Well written as always. I do tend to agree that the current environment we are in is one of something non of us have ever really witnessed. Global virus resulting in shutdown of the world economy at the drop of a hat. Resulting in a steep decline in the labor market. Followed with not just inflation coming out of it but hyper inflation at that.

So what we are living is a once in a lifetime scenario. I have mentioned before that we have to be cogniscant of comparison to 08 or previous economic times of turmoil. This is its own animal. As we see the inflation slow but labor still tight with exception of vastly unnecessary high wage tech jobs. There is still a driving demand for hourly to middle class wage earners.

The problem with this aspect is those are largely the drivers of inflation. As we can not from the stimulus environment that fueled the hyper inflation. Frankly most lower to middle class unfortunately leave paycheck to paycheck and many above their means. So that leads to more earnings or pay more spending.

However I think the best case scenario and I’m no economist. If inflation can continue to cool and labor stay tight it is the best case scenario to avoid a dramatic recession. Strong labor market almost always signals strong economy. One thing I think about a lot is the most significant cause of this inflationary cycle was the supply chain (which really was never an issue other than over supply in previous climates) as that is reeled in it has caused some loosening in pricing.

My fear has become the wage inflation related to the hourly occupations. As many states raise minimum wages etc and still relatively hard to find entry level workers it creates competition much of what we saw coming out of the shutdown that has yet to correct itself.

Essentially I think we are looking at something different than we have historically. In the months coming we will find how this effects the broader market.

Inflation may be unavoidable in order to close the gap between the haves and have nots. We know the current administration sees the growing income gap as a problem and has taken steps to narrow it. You cannot simply steal from the rich and give to the poor so instead stimulus checks are given and minimum wage is increased. How can you avoid high inflation in doing this? When you give a dollar to the lowest income earner, it gets spent, and usually more than just that dollar.

Re: changes to the labor market. COVID May have changed it permanently, but only as it pertains to the boomers retiring. What may be a bigger impact on labor currently is the decreased labor participation rate of 18-25 year olds. As stimulus and COVID incentivized them to stay home, they continue to do so. But that is not a permanent change and they will eventually return to the workforce. When they do, the unemployment rate will increase, and it will likely increase quickly. And unfortunately it will be at the same time recession hits and parents are financially struggling and credit card payments are due. I believe parents/grandparents are subsidizing 18-25 year olds at historic levels.

I agree that we’ll likely see an over tightening by the fed and we’ll see a very hard landing. Unemployment is not the gold standard. I’m surprised to see so little about total employment which has declined and shows the true increase in unemployment. I must admit though that it’s taking longer than I expected for the hard landing to occur. Not sure on timing. It was a huge bubble so its taking longer to pop.

The popping of the bubble also blunts steps taken to narrow the gap between the top 1% and the bottom 20% as recessions hit the bottom much harder than the top.

Putting this here since it is relevant. Truflation is an independent inflation index that attempts to estimate the “true inflation” by tracking price changes across millions of items in the economy.

There’s a guy on Fintwit that’s come up with an interesting model that seems to be pretty accurate across the last 6 cpi prints.

This needs to be double checked as I see there is a lot of confusion in the comments regarding trueflation’s retroactive data updates.

Basically all this is to say to be careful if you’re positioning bullish for CPI. I don’t endorse puts but here’s a datapoint that analyst consensus and market expectations may be a bit too optimistic.

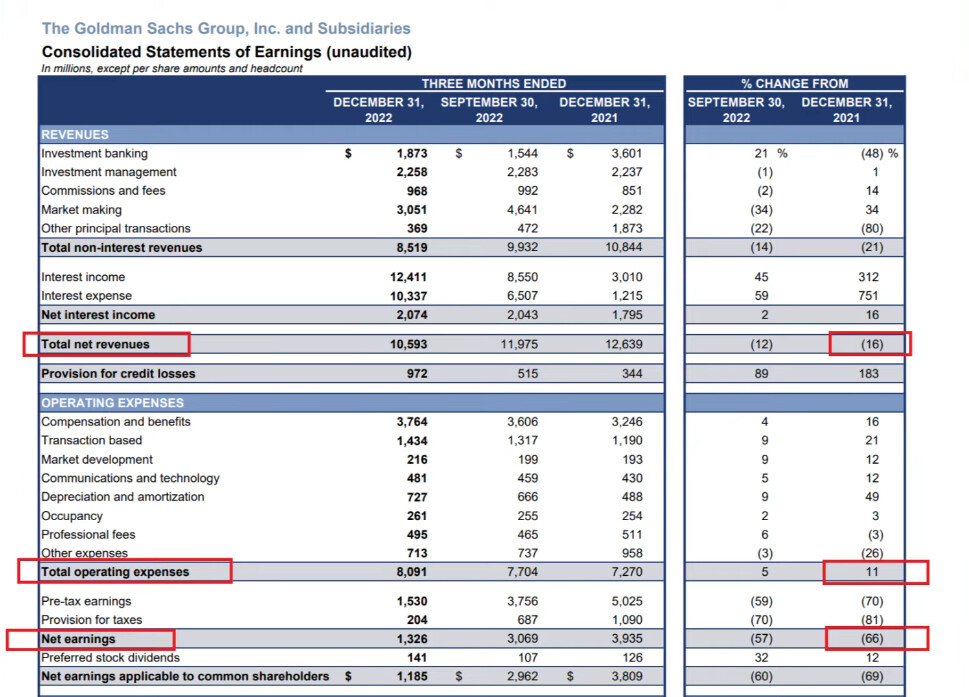

Highlighting some points from the new Maverick video on the $GS Goldman Sachs earnings report that relate to this thread.

[size=4]Lay-offs and unemployment[/size]

Goldman is facing the exact reason to lay off employees: decreasing revenues + increasing operating expenses = negative net earnings → decrease expenses. Everyone’s favourite way to decrease expenses these days is to lay off more employees.

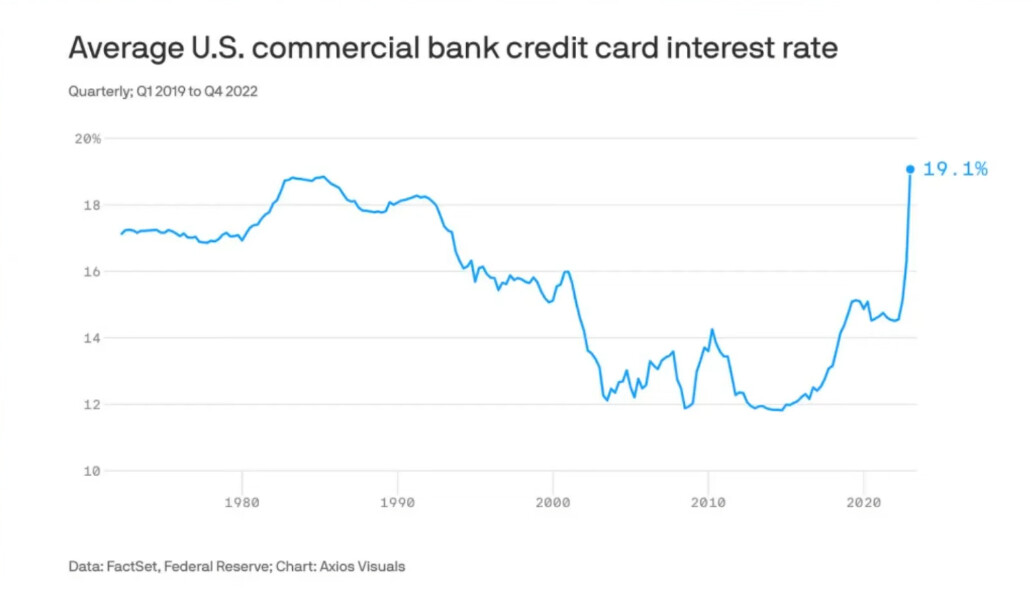

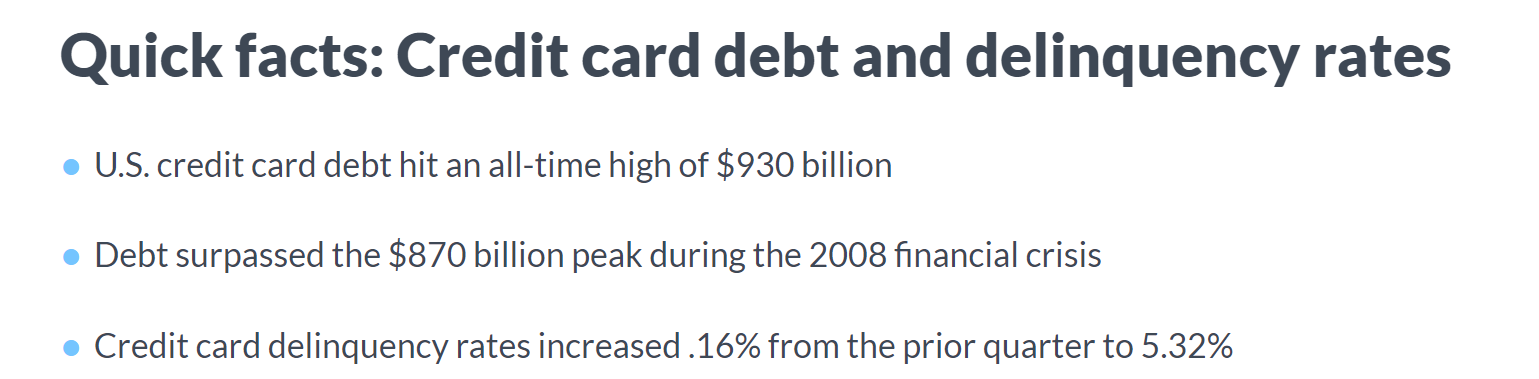

[size=4]Bubbling consumer credit[/size]

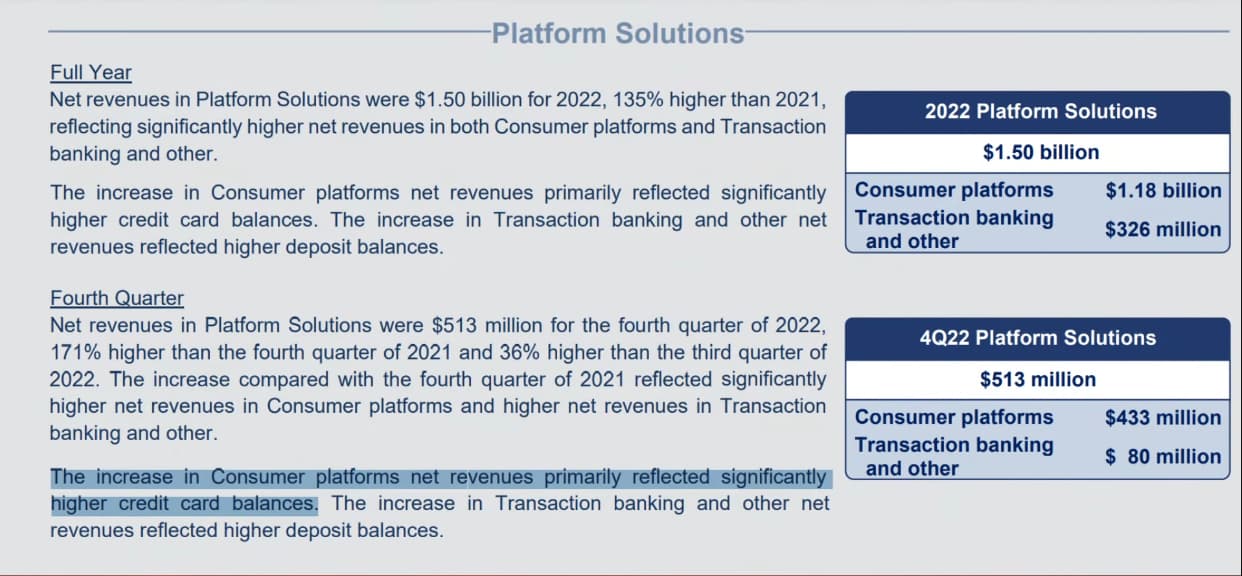

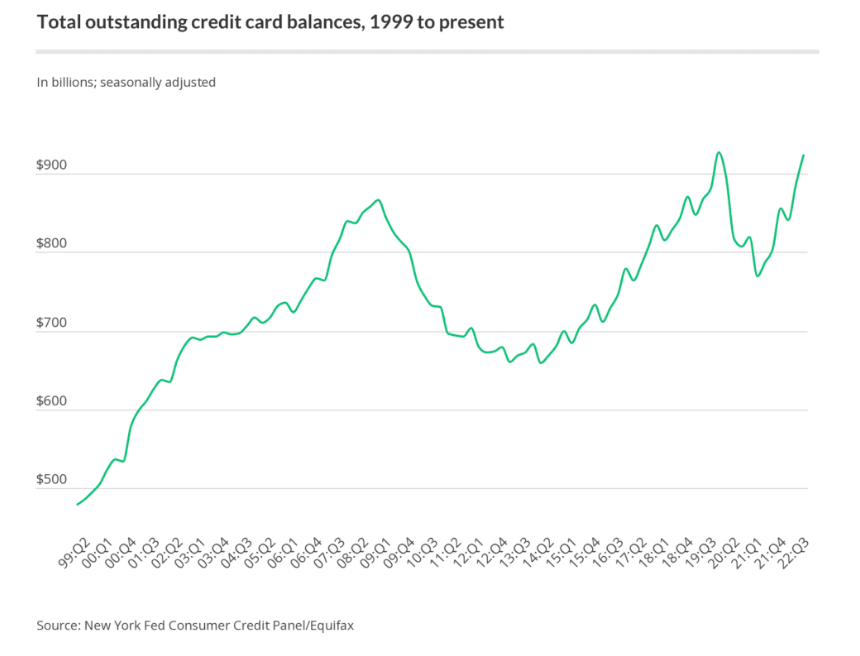

The only positive segment for $GS was Platform Revenues. However, the primary reason for growth was “significantly higher credit card balances.”

Nevertheless, noticing a few interesting countertrends popping up.

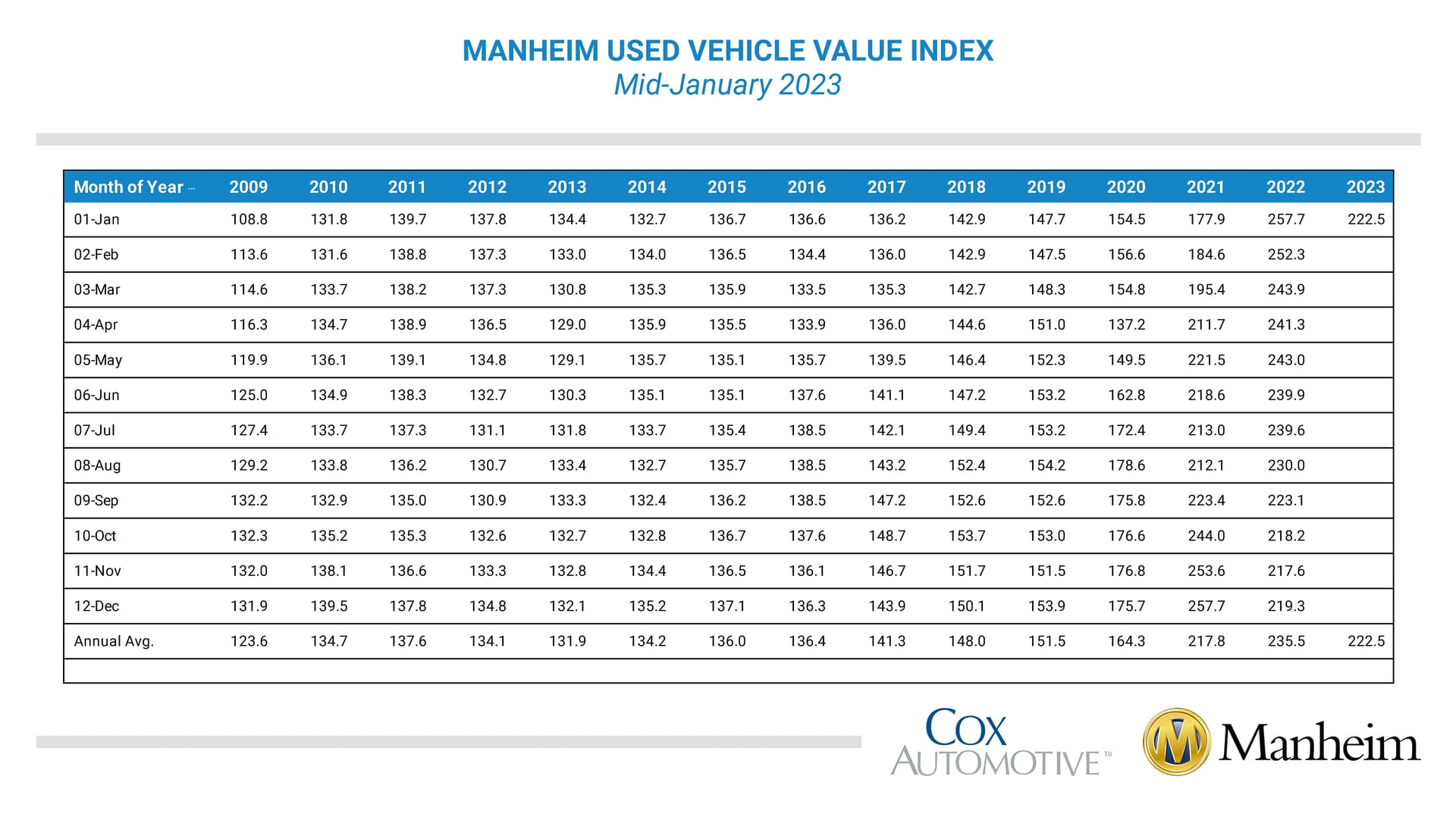

The Manheim wholesale used car index went up in the first half of Jan 2023. This is wholesale prices and not retail, but I wonder if and when the effect will carry through. (@jjcox82?)

USD seemed to be plateauing after a drop for most of Nov, but has continued with the decline over the last two weeks. This makes imports more expensive - we do not seem to have the good fortune of “exporting inflation overseas.”

These data points could be nothing more than noise in the overall downward trend. But something to keep an eye on… as if it turns out inflation is being stubborn, things might start breaking as markets pull a Crazy Ivan.

I was just talking about this last week with some guys at work. Wholesale prices have inched back up this month for sure. They haven’t returned near to the insane highs they were.

This is pretty typical for this time of year as automotive business returns to normalcy of pre supply chain woes.

January and February typical see a rise in wholesale pricing as used car dealers compete for inventory for the spring especially tax refund season. March is perennially one of the best Retail months of the year.

This Forbes article was a great read. It summarizes the historic rate hikes and rate cuts and the macro environments at the time causing the hikes/cuts.

I highly suggest you read it from bottom to top for the chronological order.

Couple observations while reading this article:

A fed funds rate of around 5.25% to 6.00% has been a comfortable area for the fed to stop raising rates, historically.

These cycles of rate hikes and rate cuts were very interesting to read. Basically a never-ending tug of war between the fed and the economy.

Implication for today’s economy: I believe the fed when they say “higher for longer”. I think they’ll go to at least 5.00% before deciding to pause and assess, with no rate cuts in 2023 as they’ve forecasted over and over despite the market’s disbelief.

Decent write-up that argues we are only in the beginning of some rough times ahead on the macro level. Some good talking points and some particularly interesting outlooks with gold & silver.

Had covered how prices of things are going up in a previous post, so will not repeat.

Where does this leave us? Well, markets are still pricing in a soft landing, or “immaculate disinflation,” as some are calling it. But … if inflation doesn’t go down fast enough yet growth slows to a halt, we’re back to staring the title of this thread in the face, again.

Economy is slowing as per most economic data points lately.

Inflation is “slowing”, but still way above target, e.g. Core PCE at 4.4% and CPI at 6.5%. Inflation data is also still positive MoM with the exception of a single minuscule negative CPI MoM reading.

Aggregate demand has already started to show itself in the housing data, as you pointed out (as well as used cars). To me it looks like if the fed eases too prematurely whether that be in their words/guidance or in their actual rate hike/pause/cut decisions, we’re looking at high risk of inflation popping back up, and I think the fed knows this.

JPow has said they would rather overtighten than not do enough, because they always have the tool to cut rates later to re-vitalize the economy. I think the fed is facing this situation #imminently. JPow’s tone tomorrow might be a pivotal moment here for markets.

One day, we’re surfing along higher highs, propelled by animal spirits, CTA flows, and short covering rallies. The very next day, life comes at us fast, with macro data delivering a one-two punch.

NFP came in absurdly hot pre-market (517K vs 193K), with wages continuing to rise and unemployment continuing to fall. Then at 10am, ISM services PMI surged to 55.2 in January, way above the consensus expectation of 50.5. Services new orders index rocketed to 60.4 from 45.2. (Values over 50 are expansionary for both indices.)

Both the labor market and the economy remain quite strong. Almost impossible to see how inflation returns to 2% in this context. Next CPI print is in 11 days. If it doesn’t show up there, it will very likely show up in March.

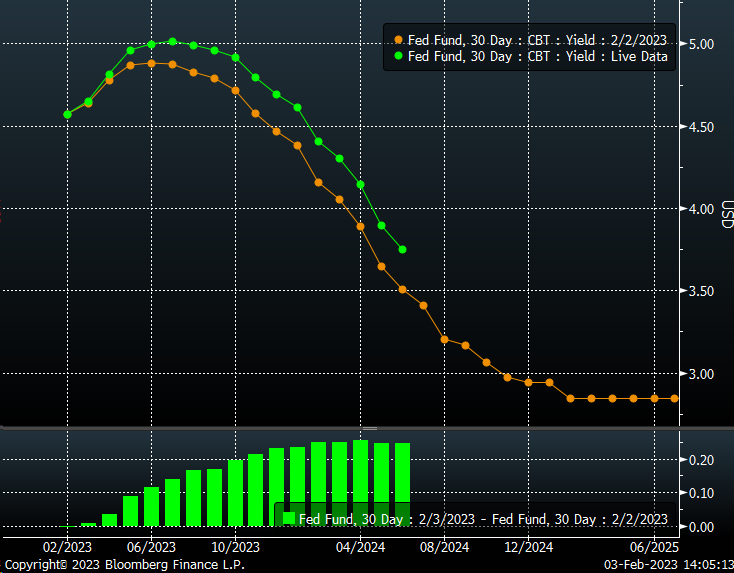

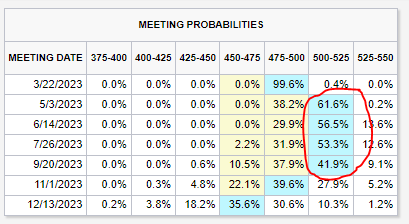

That red bit below… yeah that wasn’t there yesterday. Market has abruptly decided an additional 25bps now makes sense in May, after being very sure Mar was going to be it.

We can continue the discussion on what happens to the market as a result in a different thread.

The January Manufacturing PMI registered 47.4 percent, 1 percentage point lower than the seasonally adjusted 48.4 percent recorded in December. Regarding the overall economy, this figure indicates a second month of contraction after a 30-month period of expansion. The Manufacturing PMI figure is the lowest since May 2020, when it registered a seasonally adjusted 43.5 percent. The New Orders Index remained in contraction territory at 42.5 percent, 2.6 percentage points lower than the seasonally adjusted figure of 45.1 percent recorded in December. The Production Index reading of 48 percent is a 0.6-percentage point decrease compared to December’s seasonally adjusted figure of 48.6 percent. The Prices Index registered 44.5 percent, up 5.1 percentage points compared to the December figure of 39.4 percent.

Economic Contraction + Increasing Prices = Stagflation. The question isn’t whether we will experience stagflation at this point, it is when and for how long. The market currently believes it will start this quarter and last for about 3-8 months. We should have more insight into how accurate the prediction is after the next CPI print.

I should have included this my prior post. Apologies for the double post. This incredible thread all started because some of the smart people in this community were concerned that stagflation could lead to a recession. While that can still happen, stagflation does not automatically mean we are headed for a recession. A prolonged period of stagflation or a more accelerated economic contraction is what could lead to a recession. The point is, don’t assume that because we are going to experience some stagflation that we are going to be in a recession. The Fed (and I can’t believe I’m saying either) may actually achieve a hard landing that does not break the economic airplane and allows us to pull back up and keep flying terrified but relieved.

So please don’t take my comments to mean there’s going to be a recession. It will all come down to the duration and movement both into and out of stagflation that will determine whether (not when) a recession will happen.

Here are two threads that argue that neither the NFP data nor the Services PMI data were “that bad”. Thus, somewhat contrarian to the market reaction, especially reaction of bonds and USD.

While I do feel like he might be missing the forest for the trees in both, it is important to consider both sides carefully. Sharing his specifically and not other FinTwitters who have a similar opinion because Bob consistently shares compelling and exhaustive data that has helped me make sense of what is going on.

Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) increased 2.5% in January compared to December. The Manheim Used Vehicle Value Index (MUVVI) rose to 224.8, down 12.8% from a year ago. January’s increase was driven in part by the seasonal adjustment. The non-adjusted price change in January was an increase of 1.5% compared to December, moving the unadjusted average price down 11.0% year over year.

… we initially estimate that used retail sales increased 16% in January from December and that used retail sales were up 5% year over year.

The #1 and #2 largest call option buying days in the history of stock market both happened just last week. Higher than any point in peak meme days. This is with odte options continuing to become more and more popular. Has a 1600s tulip feel to it.

This Icahn trade is interesting.

Say what you will about the trade itself, I dont know what to think about it, thats all speculation at this point I think its more interesting that it comes from him.

This is a large unusual short term bet made by a guy that in his career has generated over a Trillion dollars in wealth for his clients.

CPI and mopex next week while we continue to make our way through earnings. It looks to me like we could have a possible reversal on our hands but it also looks super obvious which makes me pause. For this reason Im using neutral strategies on range days(Thanks to everyone that shares advice here on option strategies), closing positions quick on strong directional days (Both directions), and using longer dated spreads for swings (which will be limited until better idea of market direction.)

These are the tickers im playing downside on (Only when broad market is moving with a strong individual trend)

COIN

TSLA

ENPH

HYG

GS

Watching close (to trade)

TLT

CCL

UUP

GOLD

ITB

Stay cautious out there friends and happy trading.