Starting a thread here, courtesy of a heads up from our Shit Poster in Chief @Iloveyou

With recent news retailers have too much inventory on hand, there’s an opportunity to make a bet on the logistics side. Specifically, the trucking industry. Initial thesis is these companies will be taking hits as there’s less demand for the services. If there’s a bullish point then feel free to add here so we can have a wholistic view. Will update as we flesh out dd on TF.

We’re primarily targeting $JBHT because they are primarily an asset-based motor carrier. This term refers to motor carriers that own physical power units to haul freight with, whereas someone like a C.H. Robinson would be thought of as a non-asset based carrier because a large part of their business is sourcing motor carriers to haul freight. They have the most activity of the other publicly traded asset-based motor carriers.

The issue is $JBHT is a hard read. 46% of their revenue in Q1 2022 was intermodal - in the context of J.B. Hunt this is primarily stuff that’s being shipped via a rail line where J.B. Hunt is responsible for managing the logistics from A->B, taking the stuff to the rail, making the final delivery, etc. Therefore, in order to understand how they’re faring, we need to know how trucking and how rail operators are faring.

In reviewing their Q1 Earnings presentation, they place significant blame on the capacity and performance of rail lines.

Volumes early in the quarter were negatively impacted by network fluidity

issues attributable to labor challenges within the activities of our rail providers and customers, as well as our internal operations largely as a

result of COVID-related disruptions. As the quarter progressed, volume

levels strengthened as customer unloading activity improved, although rail network velocity continued to govern our ability to capitalize on even greater intermodal demand.

This is where we are for now. Their Q1 earnings are very bullish, but we need to understand how a reduction in demand for their services and increased diesel costs will hurt them.

Here’s a fascinating article on demand and how retailers leveraging the naturally long transit times for rail shipments as “free storage” basically. It is from April, but it provides several leads on economic indicators we can use to understand how J.B. Hunt or another company is doing. Intermodal remains resilient, despite trucking demand dip - FreightWaves

Seems to me based on financials shared in TF they are in fairly good shape with assets and largely outweighing their liabilities.

One thought that came to mind as far as diesel prices and less loads. Is essentially freight companies can control their own destiny when it comes to this as if they are hauling less they don’t need to consume as much diesel. Also they set their own pricing per load. As fuel cost increase shipping costs have increased dramatically as well basically off setting the rise. From what I see JB Hunt seems to have contractual accounts IE companies that they exclusivity with. However In current situation this could be to bearish side. If contracts were pre negotiated more than likely their load rates were as well so even if the demand for transport doesn’t stagnate pricing a load at 2 dollars a gallon vastly differs to 5-6.

Really would be interested to see how many dedicAted contracts they have.

Did come across they seemed to have closed an acquisition in Q1 as well.

Seems this deal was funded in cash. Which is probably to the bullish side. But “less than a truckload “ furniture transportation would be hardly cost affective with rapidly rising fuel cost.

I’m hardly an expert, but this doesn’t look horrible. Yeah, cash is down. But AR is up (assuming they don’t get stiffed), they’re growing through equipment purchases. Not taking on additional either

Higher Inventory = Less Demand = Shippers more incentivized to use cheaper alternatives (intermodal as opposed to truckload) = more revenue and demand of this type of service = desynchronization from trucking demand (article mentioned above) = strong balance sheet numbers under good management.

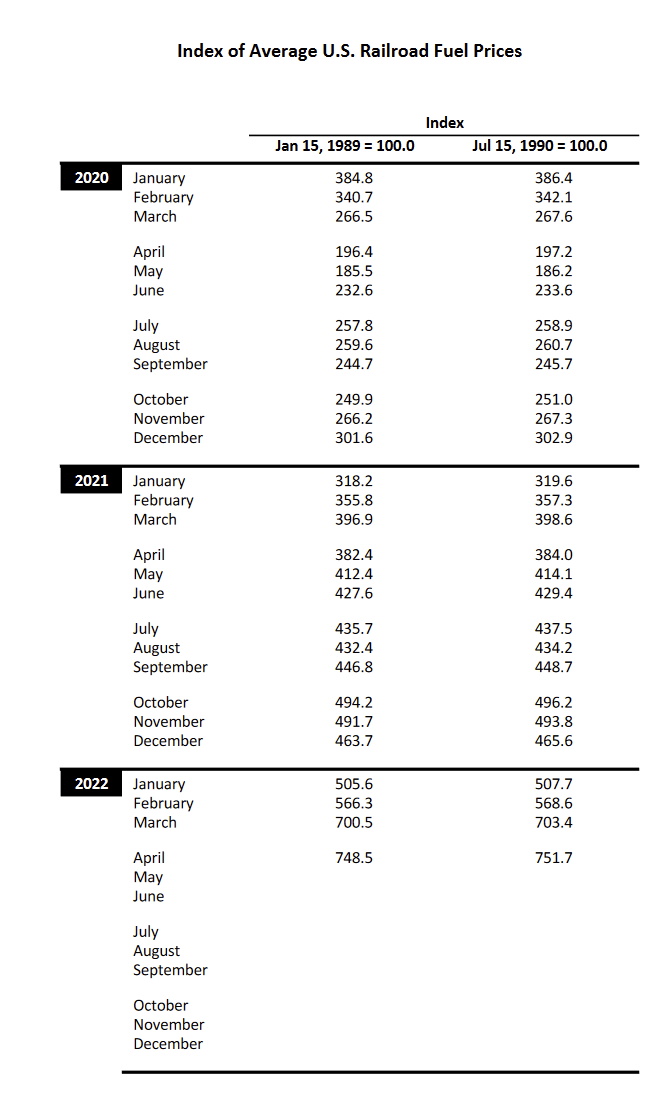

Here’s a quick figure on how fuel costs are affecting rail lines. They are going to pass these to customers of course, which means intermodal may have been far, far less of an attractive option come March. Anyone work in logistics that could comment or confirm that?

I like looking at QoQ cash flow trends as that is the lifeblood for any business. Yes they could have access to large LOC, but if we anticipate demand slowing down, not ideal.

Even with revenue up comfortably, their cash position is the weakest in at least a a year.

After reading numerous articles and info about JBHT and learning some freight lingo. I believe I am bullish on JBHT. Seem to be very diverse across all modes of shipping company has been in business since 1983.

Actively wanting to spend money to add to capacity. And they have been through rising fuel costs before when diesel was near these levels in 08. Found this to be one of the more interesting reads.

I think knowing who their top customers are would be helpful.

Also, @Iloveyou you are def right about intermodal. Looks to be the cash cow at the moment (JBI)

I read the entire transcript for their Q1 earnings call. Analysts asked several questions about fuel concerns, China shortages, labor issues and each time J.B. Hunt stated that they continue to see crazy demand for intermodal capacity and even if there were to be a downturn, they’re already turning down thousands of jobs per month because they can’t get enough labor to handle it. In other words, “recession or not, we’re maxed out”. Normally stating you were maxed out would be a huge problem but it’s a market-wide problem.

There are certainly bear cases for J.B. Hunt, but aside from a reduction in cash, I feel they are sector-wide.

Here’s a list of important points I noted from their Q1 transcript. It’s attached as a PDF because I made notes in OneNote and they don’t copy over to Discourse well. I’ll fix later.

I was leaning bullish on J.B. Hunt, but Ni found some amazing sources. Certainly a lot of factors at play here! Thanks @The_Ni I’ll go check out his Twitter.

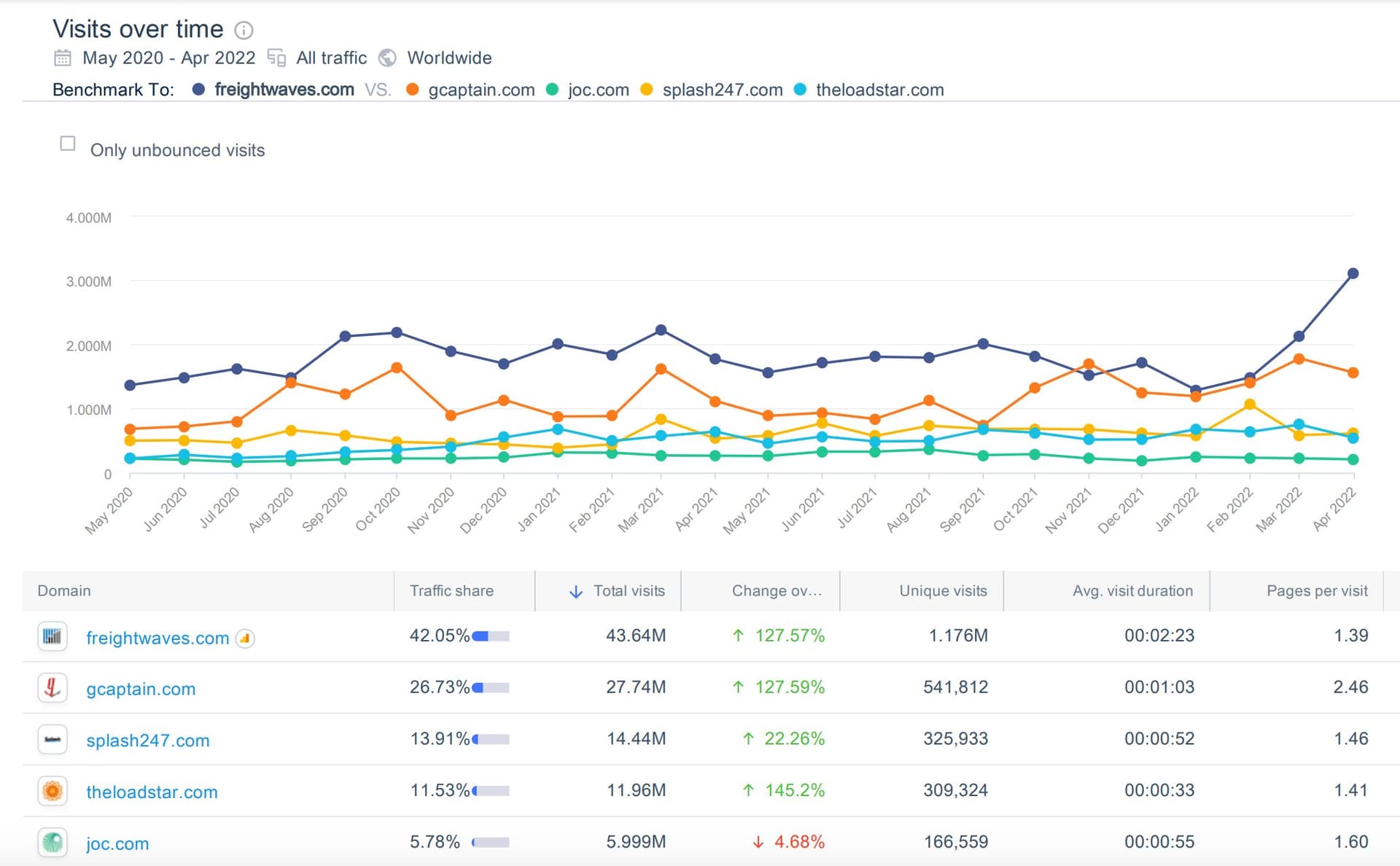

I actually do know FreightWaves, as I’ve provided information for articles they’ve written before and my organization has had some brief discussions with theirs about data and their SONAR platform. Very smart company, came out of no where and over the course of a few years it went from a Facebook group->blog site->legit news outlet->an entire forecasting platform.

Indeed, apparently they made hay when they realized so many people really got into logistics when supply chains went bonkers after being hella boring for years and years. Including hedge funds which are now paying big money for this. FW did better than others to capture this interest.

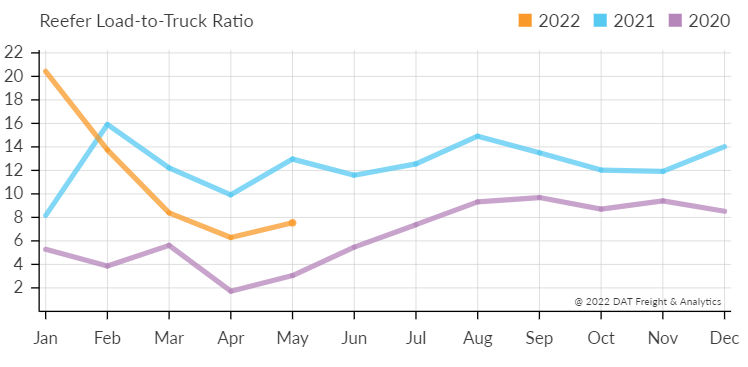

One set of numbers to look at is load-to-truck ratios - the higher the ratio, the fewer the trucks available, and so higher the rates and more at capacity supply chains are. This ratio has been falling recently.