I’ve mentioned this before in TF and possibly other threads, but I’ve seen quite a few articles talking about potential “widespread blackouts” across the country this summer from numerous news sources. Not sure if it’s just fear-mongering or something that could really happen, only time will tell.

Essentially the red flags are increased demand (due to extreme heat), less power generation, and ageing infrastructure…

This article just appeared today so thought I would post it.

Somehow this didn’t show up on scans earlier in the day, and market also seems unfazed by it?

The US Empire State Manufacturing survey, which shows new orders 6 months ahead of time, has now dipped to levels similar to those seen during the GFC and the dot-com bubble:

More details in this report, where all forward looking estimates are crash-landing:

Adding to “Conq’s super anecdotal potential indicators”…. Stuff on Facebook Marketplace in multiple regions seems to have completely crashed in value. Furniture, appliances, etc are incredibly cheap as far as I’ve seen.

Thinking out loud, in 2008 e-commerce was still in its infancy for the most part, but now with how widely available these sites are (and how widely used) there’s a potential that the pricing of these good could indicate demand destruction a little before retailers. Most of these items are being sold by people that “want them gone” so if they’re crashing it’s likely the buying pool has dried up to some extent.

Of the 35 S&P 500 companies which have reported Q2 earnings thus far, 7 raised their 3Q22 EPS guidance, 1 kept it the same, and the rest of the 27 revised 3Q22 EPS guidance downward.

In an interesting set of events, I went to the local grocery store yesterday and it had that Covid vibe - I think they just got hit with more shoppers than usual based on the lines. I was mostly looking quick snack foods and things of that sort. Made we wonder if just the whole neighborhood did the same, instead of going out to eat. Or ordering delivery, not sure if it is unique to me or others noticing similar trends.

We may be seeing the correction on the USD. It’s been exceedingly strong, partly because of the comparative strength of the USD vs the rest of the world, and the potential for aggressive rate hikes. With recession coming and fewer hikes on the cards, looks like it might finally be cooling off now.

This will have all kinds of knock on effects, such as providing tailwind to stocks as they become cheaper to international funds, but in and of itself, we could see a decline in DXY. Or UUP, if one wants to play via an ETF.

I’m gonna summarize his PoV at about 20:30 on what to look for to reliably determine a ‘bottom’. Maverick suggests watching for these 5 indicators:

A cooling down of the 10 year yield.

Yield curve inversions have to stop steepening, and at least pause if not reverse.

USD needs to go down, e.g. DXY.

More participation in investors/traders buying call options, signifying more conviction in the stock market.

Inflation peaking + fed rate hike pause. Some argue that we have seen signs of this already, i.e. recent commodities pricing and recent inflation data.

In my personal noobie opinion, I think #5 is the most important for market sentiment.

& in the short term, all eyes should be on earnings and guidance for the possible ‘next leg down’ or perhaps a bear market rally caused by shorts covering/booking profits if earnings are strong.

Atlanta Fed GDP Now has revised GDP downwards just a smidge, to -1.6%. Doesn’t seem like market reacted to this at all. We’ll probably just wait for the real thing in 2 weeks.

DXY is dancing right on that support line. With bonds saying recession will come sooner, USD strength should really start to reverse soon. Not doing anything to UUP puts obtained a few days ago yet, but may add if we breach this line next week. GDP figures will definitely affect this too - lower GDP guidance should send DXY/UUP lower.

Unlike inflation numbers which were within +/- 0.2% of the median forecast for the most part, GDP forecasts are all over the place, ranging from +2.0% to -2.1%. Mean is 0.2%, with a standard deviation of 0.85%. Supposedly the big boys are more negative than the rest, although bulk of the forecasts are positive.

As always, the difficult question is, “so what?” One thought is if GDP print is good, Fed could be expected to raise rates for longer, or at least not reduce them as quickly as they are expected to, now. This may lead to a rotation out of growth and back to value.

What else do you think might be the implications of this?

If GDP is even slightly better than expected and because data so far suggests inflation may have peaked, I believe it would be a catalyst. Market pricing in uncertainty with the possibility of significant GDP decline for second consecutive quarter currently.

Right now, I’m feeling like GDP print will be negative, but not nearly as negative as Atlanta Fed or some of the institutions are forecasting. Reasoning:

The White House recently “clarified” Recession as not being two consecutive quarters of negative GDP. Unlikely to have done that if GDP was going to be positive.

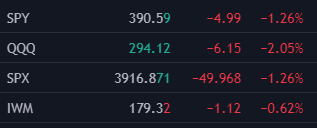

IWM is behaving much better than SPY and QQQ. If GDP was going to be very bad, it’s the smaller caps that would have been clobbered more. Fed rate probabilities have also ever so slightly moved toward higher rates for longer.

Maybe we’ll get clues in the FOMC presser tomorrow too on how GDP will be. If this prognosis of “negative GDP, but not that negative” holds, then maybe long IWM, with short QQQ as hedge, might be a play into Thu.

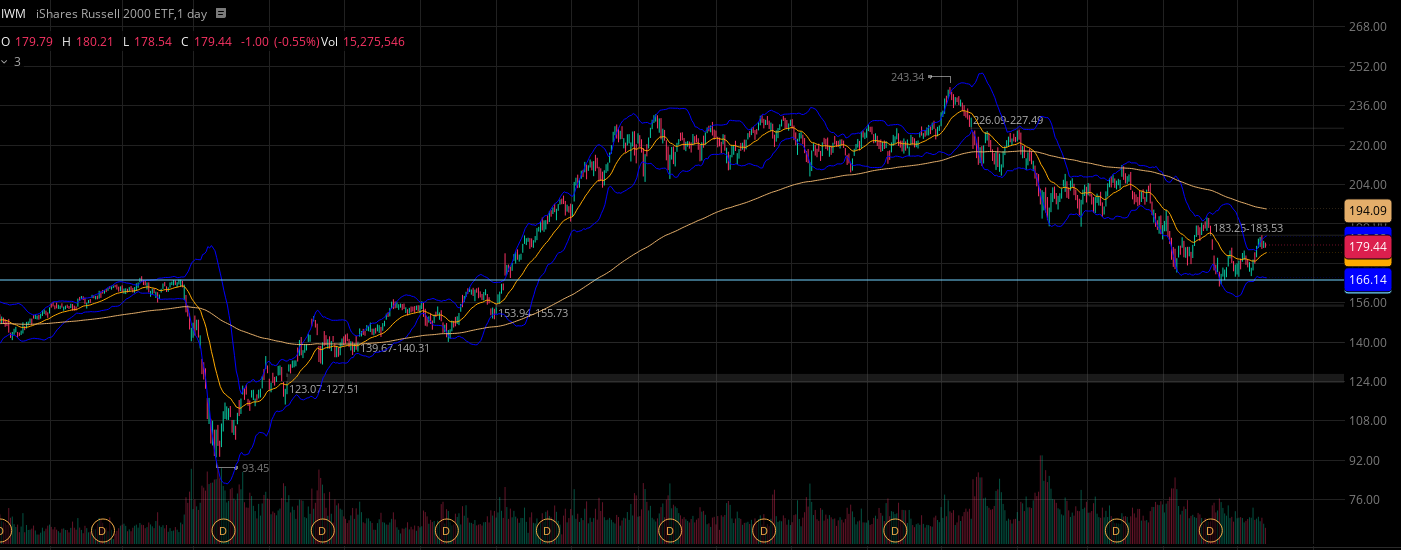

One thing to note is that IWM is much closer to its price “pre-covid drop” than SPY… So maybe those stocks have bottomed out already and just waiting vs the mega & large caps?

The implications are: the Fed could stop providing forward guidance.

Nick is the WSJ journalist who the Fed used to “leak” the impending 75bps rate hike last time around. This time, he’s talking about the Fed no longer providing forward guidance. I suppose it makes sense at some level - with loss of credibility, not many are taking Fed guidance or chatter as seriously as they would like. Yet, it still matters, so economic signals are perhaps not being incorporated into the markets as quickly because of expectations from the dot plot and such. (Associated WSJ piece.)

Removal of forward guidance would be disconcerting to markets though, and could significantly add to volatility. This piece by NIck came out today morning, so could explain the market’s reaction, though perhaps folks are looking at the Fed confirming it tomorrow, if at all.

“We’re seeing no evidence of a pullback in consumer spending,” Chief Financial Officer Vasant Prabhu said on the company’s earnings call.

Executives acknowledged that consumers could well be changing their behaviors, but not in a way that would show up in Visa’s results.

“What we don’t know are what level of substitutions are taking place, where people might be buying more staples and less discretionary items but they’re spending at the same level they did, or whether as some retailers have said, people are trading down from brands to private labels,” Chief Executive Al Kelly said on the call, according to a transcript from Sentieo.

He added that “clearly, inflation is in our numbers and people are likely… making some changes on what they’re buying,” but “they’re not changing how they’re paying.”

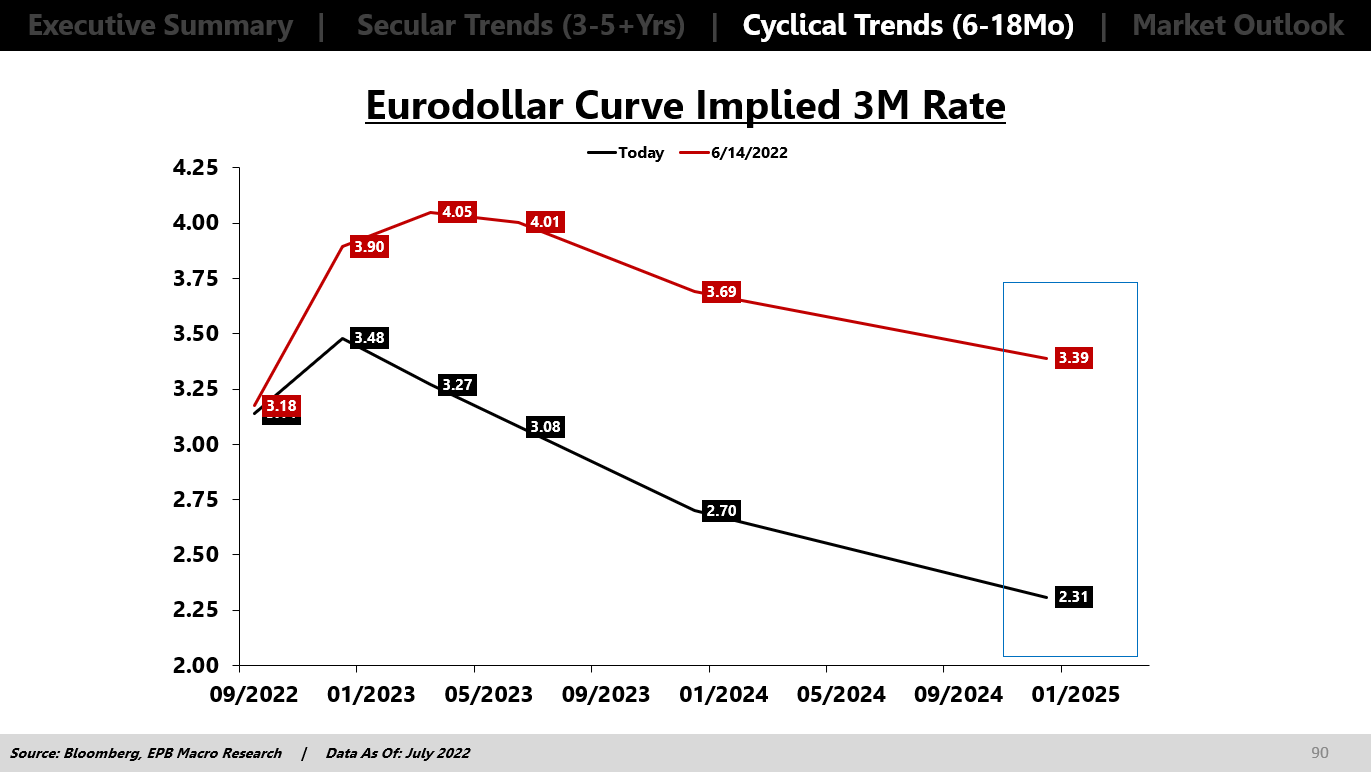

On the other hand, market is pricing bonds like recession is imminent-er, requiring major rate cuts within 6 months, which is drastic compared to where we were just a month ago:

Visa earnings seem to align with what we’ve been seeing with credit card spending at all time highs. A payment processor company such as Visa should benefit well from the current environment where consumers are forced to chase their monthly payments and continue to swipe their cards and go into deeper debt.

Todays run seemed odd to me given the gdp data and overall economic outlook. Makes me think it was due to frontrunning Amazon and Apple releases, maybe the positive numbers got out early in some circles. If so, market May be done pushing till there is another catalyst.

As mentioned by others as well, a bullish market move based on negative GDP could be because bad GDP = less incentive for the fed to do more aggressive rate hikes. The negative GDP suggests that maybe the fed is actually somewhat doing what they set out to do.

Next notable catalysts are PCE numbers tomorrow morning, which JPow has said the fed will be watching carefully, and then CPI data on August 10. However, the next CPI print is expected to be ‘bullish’ in showing a slight slow down in inflation. Nonetheless, even if we see some evidence of ‘peak inflation’, a sustained elevated high inflation is problematic. But I can see the market ignoring that and just rallying based on ‘peak inflation’. We’ll see.

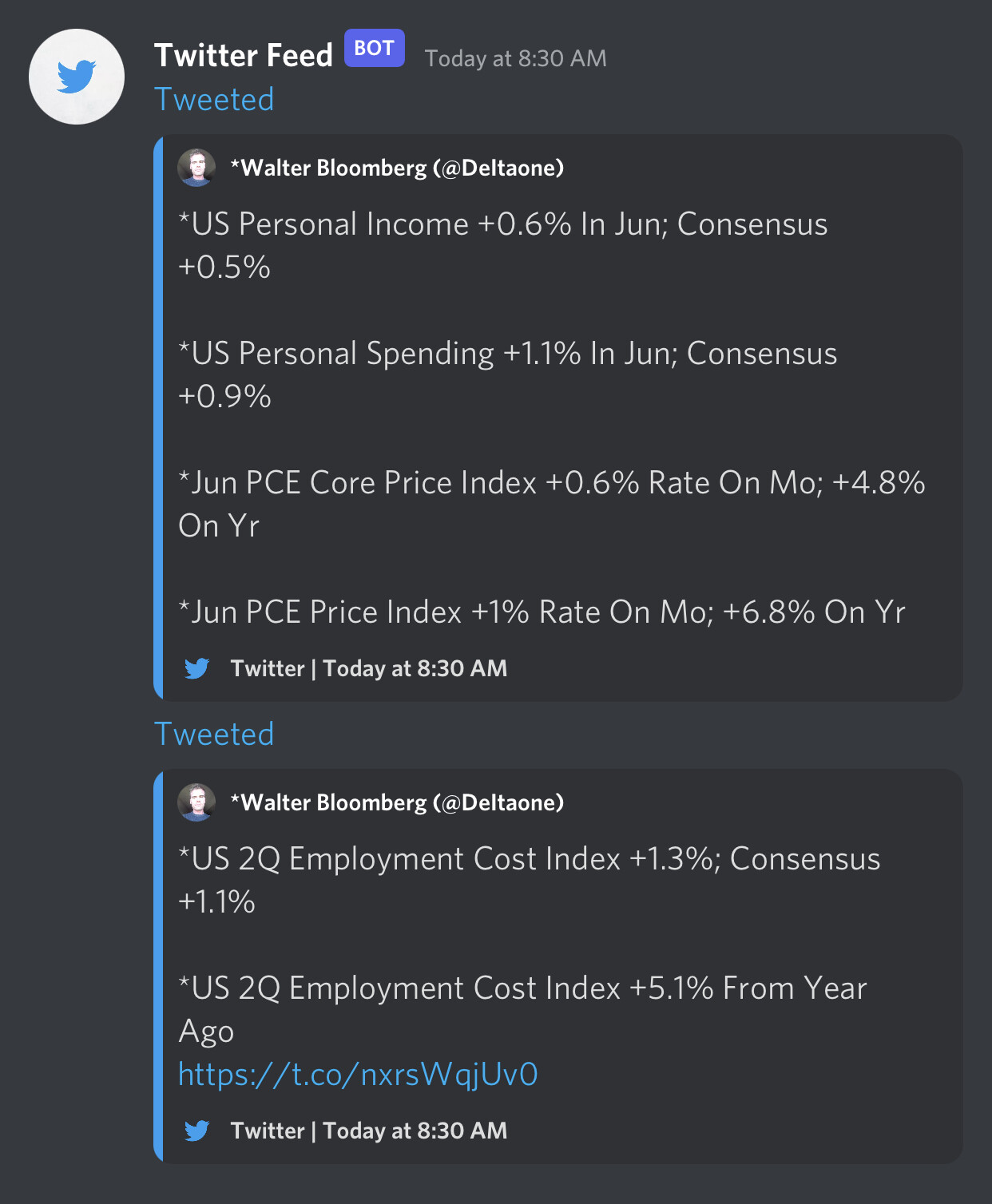

The core PCE numbers came in higher than expected but not so much higher to cause market panic. Since the Fed is now on vacation, my prediction is that the Fed will look at this and think its 75bps increase on Wednesday will do enough to bring down these numbers. I don’t think these numbers make any difference in terms of policy in the short-term. July numbers announced in August will be much more of an indicator of a potential policy shift.