The purpose of this thread is to house the broad economic discussion that we have been seeing largely take place on trading-floor. During the Ukraine situation we had a central thread that spun off multiple discussions and ideas. Those ideas were taken to their own threads and traded on.

This thread exists to capture the spirit of that “main thread” for discussions on the market as a whole and opportunities that may arise from the current economic conditions. We have some smart people here and I’d like to see more of their discussion front and center so that we can all try to figure out how best to profit from the opportunities together.

While obviously a small sample I’ve been paying attention to the crowds locally and the state of stores/restaurants. I live in Southwest Florida which was one of the earliest and hardest hit places in 2008 and given the COVID migration here I don’t see why that would change much. It’s a bit eerie but it’s starting to look exactly how it did in 2008 with massive housing developments popping up in multiple locations.

Hit Costco last night and was actually surprised by what I saw, which was merchandise everywhere:

These extra pallets on the right hand side are all the way throughout the outskirts of the store. I’ve been going to this location for years and this is the first time that’s happened. I asked an associate if it’s normal and was told “no, we don’t ever have this much extra inventory, we’re running out of room to put it”. However in happier news, the avocados have dropped from the astronomical $10.00 a bag I was paying, to a more reasonable $6.50

Gas peaked at $4.90ish at this Costco just over a month ago, it was $4.19 now:

I’ve said a couple times how our local shopping centers which were overrun a couple weeks ago are ghost towns now by comparison. I spoke with two owners of restaurants I go to and was told that business has sharply fallen off. Online you can see it reflected on a grander scale by the sentiment in the meal delivery subreddits which are increasingly full of people talking about the lack of orders and how what orders they are getting not tipping anymore:

I’m sure someone can clarify but I believe yesterday we also had some data come out that is backing up the theory that demand destruction is occurring. If this is the case, what types of things should we be looking to play? Meal delivery earnings puts seem potentially profitable? Who is the hardest hit? Let’s discuss

I am not seeing this yet in my similar frontier market (Phoenix and surrounds) but will look harder. Restaurants still seem full (or as full as they typically are in June/July offseason), Ubers have still been very expensive and hard to call relative to 2019 and earlier. Same deal in my travels to San Diego, Los Angeles, Portland and Seattle over the past few weeks.

My hunch is that the other foot to drop re: reduced consumer spending (or at least the observation of it) will come in mid- to late-August when kids are back in school. This summer might be a lot of families’ last hurrah - doing the big trip they had put off due to COVID - before tightening the belt.

With the collapse of Ass Guard, I feel obligated to contain my musings here. I’ll even make some suggestions of specific tickers/sectors to watch.

But yesterday’s discussion (to summarize) was mostly me presenting a “less than full-port Bear” case aka some limited upside case to the 2H of 2022 given some indicators. The strategy here isn’t to preempt any market uptick (unless you are a long term investor, but we’re all FD option degenerates here) but to be ready to act if there’s a rebound. Along these lines, I’d look for areas that have been beaten down but could recover quickly if a recession does not look likely or at least will be a mild one - that’s speculation for another post. Warning - very long, autistic post ahead.

Resolution of supply chain, demand collapse, and impacts thereof

Back to Conq’s observations and what they’re signaling (to me) - I’m a firm, firm believer that the majority of inflation was caused by unanticipated and far-reaching global events - first, obviously, COVID and the widespread impacts of shutdowns and the impacts to the entire supply chain, and then the war in Ukraine. Yes, other factors likely impacted the rise in inflation, but ultimately there was greatly diminished supply and increasing demand and as a result, rising prices across the board.

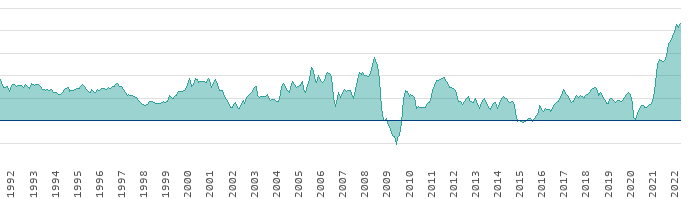

Now, unwinding issues due to supply/demand imbalance takes quite a bit of time - if you start all the way at commodities, there are so many steps to final goods (transport, manufacturing, additional logistics, retail) that bottlenecks at any area could still impact final pricing and availability at goods, so a number of indicators to look for. But at the end of the day, it starts with commodity prices, so that’s one leading indicator I’m using for monitoring inflation. You’ll notice based on the following two graphs that commodity prices over time do correlate closely with consumer inflation with a multiplier (IMO) due to COVID starting in 2020.

So we’re seeing evidence across the board of commodity prices dropping sharply in the last month in the US:

Alright, what about up the supply chain? Well, since supply became scarce and demand was high, companies were incentivized to build inventory to insure against future supply chain shocks. This was most notably seen in the semiconductor space - we’ve all heard about chip shortages, etc - but this was a big factor for retail and wholesale as well. And of course, there’s data to support this:

Okay, so inventories are building. But at the end of the day, the prices are still high, right? The CPI report that ultimately forced the Fed’s hand indicated the highest inflation (8.6%) since 1981. So all the way to us consumers, prices are still high, and as a result of that, retail spending has actually been dropping:

So what’s that all mean? Well, supply/demand imbalance due to COVID has likely completely inverted due to resolution of the supply issues, inflation, and now correlative decreased demand due to higher prices. What that looks like to me, then, is likely that inflation has peaked - if you’re a retailer, excess inventory is actually a problem, and you’re going to have to move it somehow - discounting prices, selling to discount resellers, or trashing inventory. This does also impact the bottom line of retailers - just see Walmart’s drop - but at the macro level, should impact inflation. This is why I don’t buy into “persistently high inflation” over 2H 2022 - there’s not a great case for it from the logical perspective (if inflation is high, demand should decrease b/c prices are high), and there’s also not a great case from it from the data perspective (commodity prices dropping, inventory building, consumer spending dropping). But yes, that’s a separate post. Back to the point here.

Oh yeah, this is a trading forum - if inventory is building and demand is dropping, retailers need to move inventory because it’s taking physical space and it costs them to maintain old inventory. So, interesting companies to watch here for bulls are resellers of discounted inventory - think TJ Maxx (TJX) or Ross (ROST). People need clothes, prices are high, so they’ll seek cheaper options - meanwhile, inventories are high, so TJX or ROST may be able to secure their clothes at a further discount. I’d also be watching something like Dollar Tree (DLTR) as consumers shift to discount retailers while prices remain high. I’d say these are tickers to watch in the short term (e.g. Q2 earnings forecasting) if they anticipate steady or increasing demand due to inflation and recession concerns.

I’d also watch on the bear side companies which have exposure to inventory risk because they have to manage physical inventory at retail locations, and need to specifically offer a wide variety of products (you don’t go to Ross to shop for specific labels, you go to see what they have). That’d be the Walmarts (WMT), Targets (TGT). I’d actually say Costco (COST)may be insulated from this as I believe some percent of their inventory are actually on consignment and they’d benefit from a shift in retail spending to wholesalers.

But with all of this I wouldn’t gamble into any Q2 earnings, I’d wait and see what the guidance is for these companies (and others). If we’re truly going into a recession, or even slower growth overall, these would likely be positioned to weather the storm better than other companies.

Way too long, didn’t read: supply chain unwinding, commodity prices dropping, building inventories = lowered prices going forward. That would translate both into reduced margins for some companies that have to maintain inventory (WMT, TGT) and then potentially an opportunity for discount retailers that would benefit also from consumer spending habits shifting (TJX, ROST, DLTR). Consumers may also shift spending into wholesalers (COST), which manage inventory but may be insulated due to their consignment model (need to research this further). If we’re in a period of slow growth or a recession in 2H 2022, these trends could hold as consumer demand starts to cool off and they focus on essentials and discounts.

In regards to food, I think many large grocery chains tried to pre-order what they could during the early invasion days for fear of shortages (on top of already existing supply chain issues) but now seeing as how that hasn’t affected the US as much, combined with the jacked up prices, resulted in people purchasing far less than stores anticipated. I think there will still continue to be a little rubber-band effect around food for a while (sometimes too much, sometimes too little). For instance, my two stores haven’t had crunchy peanut butter in a couple weeks!

I’ve noticed some food products have gone down a smidge in price, except for meat. Meat prices are staying up there, some have even ticked up a little over the past couple weeks.

According to the AAA gas prices website, regular peaked on 6/14 @ $5.02 and diesel peaked on 6/19 @ 5.82

Current average for regular is $4.70 (-.32) and diesel is $5.66 (.16). A little relief for the daily driver, but not much for the truckers, farmers, trains, ships, heavy equipment, or other industries reliant on diesel (about 5-cent drop per week since the peak). Likewise jet fuel is basically kerosene which is a similar grade to diesel so I’m guessing those prices are staying up there too.

If we take the 5-cents per week drop on average for diesel, that’s about another 40 cents come September 1st. So maybe around $5.25 average? (I know, that is a total wild ass guess, but all we got at the moment). That is still a very very far cry from ~$3.00 diesel before the war…

One of the biggest problems preventing inflation from coming down is HIGH ENERGY PRICES. Unfortunately they look like they are going to linger around a little longer than people are hoping. I don’t think we will start to see any real relief until near the end of this year, and that is assuming there are no more unforeseen problems.

Everyone thinks about gas prices, and diesel prices, and transportation costs. But here’s another aspect that I feel is worth looking into.

I was reading this Bloomberg article the other day, talking about Century Aluminum closing their biggest of three US sites they own, which makes up 20% of the US supply. This site is the second largest plant in the US, I’m guessing the largest is owned by Alcoa. 600 workers are also getting laid off at this one site.

Not only does it take a month to wind down the plant and properly drain everything, it takes six to nine months to restart! Century Aluminum is planning to idle the plant for as long as a year.

There are also at least two steel mills in the US suspending some operations.

This isn’t isolated to the US, various plants across Europe & Asia are also shutting down. Any energy or natural-gas intensive business is taking a long hard look at how long they can afford to keep running.

So, what does this tell us?

Energy prices aren’t coming down to pre-war levels anytime soon. Some of these plants won’t be back to regular production until 1.5-2 years from now! So figure end of 2023 or early 2024 depending on how the economy is.

By idling plants and reducing supply, prices will continue to stay high (or maybe even go up) in the short term while the economy is still operating at its current level. But until energy costs go down what choice do they have?

They believe demand will decline soon, or at the very least energy costs will outpace their ability to raise prices, otherwise they wouldn’t be closing now.

This is going to cause a rug pull for the Infrastructure Bill, which was requiring US made steel, aluminum, and other materials to be used for roads & bridges and other projects. Likewise this is going to hamper the electrification part of the bill beefing up the US power grid, adding thousands of EV charging stations along highways, and such. So potentially hampering adoption of EVs?

Taking a brief look at various Steel and Aluminum companies, many have started to come down from their recent peaks, but still have plenty of room to fall. I Believe Steel Dynamics is one of the first companies to report earnings in that sector in the coming weeks.

Hiring, firing and quitting…labor makes the world go round.

Mays numbers below indicate smaller businesses are having more separations than the larger employers (500-5000 employees) which means people are holding onto their full time jobs more, and not leaving for more opportunities which would have been seen in late 2021. Covid relief to the employee and employer made big splashes which we are paying for now, and businesses previously hindered by Covid restrictions are open full tilt. More jobs being created as the admin is trying to take credit for, but who is filling them now? How about the layoffs

This has been in the back of my head since I read it earlier today. I wonder if we will start to see some of the high-dollar restaurant stocks fall like Chipotle, Starbucks, Darden, Texas Roadhouse (wow that stock has violent swings), Dominos, Papa Johns, Cracker Barrel, Wing Stop, etc, etc…

Inflation has to be hurting restaurants hard on so many levels. They are high volume / low margin businesses…

this is anecdotal and only relevant to your portion on retailers. I’ve heard from multiple people near me that places like target are telling people to just keep their returns and refunding them because they have too much inventory. Anecdotal. Only know of one person that has happened to. Still, that seems kind of wild. This was not in a big city so i’m curious if anyone has heard the same in a major area. Demand destruction is definitely starting to happen here. The US is a big place though so not to say thats the norm as right above refrigerate says everything still seems good in Phoenix area. For reference i’m Ohio.

Consider that shrinkage in 2021 was over 50billion and given the new bail reform laws barely any retailers are prosecuting. Retailers in large shopping malls also had to and continue to endure the labor market impact which caused many to close early and reduce their operating times. This however also saved them on this costs if revenue wasn’t being generated. Just some considerations on retail

This is very anecdotal, but met a dude who is with corporate at one of these large grocery chains, and he made to points:

Till now they had been able to pass on costs to consumers, but they’re seeing demand going down now, so have decided to eat more of the costs, reducing bottom line.

They have no plans of letting anyone go at the moment because it has been really hard to find people, and they are still looking for people. Things would have to change drastically for them to consider job cuts.

Sample size of one, but sounds like something that would make sense for many companies - margin compression but no layoffs yet.

This is entirely accurate from what I have witnessed at our corporation. Hourly wage workers are still hard to come by. And no signs of relief.

The wage demand is getting out of control especially for smallish corporations. When fast food and retail is paying big bucks per an hour to bag groceries or throw some food in a bag. To me it’s a sign of worker shortage and employment continuing to rise. Evidence in jobs numbers recently released.

Personally don’t think this is a bad thing for the moment. But need a slight decline in inflation and that coupled with strong employment numbers could actually become bullish and show signs of the soft landing we have been so promised.

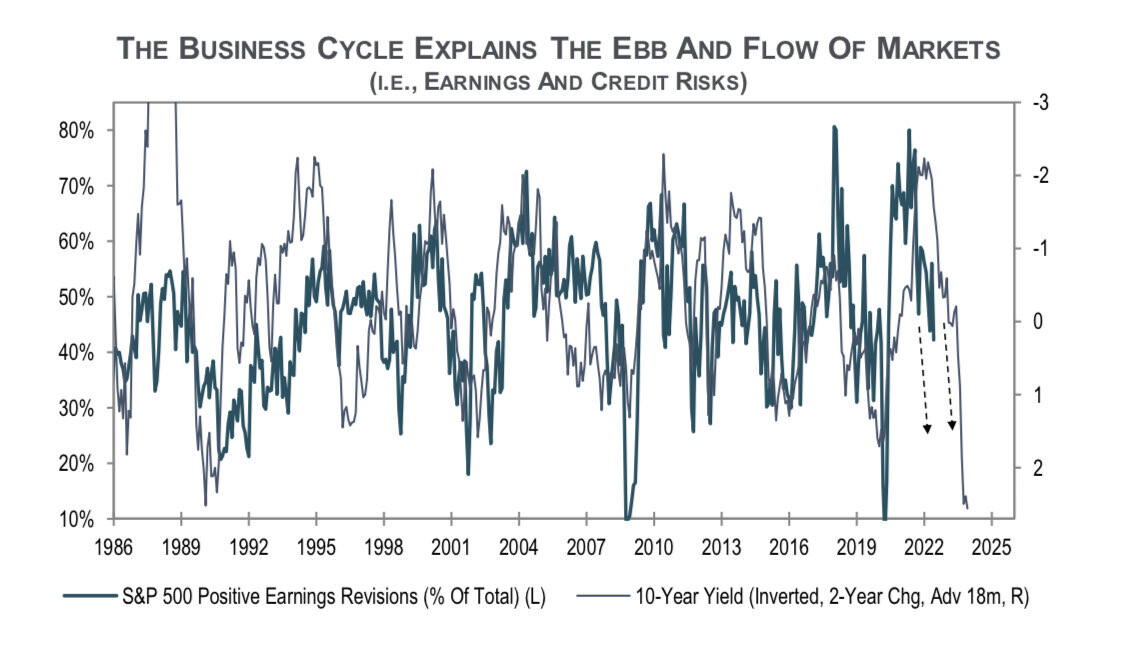

Such swings are a little absurd, and are more indicative of the fact that whatever model they are using is not able to incorporate the string of fairly contradictory data inputs its getting - strong employment and persistent inflation, yet all kinds of other slowdowns.

Bond markets priced a recession with a -2% GDP last week; if they are not suffering from the “boy who cried wolf” syndrome already, they will now price a weaker recession and rates may go up again. To the detriment of the market.

One aspect I would include is the rising rate of crime in major cities -

Does the higher rate of crime discourage - people from enjoying restaurants and other leisure activities, while I am sure inflation and higher crime are correlated - is the fear mixed with inflation also a factor to consider for those on the spectrum of who can absorb it.

If earnings revise lowered guidance (likely) going into 2H 2022 then I think the market will adjust accordingly. However, I do think that there are several possible catalysts then which will spark rallies or inverse the bear market in the future -

SPX reaches a forward P/E multiple after revised guidance from Q2 earnings that is “too cheap” to ignore - I think this is probably around 14x, currently we’re at 15x but no revised guidance just yet - when this happens hard to say, but you can calculate it, would be a good level to watch for a rebound

Inflation starts to cool off - this will take months to manifest in a way that impacts Fed decisions but a key time will be the September FOMC - if they have at that point 3 consecutive months (June, July, August) of cooling CPI then they may go from 50bp to 25bp

Q3 earnings - if companies are able to weather the “storm” of a strong USD, cooling demand, but also cooling prices and cooling wage increases, they’ll likely beat their targets in Q3 (reporting in Q4), which could lead to another rebound

Basically, everyone is looking for the worst right now. We may get confirmation - if Q2 earnings are largely a miss, I think the market could go pretty far down from here - and a recession isn’t yet priced in for the market. BUT, if companies and the markets are moving in anticipation of slowed growth - meaning revised guidance now, Q2 earnings largely beat, and inflation starts to cool off - I think that there’s certainly a real bottom in the 2H of 2022 of which we may see a good, sustained bounce. Forward PE - who knows, September FOMC, Q4 earnings (starting in October).

GL everyone, CPI out tomorrow. If inflation still running higher than expectations, could be a bad time. I’ve got a strangle on SPY I’m holding overnight.