Curious how you are handling your boomer accounts in light of the extraordinary expectations for market decline. How big of a bet are you making (% based not total dollars) for a downturn related to your total net worth?

If we believe we will experience something worse than 2008 and 2000, it may be prudent to hedge in other accounts in addition to our day trading accounts depending on how confident we are in the extreme downturn.

I hedged my boomer accounts for several weeks riding SPY down from 450, but when it rose back up to 415, I un-hedged”. Trying to decide if it’s time to re-hedge.

Thats a great question, The only boomer account I have is my 401k. I moved it to cash back in January while new contributions go into the market. (For anyone reading this, I am not suggesting anyone do the same. This is what made sense to me and my personal risk tolerance) My plan is to dca the balance back into the market, but really just depends on how things evolve.

Outside of that I have a “End Game” watchlist I have been working on that is def boomer focused. Would like to accumulate shares of companies I believe will do well in the next few years, and sell CC on them for awhile. Names like SLB, HAL, PG, CVS, GIS, KR.

So as of now there isnt anything to hedge, but when I start deploying funds to the end game tickers that’ll most likely change a bit

I also moved my 401k money to cash for a bit. That’s how I hedged. But I’m back in SPY and QQQ for the moment and leaning toward going back to cash, at least for a % of the account. It sounds like you are sufficiently hedged against a downturn. Thanks for sharing.

First Treasury Notes/Bonds auctions after QT coming this week in the lead-up to CPI:

Tuesday is the 3-year Note Auction:

Wednesday is the 10-year Note Auction:

Thursday is the 30-year Bond Auction:

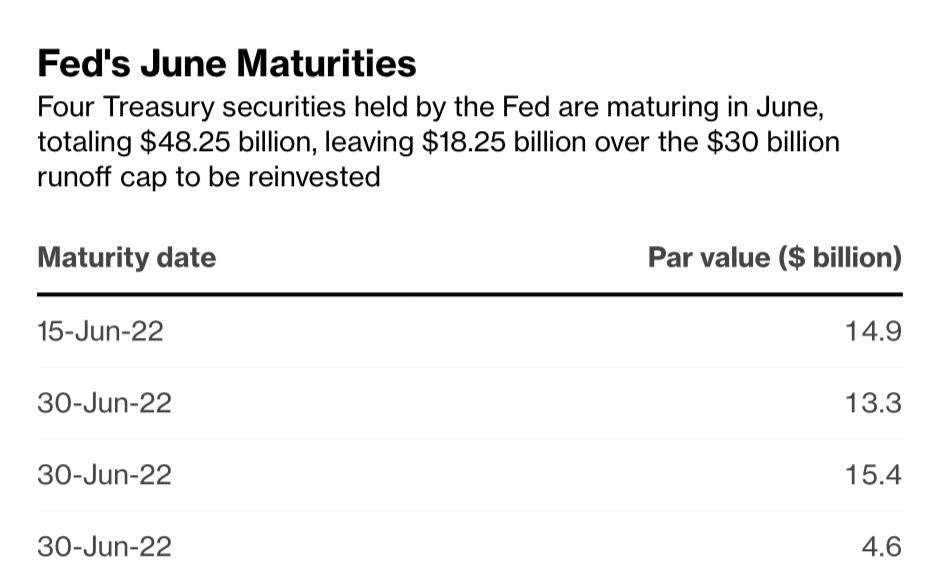

There’s $15 billion of SOMA Holdings maturing, of which only $5 billion will be re-invested and will be settled on the 15th. These assets mark the first to roll off the balance sheet

I just had a conversation with someone that works for DSV, if you don’t know they’re one of the largest transportation companies out there. Huge in Europe and in the US (through acquisitions). Anyway, she was telling me that available truckloads to move are down significantly - no one is moving freight like they were - and that has forced all the little guys that opened up in the last year or two that were drowning in work to reach out for new logistics companies and more or less beg for freight. But they’re not getting it. They’re too small and too unprofessional when there’s a glut of experienced trucking companies competing for freight too.

Lots of these guys acquire trucks and trailers through leasing or abusive lease-purchase programs. Margins are extremely tight, and they can’t afford to not have work for too long. It’s a dangerous mix.

DAT (Dial-A-Truck) posts analytical insights from their available posts each week. Their insights from the previous week support what I heard from DSV - loads being posted are down 24% from last week. https://www.dat.com/trendlines

I also found this statement interesting: May 30 – June 5 – We’ve been anxiously waiting for the seasonal correction in the recent decline in spot rates, and it may have finally arrived. Produce and grilling season typically provide a boost in demand between now and July 4, driving up line haul spot rates by as much as $0.30/mile in recent years, but not this year. Produce volumes are down 16% compared to this time last year or the equivalent of almost 30,000 fewer weekly truckloads of fruit and vegetables.

Is the abusive lease program debt securitized? Sounds like the smaller truckers will default once there’s no work available.

Also, I saw a chart today that showed that containers coming in from china → US dropped substantially, obviously that is directly correlated with trucking volume.

Hope everyone had a great day,

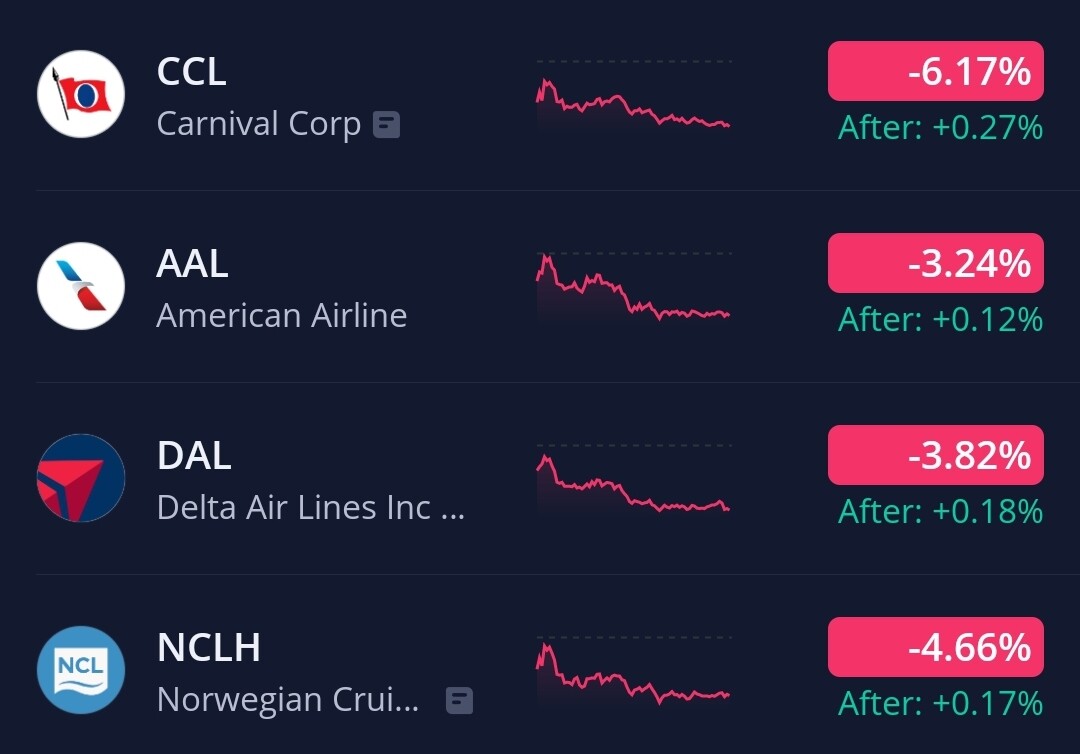

I want to mention Cruise Lines and Airlines again, they are currently feeling the pain from higher fuel prices and lower consumer discretionary income, and across the board financially haven’t recovered from Covid 2020.

I have been playing CCL, NCLH, DAL, & AAL with some decent win rates and gains.

Also like how easy it has been playing option on them, if crude is up and the market is trending down, they typically just bleed out making it easier to enter / exit.

CCL has earnings on June 27th, last ER they reported a 7.5% increase in revenue, nowhere near where they need to be, and a 3.9 billion dollar change in free cash flow. They noted trends in bookings looked strong but as of the end of March they were still only at 70% fleet capacity and roughly 60% occupancy. They have recently also had to cancel a number of cruises due to weather developments, and the airline industry isn’t doing them any favors with flight prices continuing to climb. I will be playing CCL into earnings as I think the painful story will continue.

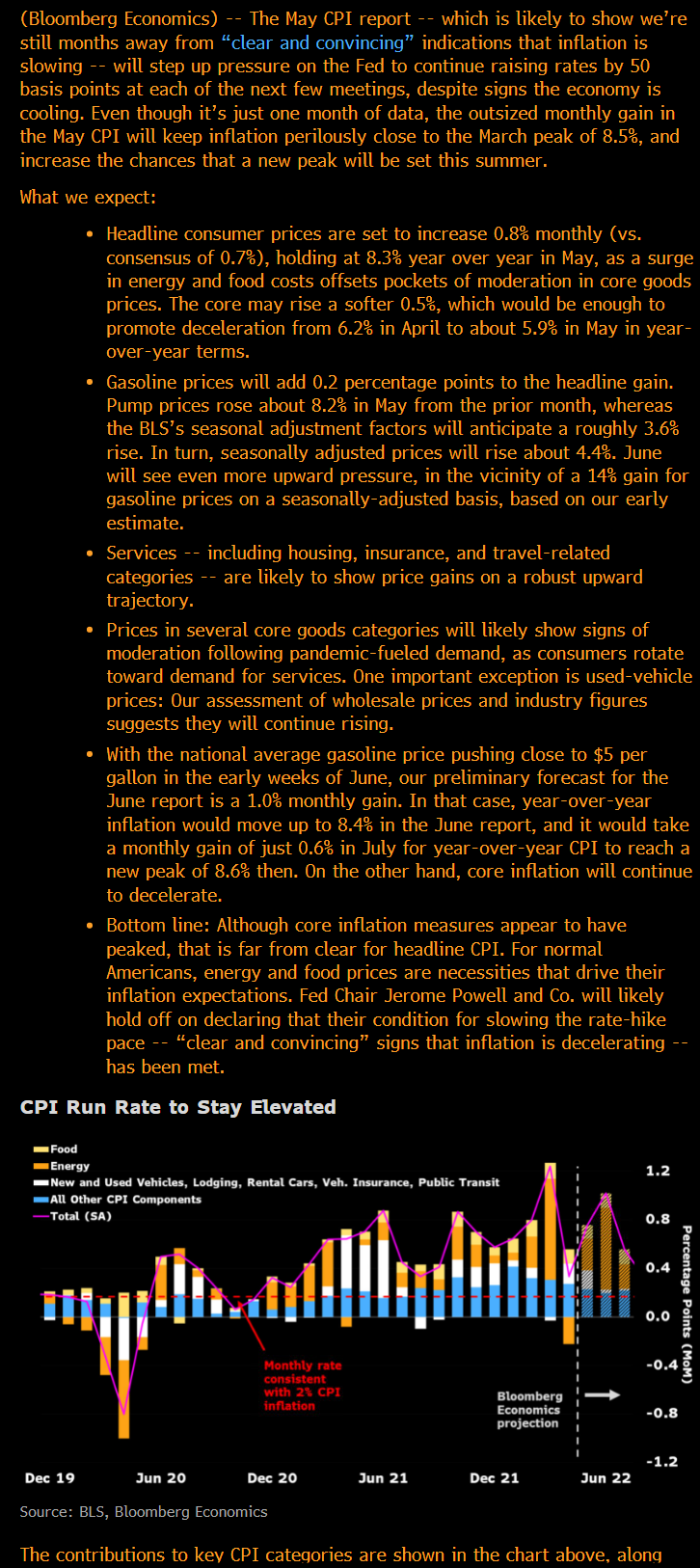

The Cleveland Fed has a model called inflation nowcasting that they use to predict what CPI will print at. Basically, by backtesting their previous predictions, they generally mildly underestimate the Actual print. For the May print, the model estimates 8.23, and the surveyed value from economists is 8.3. Perhaps we get an 8.4 tomorrow.

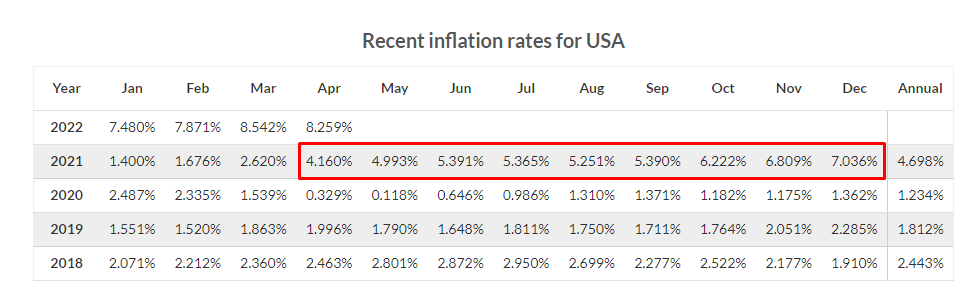

As seen in my red box, CPI started rocketing in April onwards. We also got the first sign of ‘decelaration’ last print going from 8.2542% to 8.259%. I wonder if by comparing YoY numbers with relatively high numbers from last year, that in this way the CPI headline print might get alleviated? Might give the CP-Lie cooks some room to play with.

If PPI also comes in hot, hard to see how markets won’t keep going doooooown in the near term, as almost everyone expects. (With some very short-term kinks to that possible becasue of opex, but we’ll deal with that in one of the relevant SPY threads.)

Just incredible. And every bit was earned with all your consistent hard work in this thread and in the community at large. Congratulations!

On the topic of bearish sentiment, I am having my fourth meeting with a large lender this week in the last four weeks. They are all worried about the economy for obvious reasons. The big takeaway is that supply chain is no longer an issue for many manufacturers even though they use that as an excuse. They are sitting on massive piles of finished goods but no retailers are buying. This is consistent with the story last week about TGT liquidating inventories. Many of the large retailers have told manufacturers not to expect any sales in Q2. So mark this post because manufacturing Q2 earnings may look pretty bleak.

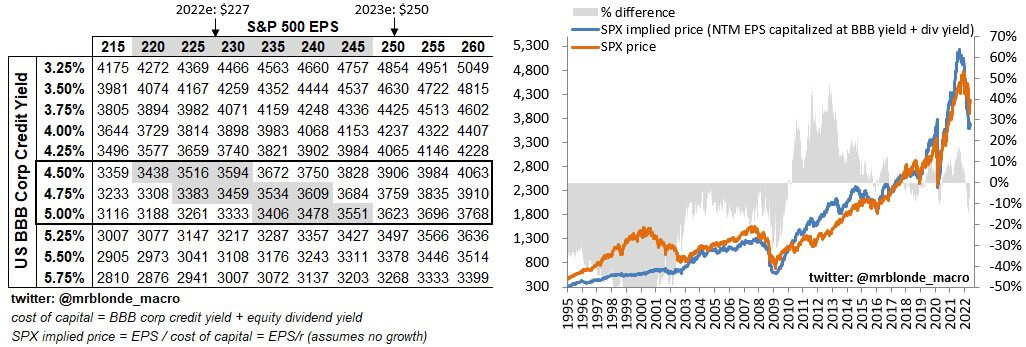

Also wanted to leave this here that @juangomez053 shared in TF. It assumes that markets care about fundamentals again (which is does) and takes a terminal value approach (which is not quite accurate of course, but given the big picture, it is directionally correct enough) to SPX. And finds that we still have a bit to fall.