I’ve observed the effects of such weakness in my day-to-day job.

One of my pressing issues is a carrier network (read: one guy that paid LegalZoom 3x for 3x business incorporations for the same set of assets) that failed and probably has about 10-20 truckload shipments held in a warehouse they won’t release. There will be more of these stories of small carrier operations failing, for sure.

Another pressing issue the growth of consolidation schemes, most of the ones that reach my desk involve some jerkwad that agreed to have a shipment delivered by t+3 but instead took the shipment to a warehouse, unloaded it, reloaded into a container (possibly with another shipment) and sent it via rail. The purpose of this is along the lines of:

3000 for a linehaul rate

2800 in fuel + other expenses

or

2500 to rail it and deliver

Many small, unreputable carriers are choosing the latter. In order to avoid punishment, they insist the delays are due to truck breakdowns, etc. when in reality the shipment was sent via rail against the contract terms. Depending on the type of shipment this can range from mildly inconvenient to catastrophic. For example, any kind of food, pharmaceuticals, personal care goods, drinks should not enter circulation if integrity of the shipment is compromised.

The main point though is that these small carriers are forced into these practices because of a sharp increase in fuel prices. Spot rates aren’t responding equally to fuel costs due to shrinking demand for freight transportation.

The question we most need to answer is how does this effect a massive, established freight carrier like J.B. Hunt.

So I did some additional research tonight and found this source:

It’s a short article and it’s an interesting read, frankly, but here’s the juicy bit:

" The capacity situation, however, has been bifurcated by carrier size. Small carriers dependent on load boards for freight have seen fundamentals tank as lower spot rates have been met by rising costs, notably fuel. Conversely, large fleets are still seeing contractual rate increases and many management teams say they could use additional drivers and equipment."

If that’s true, I believe J.B. Hunt is one of the best-positioned truckload freight carriers. I believe the ticker will be dragged by market conditions like almost all others, but they have strong potential for growth otherwise.

most contracts have what is called a fuel sur charge. So as fuel rises, so does the fuel surcharge. it may be calculated a little different in each contract, but I have never done a contract with a customer that was an “all in price”. it protects both the trucking company from rising fuel costs, and the shipper from being gouged when fuel prices drop.

Another tweet from the FW CEO that is full of information that basically confirms the trend we discussed two weeks ago - enough weakening to hurt the new outfits that spring up last year, but not enough to hit the big boys: https://twitter.com/FreightAlley/status/1540863514641842177

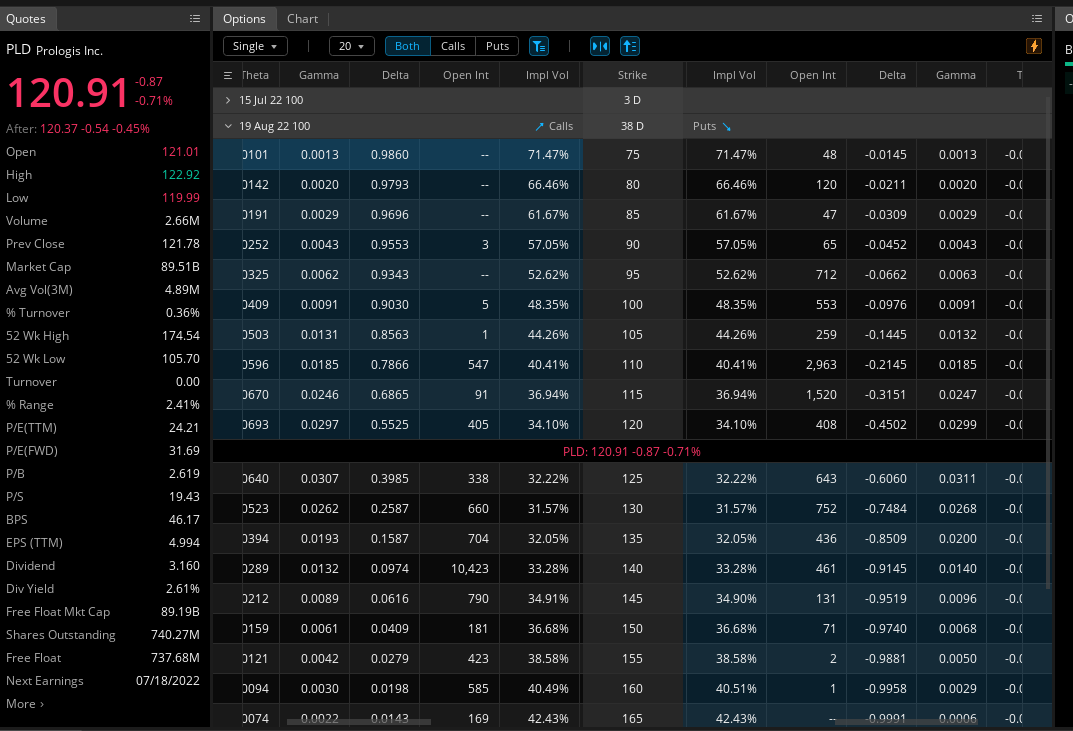

Monday PM - Prologis (3rd party warehouser) (PLD)

Tuesday AH - J.B. Hunt / Marten Transport (JBHT) (MRTN)

Weds AH - CSX, Landstar, and Knight/Swift (CSX, LSTR, KNX)

Prologis is a different business than a trucking company, but excited to hear their guidance to gauge what the trucking earnings may say.

Originally, I was going to plan to ride IV on the tickers with the most volume, but while trying to figure that out I noticed the OI on the 8/15 monthlies for PLD seems wildly stacked and IV seems low. Any earnings gurus have thoughts on upside in trying to ride IV on PLD?

im down to ride IV with you brother. Probably play the downside as it seems trucking took an overall hit with rising fuel prices. were you thinking calls?

Oddly enough thought of this thread in drive to work today. What’s the thoughts on SNDR they haul a lot of WMT loads. And if retail inventories have been elevatedas we have heard with previous retail earnings guidance this could result in less loads or routes needed I’d think.

I can tell you WMT squeezes everyone, so if they are shipping less SNDR definitely got squeezed by them in the process. I will stay away from them though, because it seems very low volume, spreads are insane, and there’s almost no open OI.

If you do want to play a traditional over the road trucking co, I’d look at KNX as the volume is significantly higher and their business model would be very similar.

I think it depends. I’m most interested in PLD, KNX, and CSX as they have the most volume.

PLD - I’d like to lean on someone with more experience in industrial real estate investment as their business is to lease warehouses to other companies.

CSX is a tough call, as the rail lines really benefited from the supply chain crunch / shortage of available trucks.

KNX - Leaning bearish due to fuel + probably a decline in brokerage revenue. Knight is the brokerage part of Knight-Swift, I’m not sure how much of their business is hauling and how much is brokerage right now.

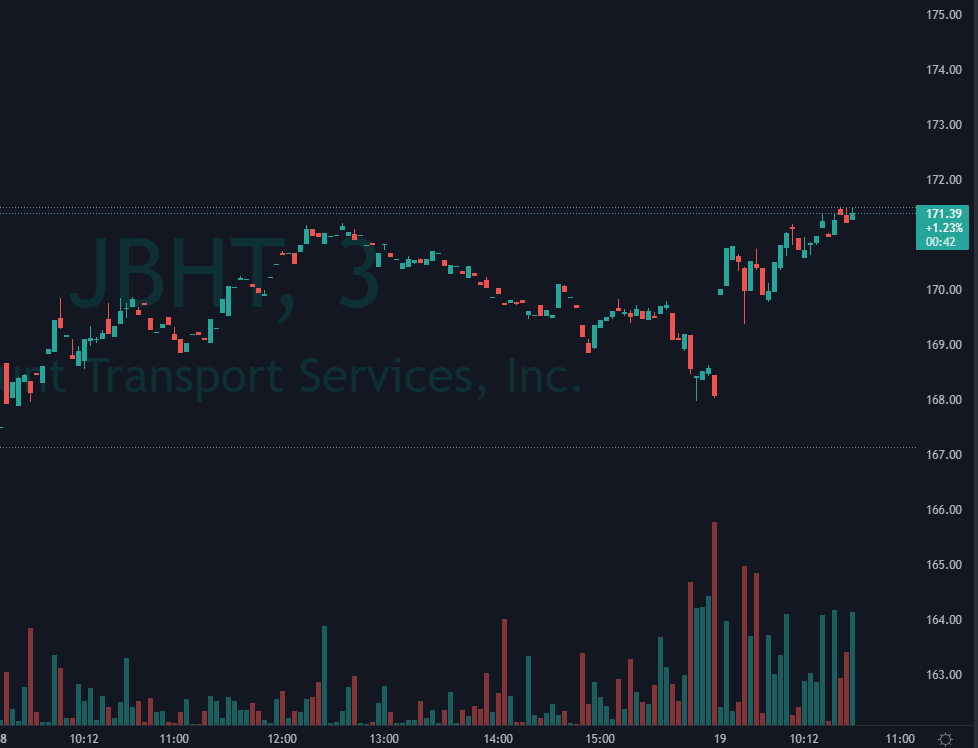

From a little (very tiny) bull perspective on JB Hunt

And related BNSF news on collaboration on rail loads which was raised I believe during their last ER. Be interesting to see how much of that partnership has saved them money or increased revenue

Marten came out with their earnings and beat estimates - $0.39 EPS vs 0.33 consensus.

Their earnings were very strong - but it seems their dedicated growth slowed compared to intermodal (read: choochoo trains and boats) and brokerage (skimming 20% off the top to have some other fuck do the work for you). Marten is not a company I thought of as having a large brokerage business so I think some of this was they had a lot of room to grow their brokerage, whereas KNX, LSTR, and JBHT have established brokerage operations. MRTN’s Q1 brokerage revenue was about 30m, JB Hunt’s was 675m.

Based on this though, I’m expecting good earnings for JBHT, LSTR, KNX, and CSX. I’m holding 7/22 29.5c for CSX, but do not anticipate holding into earnings on Weds AH.

when asked how customer sentiment / slowdown in demand is affecting them, they largely said the market is so massive there hasn’t been an effect on them. they did comment seeing a strong decline in last mile deliveries of value furniture products (think low-end like Ashley, IKEA, Rent-a-Center). This makes sense because if you’re low income gas is likely killing you.

fuel is largely a pass-thru cost for them

fuel is hurting small carriers more - as they described they are fleeing to the safety of large fleets. 2020+ was great for small carriers or owner/operators (dude and a truck) due to an abundance of freight, hours of service regulation suspensions, and high spot rates. Spot rates that aren’t keeping up with inflation, diesel costs, and a reduction in demand are crushing small carriers that rely on spot loads (most of them). This can be interpreted as bullish for large fleets. People are no longer working for themselves so they can enjoy the safety of working for a mega-carrier like JB Hunt that can weather a recession. This means large carriers like JBHT, KNX, and LSTR have more drivers, more capacity, and a better ability to handle customer demands.

As MRTN ran 17% yesterday, look out for JBHT and other motor carrier stocks today. I don’t think we’ll see such great movement, but there could be some nice plays out there if the market trend agrees.

Nothing notable with JBHT today. Trimming half of my CSX position at 42% profit. Spreads are a little wide here, so it can take a minute to get a fill at the ask.

From what I can tell, strike is about half the unionized railroad works. If rail freight demand is inelastic, this could result in major price dislocations.

Possible plays:

Bullish on JBHT and KNX (trucking companies, though intermodal might complicate things)

Bearish on CSX and UNP (rail companies)

Bullish DBA, DBB, and DBC (commodity ETFs)

Possibly bullish on ZIM, DAC, GSL, if this lasts (shipping)

Moves tomorrow should guide us on which of these end up being real plays.