https://twitter.com/TheSpacShack/status/1479119786999107588

Haven’t looked into this yet but it seems like a sizeable chunk of shares will unlock on 19 Jan. Adding this as a placeholder for now for what could be worth some digging into

https://twitter.com/TheSpacShack/status/1479119786999107588

Haven’t looked into this yet but it seems like a sizeable chunk of shares will unlock on 19 Jan. Adding this as a placeholder for now for what could be worth some digging into

They had a PIPE shares unlock on Sept 1st 2021, it seems the price dropped 20% and recovered to -9% right after. FYI

Taken straight from the merger release:

“None of Lucid’s existing investors will sell stock in the transaction and are subject to a six-month lock up for the shares they receive in the transaction. All proceeds will be used as growth capital for the company to execute on its strategic and operational initiatives. Lucid currently has no indebtedness.”

“The transaction includes a $2.5 billion fully committed, common stock PIPE with a unique investor lock-up provision that runs until the later of (i) September 1, 2021, and (ii) the date the PIPE shares are registered.”

“In connection with the transaction, Churchill’s sponsor has entered into an agreement to amend the terms of its founder equity to align with the long-term value creation and performance of Lucid. Churchill’s sponsor has agreed not to transfer its founder equity for 18 months after the closing of the transaction.”

So I took a quick look at it and while it’s true that Ayar (a holding entity of the Saudi Arabia sovereign wealth fund) is party to the lockup expiring on 19 Jan, it’s not clear what portion of the remaining legacy Lucid shareholders are similarly locked-up. The Investor Rights Agreement is not clear on which other individuals or entities are bound by this. Senior execs / directors which I would assume would have signed on to the lockup only make up c.1% of the shares.

My view is that it is probably a strategic LT bet on the EV space for the Saudis so it is probably unlikely they will sell down their stake at this stage even if their lockup expires. As for the remaining legacy shareholders, between 1 to 11% of the shares could potentially be unlocked, depending on your view / reading of the docs.

TLDR, I think there might be a small downtick post unlock but unless the insider unlock is much larger than 1%, it might not move down too much.

https://www.sec.gov/Archives/edgar/data/0001811210/000110465921026357/tm217491d2_ex10-1.htm

Currently in with puts for Jan 28, 36p

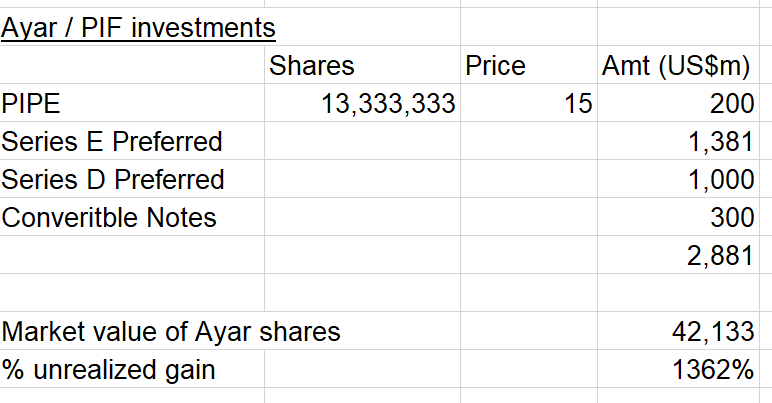

I did a bit more digging and Ayar’s cost basis on their investment is only around 2.9bn but the market value of their stake today is 42bn (at $41.5), a whooping unrealized gain of 1362%. So it is entirely possible that they look to take some off the table and realize some of their gains.

They were also a previous investor in TSLA and exited pretty early so an early exit for LCID is a possible scenario but bear in mind a big move will only happen if they announce they are selling down

Decided to take a small position here as well given how much PIF is up and current sentiment towards growth names. Think it might be worth a punt

Sold some 18 Feb, 40-45c credit spreads and bought / looking to buy some 11 Feb / 18 Feb 35p

I think there’s some confusion here. It’s not actually the PIPE unlocking but it’s the Saudi investors that were able to buy LCID shares at $10. They own the vast majority of the shares which were to unlock 180 days post merger.

180 days drops on the 19th.

Whether you want to look at this as a buying opportunity or opportunity for puts (or both), LCID will now have massive selling pressure. They’re up billions of dollars they are definitely going to cash out at least some of their position.

Also, in case you think you’re reading it wrong. It IS 1.19 BILLION shares. PIPE was 166 million and PIPE unlock dropped LCID ~30%. PIPE bought in at $15. LCID shareholders hold at $10. LCID shareholders will most likely sell bigly.

No confusion here. It’s a question of if and when PIF / Ayar will sell down their stake post lock-up expiry. If they don’t sell the stock won’t move…

Although I agree it is likely they will pare down at least a portion of their stake at some point in time given how much they’re up. Just bear in mind this doesn’t have to happen on 19 Jan or in Feb/Mar at all so that’s a risk you’re taking if you buy near dated puts

Question: shares unlock on the 19th but they may not all sell right away, correct? Would the Feb options be a safer bet?

With the craze around EVs I think this could be a risky play. We have to understand the other side aren’t exactly dumb investors and they won’t be dumping their shares cratering the price.

A constant sell off creating a ceiling is what I would expect, so I think CDS are a better play than puts. Still, being EV the play is risky, but should net nice premiums

On September 1st at the PIPE unlock, LCID dumped from $20 to $15. I think it makes reasonable sense to at least trim a partial position if you’re an early investor in LCID at $10 per share, especially at these prices, and in these times of market headwinds.

Yup I think if you’re buying puts, the further out the ‘safer’. the 18 Febs have the most volume and OI if I recall correctly

Follow-up to my above question though:

Assuming the stock goes flat until the 19th, buying puts NOW for the 21st would likely result in theta decaying your entry. So whether you’re playing the Jan or Feb calls, it would maybe be a good idea to wait, right?

I’m thinking what I’m going to do is look at maybe buying some Feb puts a day or two before the shares unlock on the 19th.

However I’m also looking at the run from yesterday and thinking there’s a good chance of a pullback Monday, then hopefully (for me) flat until the 19th. So maybe a potential short term play is a put near open on Monday hoping for a dump, take profits, then do what I said above and pick up more puts on the 17th/18th

You are correct that if the stock remains flat, theta will most likely decay your options. However, the market is hard to predict and options pricing is even more complex than just shares.

I’m not an expert in option pricing, however we can assume that the share unlock date volatility is already priced in via higher IV, similar to how options have a higher IV before earnings even if the price remains flat. The stock can become more volatile up through the share unlock, increasing IV and thus increasing the option cost, so waiting until right before share unlock isn’t without its risks.

We also don’t know what will happen between now and the share unlock date. Remember this is public info and there are many other players in the market. People holding their shares may begin to dump them before the share unlock if they believe OP’s similar thesis, so buying puts now may even be a better play. There is no indication the stock will trade flat, if we knew that, selling options would be a no brainer and guaranteed profit, but we know that doesn’t exist.

Although sovereign wealth funds operate in mysterious ways, it would not be unreasonable to expect them to liquidate some of their 13x returns at some point in the near future. Market will probably try to front run that, which means we could expect some selling pressure when lockup expires. Will be looking at getting some Puts shortly.

I thought I’d bring a few points here that present a bull case, because its very bearish up in here. I think there is some evidence that points to the Saudi PIF not selling any of their position in LCID when the lock-up period expires on the 19th.

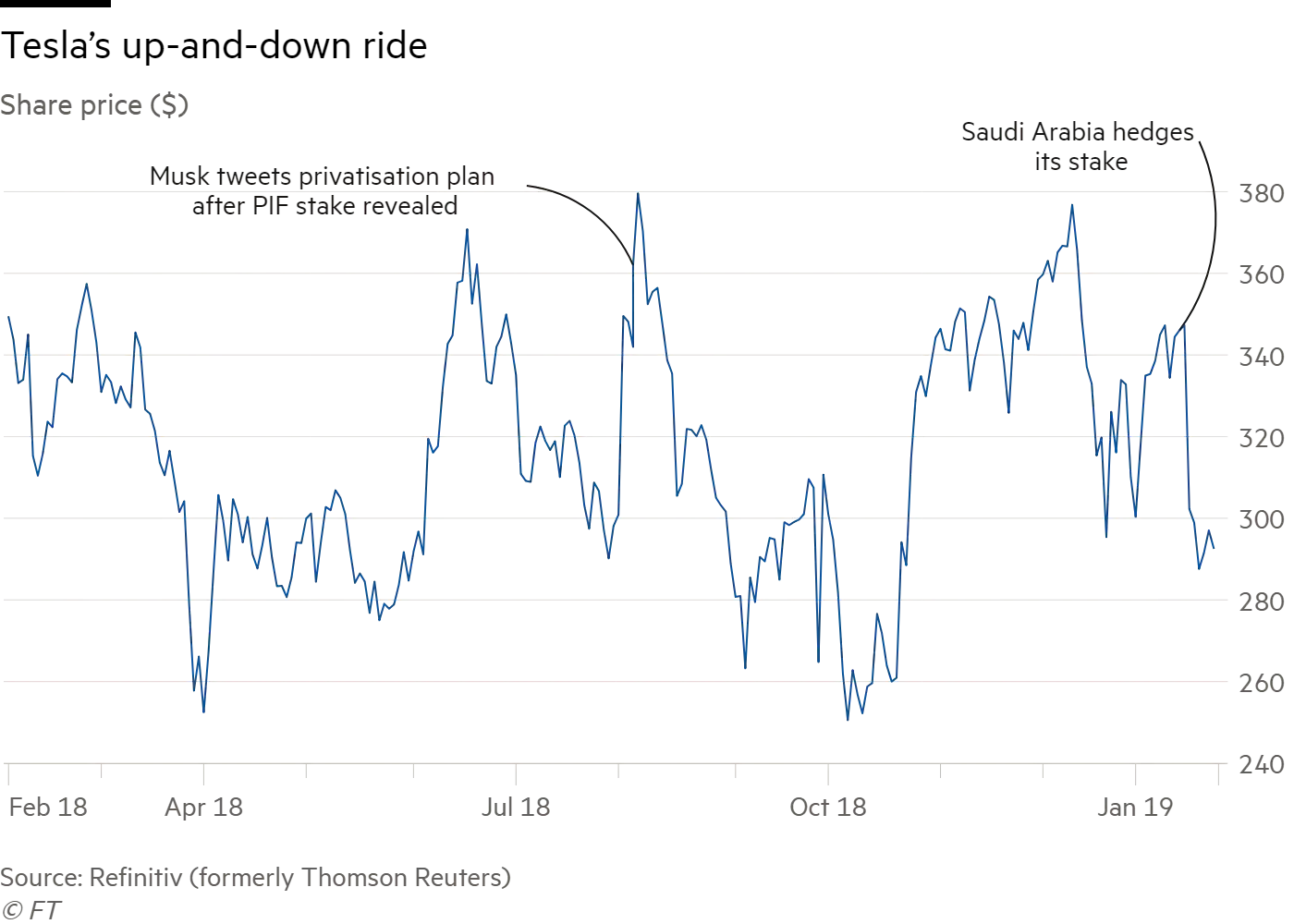

“While PIF’s bet on Lucid has paid off handsomely, it left a fortune on the table by selling the automaker’s biggest rival. The sovereign wealth fund bought a split-adjusted 41 million shares of Elon Musk’s Tesla in the fourth quarter of 2018, but disposed of the entire holding by the end of March last year — when the company’s valuation was about a tenth of its current level.”

Source - Saudi Arabia's PIF Made Fortune on Lucid Motors, but Sold Tesla Stock - Markets Insider

Sources - How Is Lucid Group’s (LCID) Upcoming Lock-up Period Expiration Likely To Play Out

https://twitter.com/SapracOrg/status/1480237589168680961?s=20

https://www.wsj.com/articles/lucid-long-before-spac-promised-to-build-saudi-auto-plant-11615340681

I’m glad you posted this. I intended to write a bull case myself yesterday, and you’ve included part of it. I was chatting with someone the other day after seeing the response to the news late last week about Lucid planning expansion into Europe this year.

I asked them about what they thought about the lockup expiry and their commentary was that the Saudis won’t sell until the factory is built. When I asked about other sellers the response was that Michael Klein can’t sell anything until 2023, Churchill owns 20% and the Saudi’s 60%.

I did some digging into the options chain after opening a short term call trade for this week, and noticing mostly what looked like synthetic longs. I was filtered for large (750+) orders - including those below.

I checked again today and there were more of these large orders. If you are going to go bearish, I think it makes more sense to wait and sell a call spread rather than just buying puts. Or at least give yourself some time.

I’m glad I’m not the only one. I mainly just wanted to provide folks with a different perspective in this thread. I’m bullish long term on LCID, and I still have a load of shares I’ll be holding, but I cut all my calls last Friday. I picked up a few ATM 1/21 puts today, just because I think there will be a correction this week. I’ll sell those puts long before the 19th, though. Its a game of “wait and see” for me, although I certainly lean toward the mindset that PIF will not sell.

Fully appreciate the above comments. As I mentioned a couple times, there is no guarantee PIF will cut their stake and that even if they do, that this will take place immediately after lockup expiry. So playing on the short-term downtick in price is a bit of a gamble - I only have a small speculative position in this and I wouldn’t encourage anyone betting the farm.

That having been said, it is also important to note the following:

PIF’s investment in LCID is up a massive amount and at these multiples of return, it is not inconceivable that they opt to cover their cost basis by selling $1-2bn worth of LCID shares

For TSLA, PIF bought shares in Apr/May 2018 when it dipped below $300 and hedged their stake just a couple of months later in Jan 2019 when the stock closed just below $350 (that’s roughly a 16% gain). FT reports they put a collar in place, meaning they sold calls and bought puts here to lock in their gains. It is possible they look to implement a similar arrangement here for a portion of their position, particularly if they’re concerned about downside risk from macro factors in the short to medium term

(behind paywall, view incognito)