yields- Short term I look at how they are moving then look at the relationship between different maturities, mainly front end vs back end.

DXY- Dollar (Big +/- moves in QQQ, GOLD, SLB)

(Play directly in UUP for short scalps)

VIX- (Use this as a temperature gauge)

(Play directly in options or UVXY)

HYG- Highly correlated with SPY, creates divergences intrayday that are my highest win rate trades. Also a good temperature guage for the real economy.

AAPL- High weight in SPY/QQQ, also a great temperature gauge on broad market movement and risk on/off sentiment.

While watching data, earnings, news, etc. I then I look at technicals, mainly fib lines, MACD, RSI, and volume.

Risk management/Capital Preservation is guided by hedging, position sizes, dte, and strike.

If we get a strong trend Ill scalp select names or indexes when I can.

Its not perfect and requires a decent amount of management but it has been working for me for the last few months so I suppose Ill continue to play it until it doesn’t.

Hope this is helpful, good luck and stay cautious out there friends.

Keeping an eye on this indicator to see if the last few days movement continues to trend. Not something I would trade on its own, but a piece of the puzzle worth paying attention to.

Excellent communication @TheHouse , really appreciate your time in contributing this for us all. I’m in total agreement with you. Picked up several SPY and QQQ puts for Feb/Mar/Jun 2023 a few days ago. Planning to average down if we push to 410 or 420 or even 430.

Unemployment is a lagging indicator while PPI is a leading indicator.

PPI is inflation for producers of products, or the price before it gets to the consumer. This points towards lower CPI prints to come. The market is reacting to this only at face value. Inventories are fine, its the consumer that isnt. I think there are significant dark clouds above the US and world economies right now and the equities market is balls deep in this narrative that the fed will eventually pivot and save the day. This tells me most people forgot that every recession in the last 70 years has involved a pivot and the fed cutting rates. Dot com or the earnings recession is imo the closest example of the type of recession we have or will have but sprinkled with a little bit of early 70’ stagflation and a dash of 08’ asset bubbles, oh and lets not forget a dash of tulipmania because we are selling cartoon character jpegs for obscene amounts of money while buying the dip on the latest meme stock that has never made money.

Here is the fed funds rate for the dot com recession.

You will notice they first cut rates in December of 2000.

This is what the market looked like for this same time period. Blue line is Dec 2000 when they started cutting rates, yellow lines are the official recession dates start to finish and the recession announcement date is purple.

So when a fed pivot is actually on the table Im going to mindful of this possibility.

And a few additional things I wanted to mention,

I alot of times dont know what to say when asked about timing, I believe we are in an inflationary slow growth period that will lead to a deeper contraction. Or put another way, stagflation leading to a recession. All of my trades this year have been from this perspective. I think we are currently sitting somewhere in between inflationary slow growth and a deeper contraction, from there as Ive mentioned before I like playing “legs”.

Im never suggesting anyone make any trades based on my opinions or follow me into any trades. Im just sharing thoughts on what I see in the economy and sharing how Im trading it. We all have our own personal risk tolerance and hey I like taking risks every once in awhile, but If you go blow your load on FDs, I wish you luck but thats on you not me.

As always @TheHouse we all appreciate and value your perspective and insight. But as I’m sure you know with enough conversation we have had there is always the other side and what could be the case.

I strongly believe but not wholeheartedly convinced just yet that what you portray above and in many of your insightful posts or commentary is accurate.

My very simple one hesitation here is unlike the above mentioned examples of recessionary climates or periods of recession. We are currently in a state of growth still in many aspects. 2020 caused an economic collapse for many for several months or a year shuttered business mass layoffs government stimmys. The rapid explosion coming out of that is what I think has largely caused many of the inflationary issues we are facing it wasn’t natural growth it was a straight rocket from the depths of earth the economy went into with the global pandemic portrayal and fear.

A few differences in current times many of the inflation issues pertain to supply chain backlog wether it’s auto housing/construction. We all likely remember the spike in lumber pricing. When building was on a rip. Or we currently are aware of the energy crisis due to war time or non drilling OPEC etc. it’s all been a comedy of errors that has caused this situation that’s currently unfolding. This has all been unprecedented in our lifetimes.

My cautionary statement would be the rapid growth we have experienced has to coinicide with some slow down. But does it really represent a slowdown to pre covid levels ? That’s where my hesitation comes in. Are we in a better spot now than March of 2020? I’d venture to say yes as we value and look at these segments or companies. Demand is still apparently strong the US consumer is resilient as ever right now. Jobs are still out there. Companies are hitting their EPS and largely with exception of outliers still profitable.

Essentially JPow shouted this shit months ago while he was still saying inflation was transistory. That the US economy was in a strong position to obtain a soft landing. Although it thinks it’s unlikely myself I have started to sway to the direction that the essential curve has been flattened and we are on our downward slope of this inflation. By no means do it think we are out of the woods but I do feel like a “soft landing “

Is more possible than it was 5 months ago.