I didn’t write, but I did think it was worth sharing (it is from one of my bomer accounts newsletters)

Economy Snapshot

• Unemployment rate: 3.6%

• 30-year mortgage: 5%

• Inflation: 8.5%

• Target Federal Funds Rate: 0.25% - 0.5%

With all the talk of inflation in 2022, you may be hearing another term: stagflation. The big fear is that as the Federal Reserve (The Fed) attempts to engineer a so-called [“soft landing”]) for the economy by increasing interest rates, it will spark a recession with widespread layoffs.

The irony is that after so many years trying to increase inflation to its target 2% goal, the Fed is facing more inflation than it can handle, with record price surges and the Consumer Price Index (CPI) registering [8.5%]( inflation.

High inflation coupled with high unemployment and low economic growth is the definition of [stagflation]), and we’ve been here before.

In the 1970s, the U.S. experienced a period of persistent and severe stagflation, brought on by an oil shock and the doubling of energy prices twice during the decade. The first oil shock occurred in 1973, following an embargo by the Organization of Petroleum Exporting Countries (OPEC). The second occurred in 1979, stemming from the Iranian Revolution. From 1974 to the end of the decade, unemployment averaged 7.9 percent, while inflation reached 8.1 percent, according to the U.S. Bureau of Labor Statistics.

The oil supply shock in 2022 resulting from the Russia-Ukraine conflict is eerily reminiscent of these periods and is exacerbated by the fact that so many nations rely on Russia for their energy resources. While the issue is more prevalent in Europe than in the U.S. due to a greater reliance on Russia, the U.S. still remains a net importer of oil in general.

A surging U.S. economy

The U.S. economy is proving that inflation by itself isn’t necessarily a bad thing. As long as jobs numbers are solid and workers’ earnings increase, an economy can still grow, although at a slower pace. And strong economic data in the U.S. provides a solid backdrop for Fed officials to continue raising interest rates to help combat inflation.

Total nonfarm payroll employment rose by 431,000 in March, 2022 and the unemployment rate declined to 3.6% (from 3.8% in February). Led by job gains in leisure, hospitality, professional and business services, retail trade, and manufacturing, the U.S. economy appears finally to be returning to pre-pandemic numbers. This report marks the 11th straight month of job gains above 400,000, the longest such stretch of growth dating back to 1939.

Average weekly earnings continue to climb in 2022. Jerome H. Powell, the Fed Chair, even said, “The promise of wages moving up is a great thing.” Wage increases, in conjunction with leftover stimulus checks, and savings from pandemic immobility help support the average American in light of decreased purchasing power.

But the Fed’s ability to increase interest rates without harming the economy will determine whether the economy can navigate this period of hyperinflation without provoking a recession, and that’s an open question, according to investment bank Goldman Sachs.

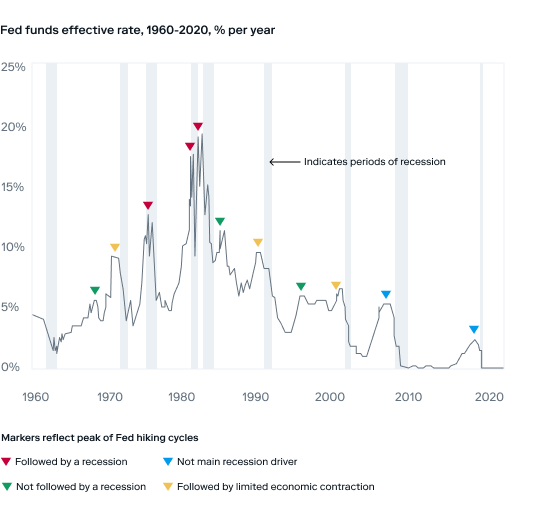

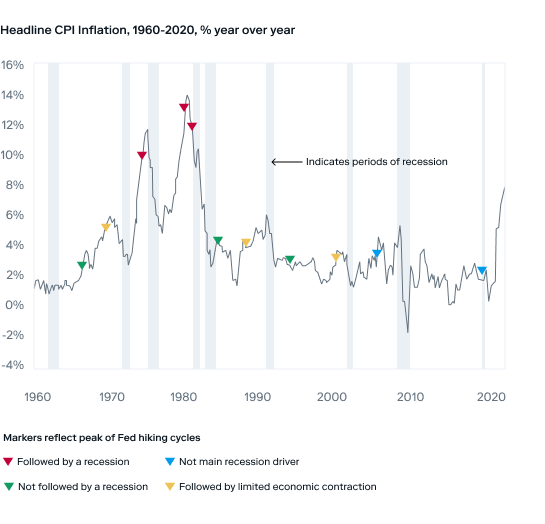

Check out the following chart to understand the correlation between Fed rate increases and recessions over the decades:

Interest rate hikes and recessions

Source: Goldman Sachs GIR, 2022.

Understanding inverted yield curves

One glaring signal of a potential recession, however, is the recent inversion of the Treasury yield curve for 2-year and 10-year notes.

Here’s what that means. Normally, longer-dated bonds, such as the 10-year Treasury, command higher yields than shorter-dated bonds, like the 2-year Treasury. You can visualize this concept as an upward sloping yield curve, with longer-dated bonds providing higher yields. () This is because investors typically want to be compensated for investing over a longer period of time.

Yet, investors are currently driving down yields and buying up bonds with longer maturities—such as the 10-year Treasury—driving yields below shorter term maturity bonds. This results in an inverted, or downward sloping, yield curve. Typically an inverted curve signals that investors believe a recession may soon come, and the Fed will have to reverse course and cut interest rates in the future.

Remember that bond prices and yields are inversely correlated—so the outcome is an inverted yield curve where short-term bonds command higher yields and lower prices than long-term bonds. Good to know: As recently as 2019 we saw an inversion of the 2-year and 10-year Treasury yield curves, but no recession followed.

Yield curves may predict recessions

Nevertheless, the economic data remains strong enough to assume that the economy can withstand further inflationary pressure and numerous additional interest rate hikes in 2022. Only time will tell whether the Fed delayed too long with its first interest rate hike.

European economies are showing signs of weakness

European nations are far more reliant on Russia for energy resources than the U.S., and that poses a larger potential risk to those economies. Until recently, pandemic-induced supply shocks primarily caused inflation. And investors expected price pressures to alleviate in the first two quarters of 2022.

The Russia-Ukraine conflict upended expectations about inflation, and comparisons to the 1970s are now more stark, as energy prices compound existing price increases. As in the U.S., European Central Bank officials had a clearer path towards combating inflation using monetary policy (i.e., raising or lower interest rates). But geopolitical turmoil has added uncertainty to forecasts.

Prior to the conflict, expectations for annual growth in the European Union through the fourth quarter of 2022 were greater than three percent. Economists now forecast growth of approximately 2.5%. The United States has higher growth expectations for the year of 2.9%.

Possible spillover to U.S.

The U.S. recently started blocking Russia from making debt payments using dollars held in American banks, in an effort to starve Russia of its international currency reverses. Russia has since resorted to paying its debt in Russian rubles, as opposed to American dollars, as its contracts stipulate. This breach has increased the likelihood that Russia could default on its debt, which could have drastic consequences for the Russian economy, such as restricting its ability to trade with other countries. The cost of insuring Russia’s government debt now signals a record 99% chance of default within a year. Good to know: Russia’s debt default in 1998 had global economic repercussions.

Investing to combat inflation

Holding too much of your assets in cash is a sure way to lose during periods of inflation. At the current level of inflation, a dollar today will lose half of its purchasing power that can cover at least six months of expenses will ensure that you have financial security in the event of an emergency.