“U.S. supplier price increases decelerated in December to their slowest annual pace since March 2021, adding to signs of cooling inflation.” @WSJ

“Retail sales, a measure of purchases at stores, restaurants and online, declined a seasonally adjusted 1.1% in December from the prior month, the Commerce Department said Wednesday.” @WSJ

“They could begin deliberating at the Jan. 31-Feb. 1 gathering how much more softening in labor demand, spending and inflation they would need to see before pausing rate rises this spring.” @WSJ

The data that will substantially influence the outcome of the FOMC decision has been published. The only new reports that might have an impact are the regional Fed surveys of manufacturing and services for January. Already reported was the New York survey for manufacturing (Empire State) which showed an outsized drop while service sector data remain in contraction. Then the Philadelphia Fed survey for manufacturing told a more positive story, although its factory sector is slowing. In the coming week, the Philadelphia Fed will release its survey of the service sector at 8:30 EST on Tuesday. The Richmond Fed’s surveys of manufacturing and services will be reported at 10:00 EST on Tuesday. The Kansas City Fed’s manufacturing survey will be at 11:00 EST on Thursday and service sector survey at 11:00 EST on Friday. If these back up the data that the factory sector is moving into recession and that activity in services is continuing to slow, it might give Fed policymakers another reason to reduce the size of the next rate hike to 25 basis points after the 50 basis points in December. The FOMC will have evidence that inflation is improving – if still too high – and incorporate lagged effects of previous rate hikes into their policy outlook.

The report that is most anticipated is the advance estimate of fourth quarter GDP at 8:30 EST on Thursday. The Atlanta Fed’s GDPNow looks for an increase of 3.5 percent in the final quarter of 2022, similar to the 3.2 percent rise in the third quarter. While this makes the second half of 2022 one of solid growth, indications are that first-quarter 2023 is going to reflect subpar activity, at best.

LEIs say we should remain open to economic data weakening considerably in coming weeks/months. TBD. SPY puts and VIX calls are stacking up in March, someone knows something.

“In our commercial business we expect business trends that we saw at the end of December to continue into Q3.”[color=orange] - $MSFT earnings call[/color]

Comment aligns more closely with earnings-recession narrative versus soft-landing narrative.

Thank you so much @rollover for keeping up with all the economic data. I agree a pause in rates is coming soon but probably not this go around. The tone from the fed speeches gives me hesitation on picking a direction to lean towards before the speech. I will take a small position equal in puts and calls if I play at all but will likely just see what happens from the side lines and maybe try to scalp a little. I have been looking a lot at what happens in the market the week after rate day and hope to finish that data collection and organization later tonight. So far the strongest correlation to market direction the following week is with a Red rate release day of more than .4% drop from open to close. The following 7 days tend be pretty red also. I’ll hopefully get that posted in the FOMC Rate day (not mins) thread tonight

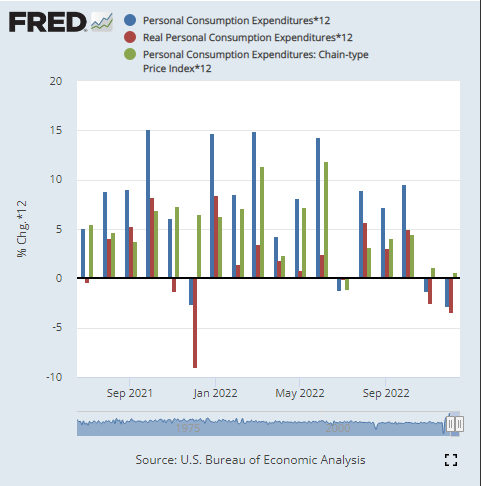

PCE shows HHs are feeling the pinch (not enough to change the quarter point for this week) but if the data continues to this trend, it will bend the Fed’s curve.

Market is pricing in a 0% probability the Fed hikes by 50 basis points tomorrow. This is what could set up the ‘blood in the streets’ scenario if they do hike beyond a quarter point.

Do you think that is a possibility? That would most certainly cause $rope. Im starting to feel more bullish on tomorrow due to employment cost and consumer confidence release today.

I think they will thread the needle, quarter point raise with very hawkish language. This current market counter-rally is not what Jpow wants to see so there is always the very real possibility of hawkish action.

Market is pricing in more than one rate cut in the 2nd half of 2023, which is completely against fed guidance.

With financial conditions looser than pre-rate hikes, JPow will need to tread carefully and avoid sounding too dovish. I think it’ll be a 25 bps hike with hawkish language such as:

Implication of higher terminal rate, e.g. “we will continue hiking by 25 bps every meeting until the job is done”

Doubling down, or tripling/quadrupling down at this point, on holding higher for longer, e.g. “we are not even thinking about thinking about rate cuts in 2023”. Perhaps even straight up stating that “the bond market is incorrect in their assessments about rate cuts.”

Could argue that all of this has been said before, and therefore “priced in”, but the actual thing is literally not priced in, e.g. no rate cuts in 2023. If JPow can navigate the conference such that the markets actually believes him when he guides higher for longer, then the market would then start pricing in these words.

But what will it take for the markets to believe the fed? Not entirely sure because yeah, these things have been said before. Maybe JPow could turn it up a notch.

Now we are going to take the Fed guidance as the holy grail after chastising them over the transitory etc so essentially spin it to our narrative.

JPow job isn’t to universally crush the economy with over tightening. As the numbers have continued to trend down without any adjustment in rates for 60 days I’d take that as a sign that the levels we are at are working an very select hikes are ahead. If any more after tomorrow.

As Ni mentioned if the numbers become hot again sure they won’t stop but id think it would take a sudden large surge not just some blip uptick to cause more sustained hikes. We also forget so easily that prior to last half of last year 50 bps and 75 bps jumbo hikes are not the new normal they are a unique counter reaction to unique times.

That’s what I was getting at we are so quick to jump on a wagon and accept it. Now granted the Fed was behind the curve and had to amplify to catch but I’d be absolutely shocked to see a 50 bps anytime soon unless we get severely out of hand again.