[Edit 9/19: Realizing this is the incorrect screenshot… return profile similar enough though.]

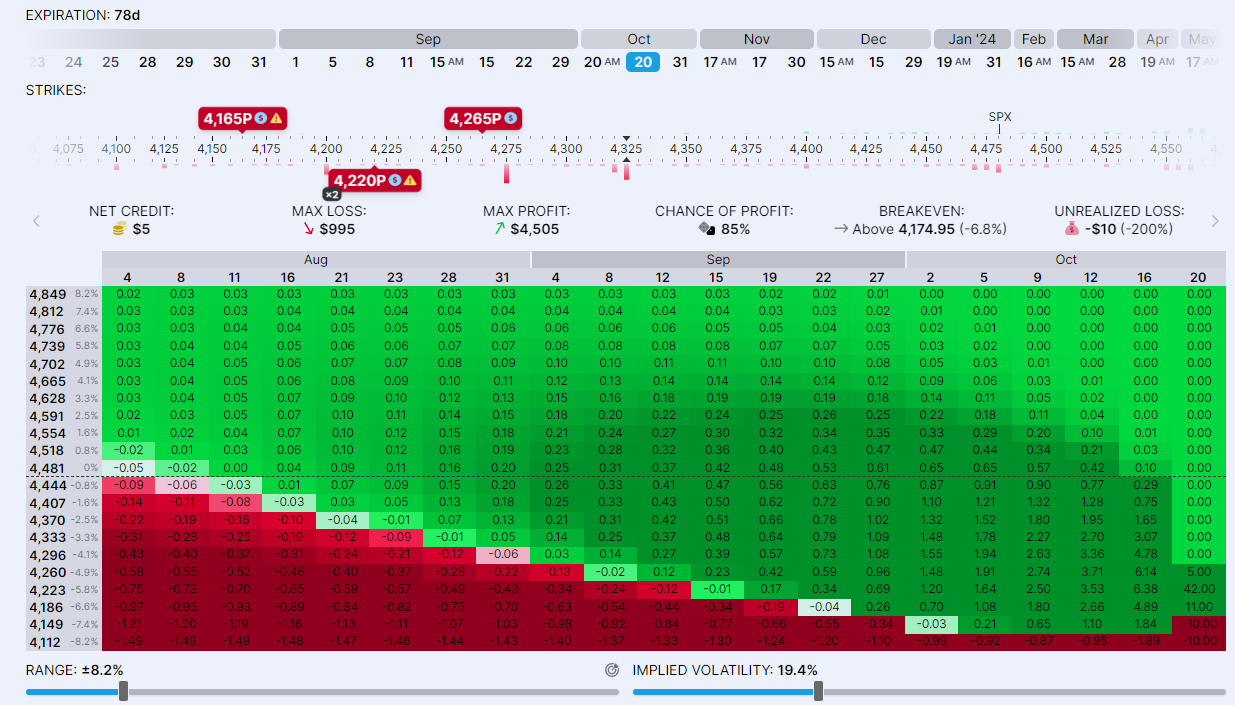

Why these strikes? JPM put collar strike is at 4215, and 5 out of the last 7 times, market was very close to one of these strikes when they expired. The 4200 area is also a decent support area, so if there is a plunge, should rest there for a bit.

Sold the put portion for $0.17. Technically that’s a 8.5x return on the initial outlay, but since max loss was $102, it’s more like a 16% return on risked capital.

This had the potential to work out very nicely as one of the strikes needed to be close to the money, which was almost the case up to just before earnings. Ah well.

8/24 (1DTE) SPX 4495C/4510C/4545C call butterfly for $0.25, if NVDA does what the masses are demanding - targeting a 4500 close tomorrow

8/25 (2DTE) SPX 4325P/4300P/4255P put butterfly for $0.20 as insurance, in case a 1-2 punch from NVDA and Jpow sends markets reeling - targeting a 4300 close on Fri

If the past is any guide to what will happen, well likely close right at 4400 on Fri

This for today didn’t works, but got some more for tomorrow cause they are so cheap:

8/25 (1DTE) 4490C/4505C/4520C call butterfly for $0.10 - this is for the bull case for tomorrow, and complements the 4300P bear position I took yesterday.

Also got more MULN because this is an artificial pump happening to stay in compalince. That’s a ~10 day affair, so got 16DTE options:

These are amazing fills for OTM put spreads - so much so that it is likely I will somehow get screwed, and just don’t know how, yet. Only way to find out is to f*ck around though, so got a handful only - for the sake of science.

I don’t expect these to expire OTM by any means, but counting on the spread value increasing more than where it is now, as price falls. And if it doesn’t… I’m out of pocket $25 and $50 per contract, for a potential $450-475 gain.

Context for those to whom this is a new ticker: VFS is a Vietnamese EV maker that did a de-Spac, has < 1% FF and ultra-low float, has warrants exiting lockup in 30 days, and shares in 180 days. Unless there’s an offering, prices could remain elevated for a while.

Btw while ITM call spreads look awesome too, with their own $4.90 credits, they have major assignment risk, and subsequent loss because of short fee overnight. Hence went with OTM put spreads.

Closed out the Sep spread for $4.25, making $0.25 per contract. And the Oct spread for $4.60, making $0.15 per contract. Based on capital risked, that’s a 53% return.

Cannot complain, but kinda disappointed as this could have been so much more. VFS fell 40% today, and one of the spreads went into the money, so liquidating this now was the only option; was not going to hold overnight and find out bad things tomorrow.

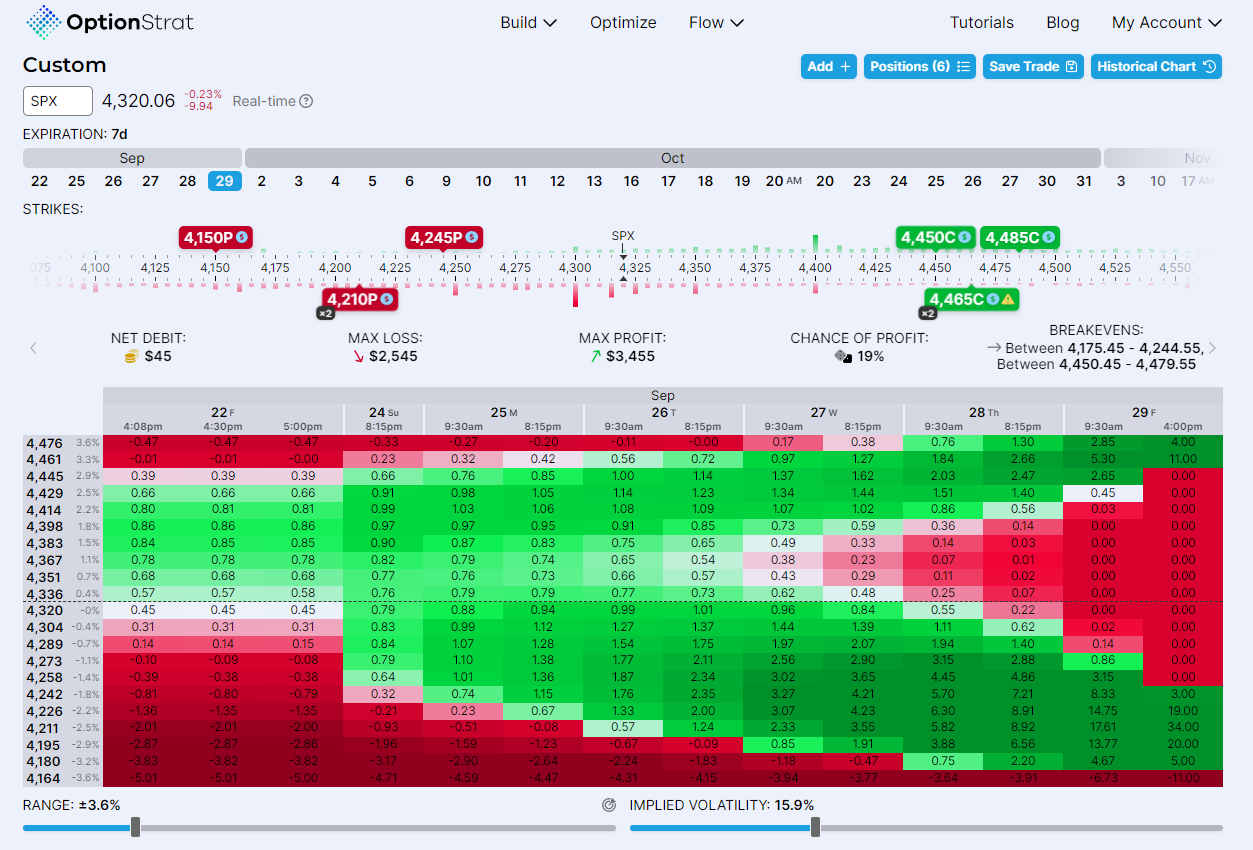

Ok I lied when I said I was going to sit on the sidelines until CPI… took some lotto butterflies that will work out if we pin to one of the major OI levels. They are XSP so I can scale in and out while still lotto-ing.

SXP/XSP is around 4450/445 at the moment. A 100-pt (~2.2%) SPX move - and therefore a 10-pt XSP move - is a bit more than what options are pricing in (+/- 60 points), but then we have CPI and opex, and we are in negative gamma, so long odds felt lotto-worthy.

With less than hour to go, all these are now destined to expire worthless. No surprise, market pinned the middle of the range.

Nevertheless, the show goes on.

On one hand, this is probably the most balanced I’ve seen the markets be in a long whlie, both in terms of technicals and underlying gamma structure. (Threading the 20SAM and 50SMA, and roughly the same amount of puts and calls expiring today near the money.)

On the other, vol is super low, there is FOMC next week (source of vol), and many indices are showing H&S patterns. Flows should really have provided tailwind these last two weeks; that did not happen suggests underlying selling tendencies. If all this option magnet stuff was holding markets up, then… we could go down, now that that support has been removed. Also, overall, there are more puts than calls, and a lot of them expiring today would remove cushion from downward moves.

I learned about something I had never heard of before over the weekend and hoped to get your thoughts on it. YouTube guy blamed Fri sell off on 50% of company’s being in a “blackout” out period. Apparently about a month before earnings, many companies prevent certain employees from buying or selling said companies stock due to potential insider trading violations. Pension funds also. The theory goes that volume drastically decreases during this time which tends to lead to a predictable downturn in the market the last few weeks in sept unless retail investors step up. I’ve also read a paper that disputes this over the weekend. Is this anything you are familiar with?

When I worked for a publicly traded company, this was the policy: Blackout periods begin 15 calendar days before the end of each company fiscal quarter and end two trading days after company’s public announcement of its financial results for such fiscal quarter. It adds up to a LOT of time that you can’t trade your employer’s stock as an employee.

Hmm, had not heard of that before, but sounds interesting.

It’s not just the 15th that is the blackout window though - it’s from then on to whenever eanings happen. Shouldn’t price be depressed during that entire window?

It would also need the insider trades and buybacks to be a significant portion of the volume. (The video suggests GS’ buyback desk sees 35% reduction in volume, so its not the full removal either.)

I’d like to see some real numbers behind this, if possible. In similar rigor to the paper you linked that shows the opposite.

And this is not anecdotal, but here are the last 4 such days before Sep:

15th Jun: 1.22%

16th Mar: 1.76%

16th Dec: -1.11%

15th Sep: -1.13%

A bit all over the place, but also, big moves. Personally, I think it has a lot more to do with quadwitching around opex, which happens on or a few days of that date, than buyback blackouts.

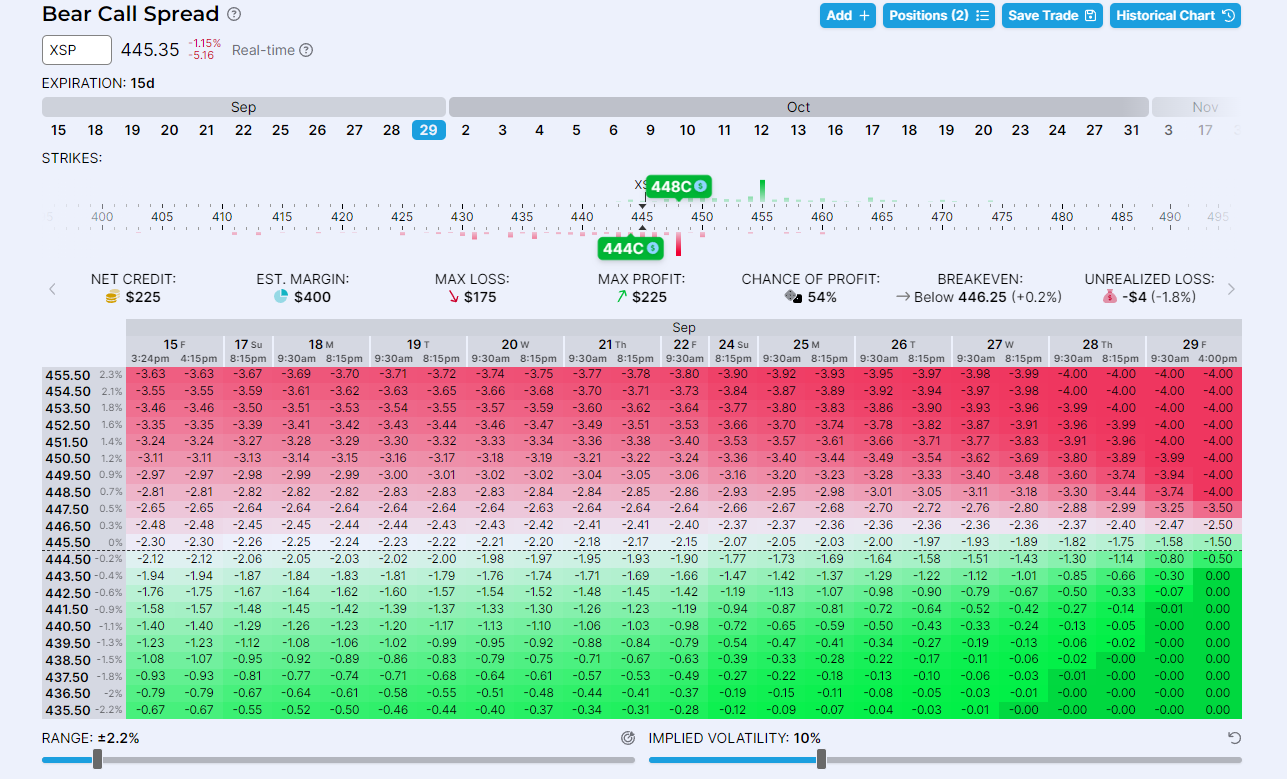

Closed this for $1.70, keeping 24% premium. Nice drop today, market may hold into FOMC tomm, so closed position.

Closed half of these for $0.50. Since I opened it for $0.05 credit, that’s a … 11x return? vOv Will liquidate the other half depending on how FOMC goes. (Had opened this 6 weeks ago, 2 weeks left to expiry.)

SPX looks like its testing the bottom multiple times, and $0.05 credit → $1.55 credit (31x ish) will suffice for now.

Will likely plow a chunk of this for a similar return profile at the end of the day, based on where market ends up, as I still want to have that JPM strike play.

Closed 1/2 out at $1, remaining 1/4 expired worthless. Frankly got really lucky with the exit - we still closed 40 points away from the closest long strike… such is the leverage of flies. Profit 185% - cannot complain ofc; will try to thread the needle again for the Dec JPM hedge expiry.

")