Wanted to share two thoughts as we go into another potentially rather explosive week. When things can get quite confusing, helps to keep the big picture in mind. This is one version of the future of course; please do share what you think.

Expectations of market recovery contingent on Fed pivot

Part of the expectation for a market recovery soon is based on the Fed pivoting.

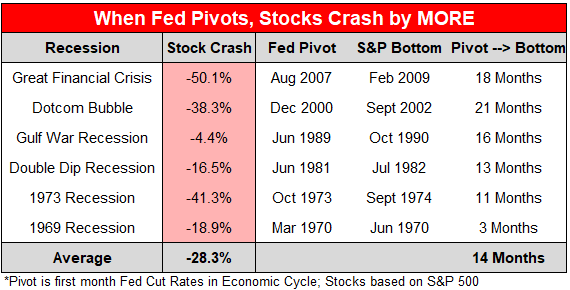

The thing is, if the Fed pivots it will very likely be because there is a recession. In which case, markets will go down to price the recession in, which it has not done at all yet. That rates will go a few points lower may not help much in that case.

Now, if there is no recession and/or noticeable hurt to the labor market, we can expect core inflation to keeping running somewhat hot, given wage-price spiral and all that. Which then means that rates will remain high for a while. Which, in turn, will keep markets depressed.

Thus, feels like we’re in a bit of a “depressed market if there’s a pivot, depressed market if there isn’t one” situation.

Incidentally, inversions are abnormal and we’re around a massive -0.5% right now, so we should expect the long end to eventually catch up and be higher than the short end. If there is no pivot, that just means even more discounting for risk assets as the long end has to rise a lot more. (Buying TLT is a play if one believes this.)

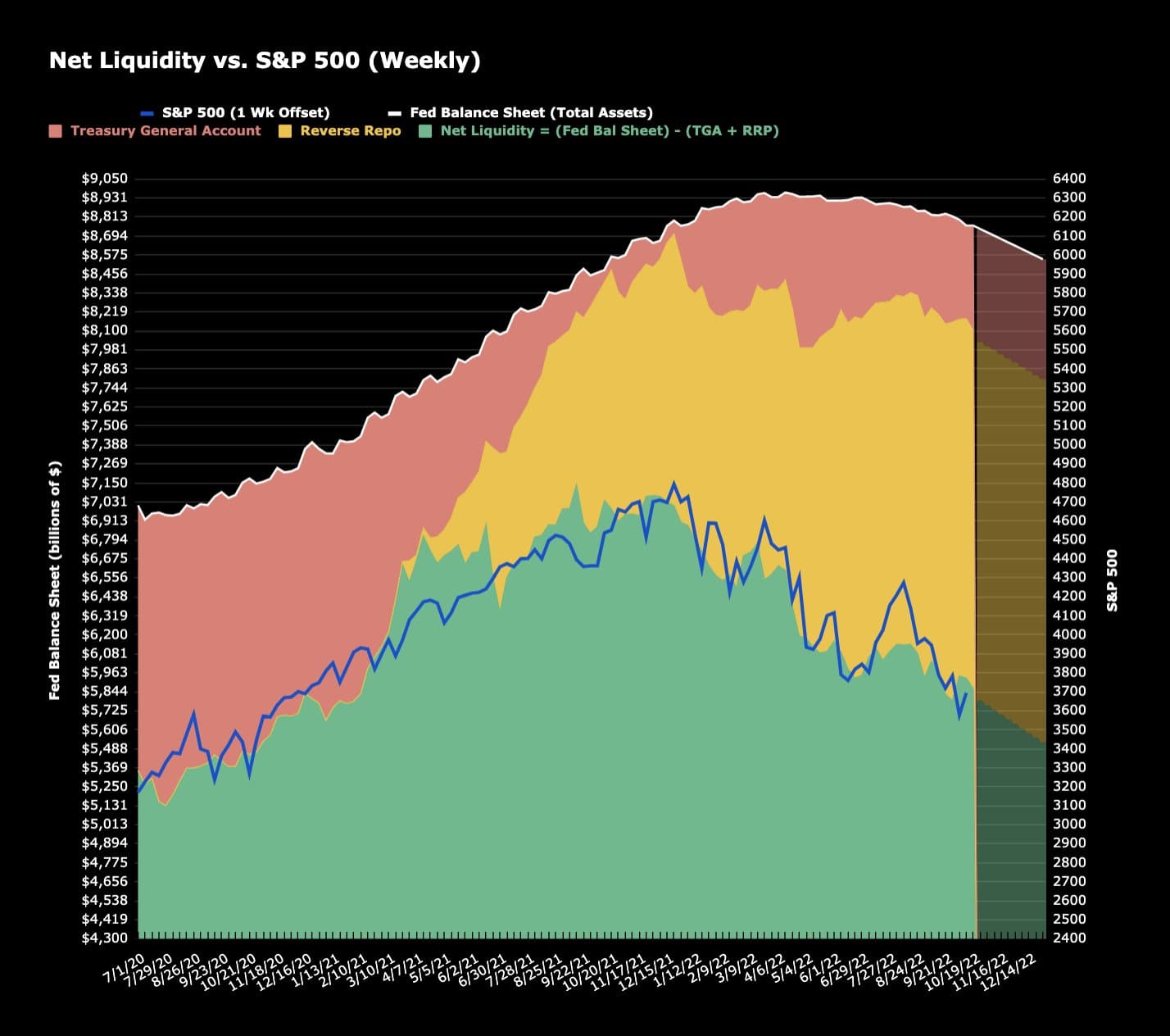

In the event that something breaks, I think the Fed will first try to control it by providing unlimited liquidity through things like the reverse repo facility or buying bonds, because messing with rates disrupts their inflation mandate. This is perhaps what the Treasury Dept was trying to get a feel for when they sent the survey out about buying bonds from the secondary market (vs primary, like how the Fed does it now).

Also, one of ways this episode is different from previous episodes of economic regime change is the Fed is raising rates into a recession. That puts us in rather uncharted territory.

Associated market corrections

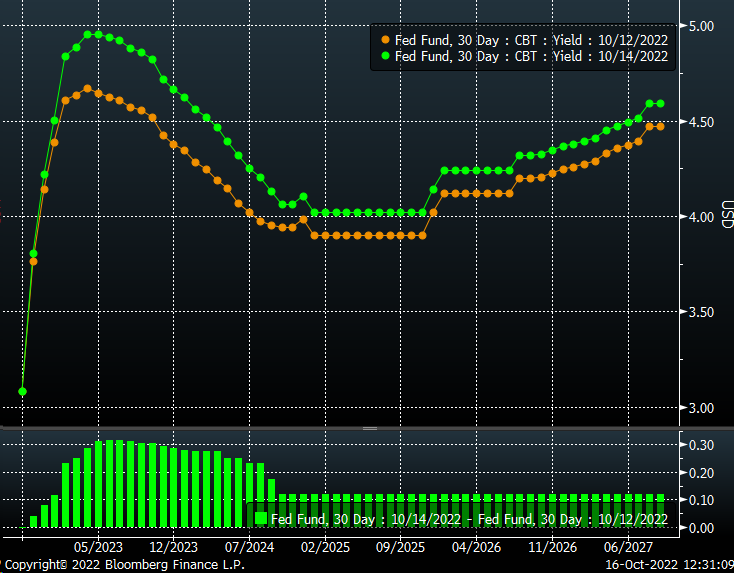

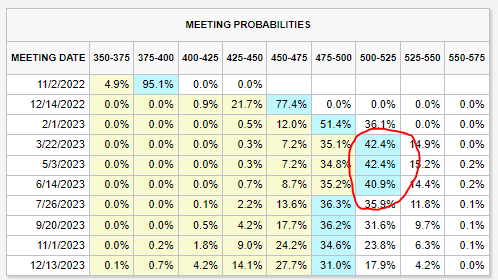

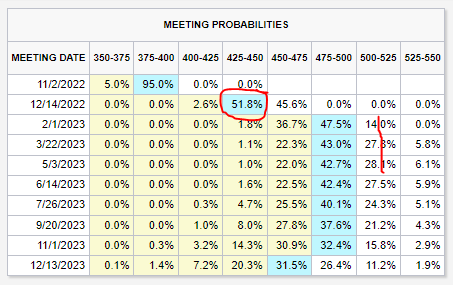

As we can see below, Fed Fund rate expectations have flared up in the last two days, thanks to the CPI print. (This moves in parallel to the yields I noted above.) As we know, this will effect equity pricing.

(Source)

People have a choice to earn 4%+ on risk-free government bonds now, that is soon to be 5%. Historically, there’s been 100-200 bps risk premium for equity compared to bonds. Current S&P P/E is 18. So that’s about a 5.5% yield ( ~= 1/18). Imagine what happens when bond yields hit 5%. People - retail and institutions - will switch from equity to bonds en masse. Many are starting to do so already.

Also, this is before any earnings adjustments. If earnings are bad, P/E goes up even more! Which means even more of a correction. Considering all this, fair value of S&P is probably quite a bit lower than where we are now.

This does not mean that this will happen immediately. Q3 earnings are key. If earnings - and more importantly, guidance - disappoints, we could begin this leg down soon, helped along by rising rates. However, it is not clear how bad earnings will be, if at all. We have seen how companies are still adding jobs in the aggregate, and consumer spending is still quite strong. While layoffs may not begin until earnings take a hit, consumer spending should be a leading indicator. This suggests that we might have to wait another quarter for this earnings effect to occur. Maybe even two.

All in, I find it difficult to see how the stock market becomes bullish again anytime before late 2023. Though there’ll certainly be bear market rallies. And if Q3 earnings are not bad, we might even have a Santa rally into the end of the year before we revert back to the overarching bear-market trends.