The last two weeks have seen a significant shift in the market’s inflation expectations, since the payroll numbers came out. Jim Bianco lays out the important bits in this thread. Main points:

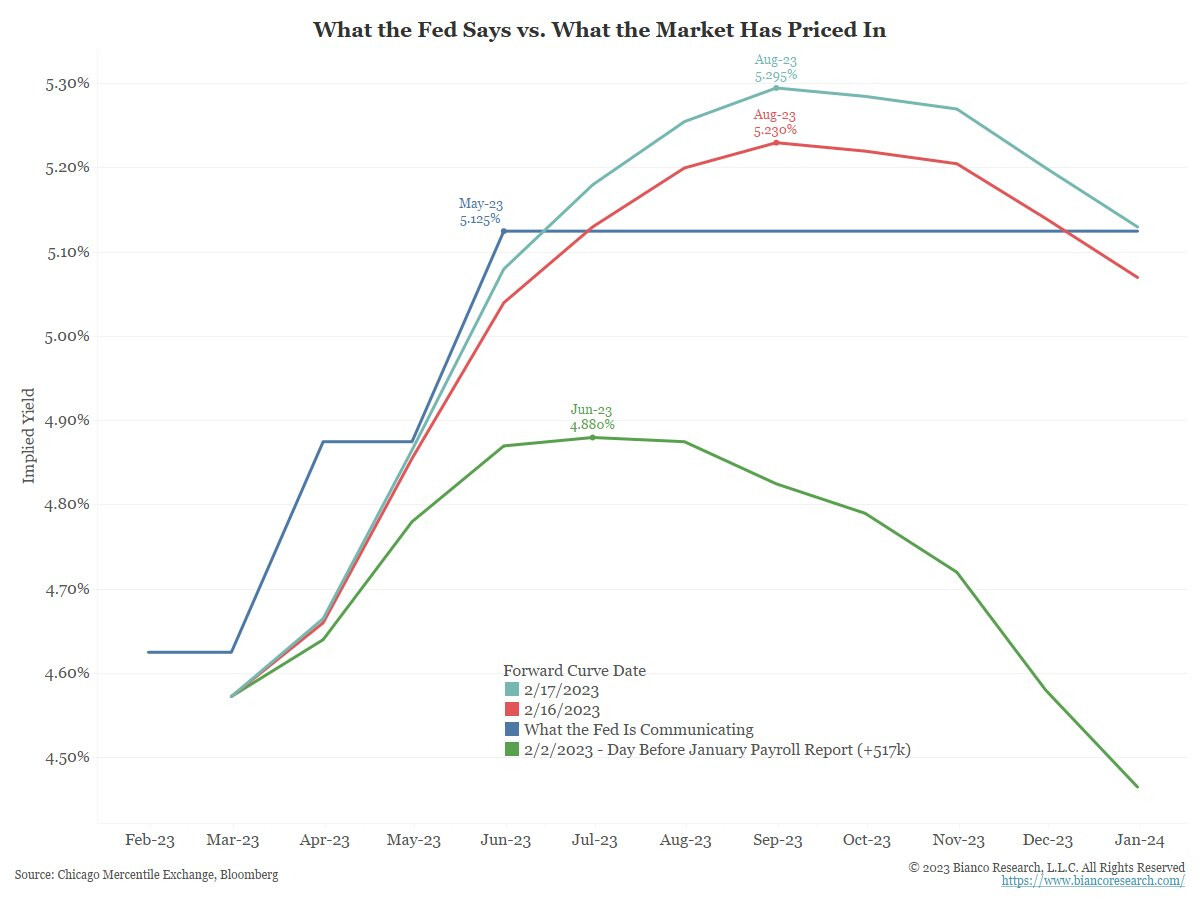

- Forward curves no longer pricing in a pivot in 2023. (Image 1)

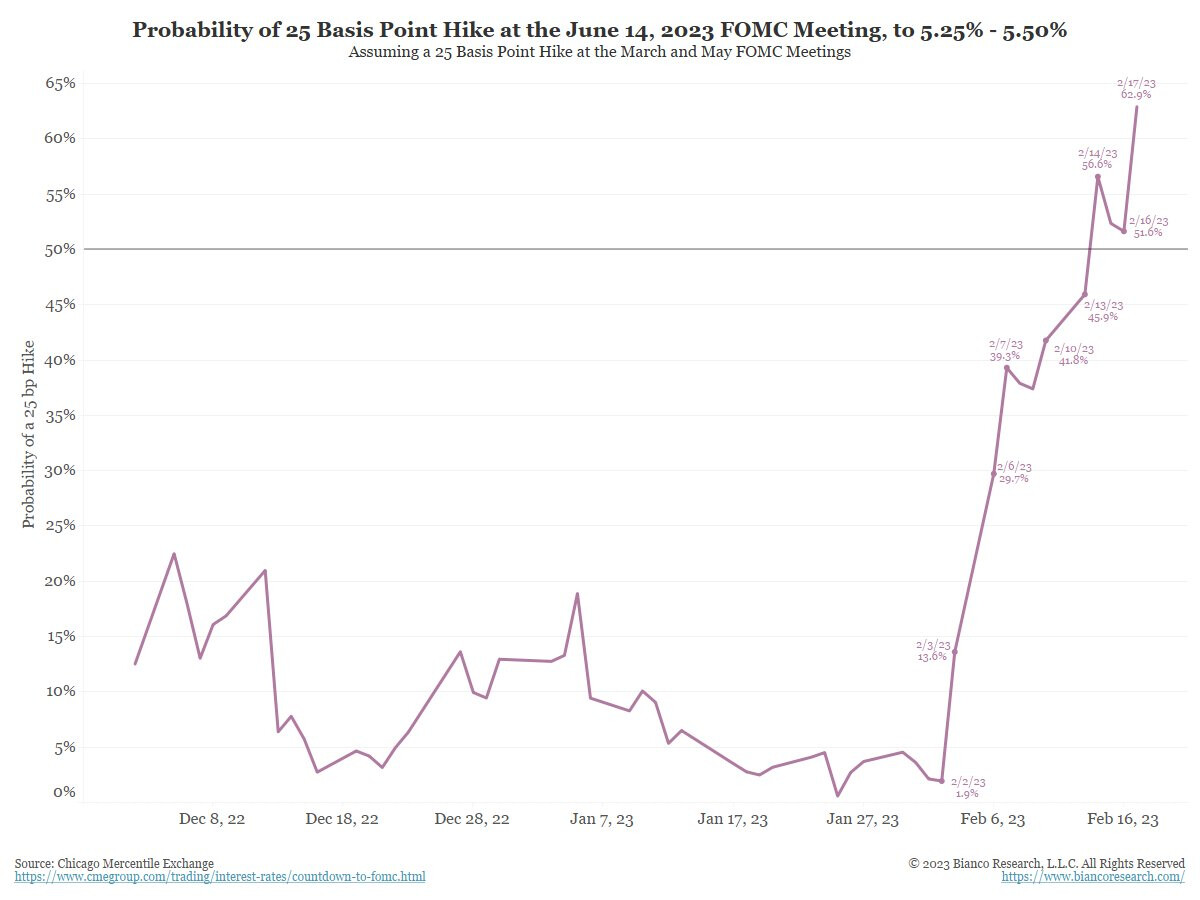

- Probability of 25bps hike in June went from 2% to 63%. (Image 2)

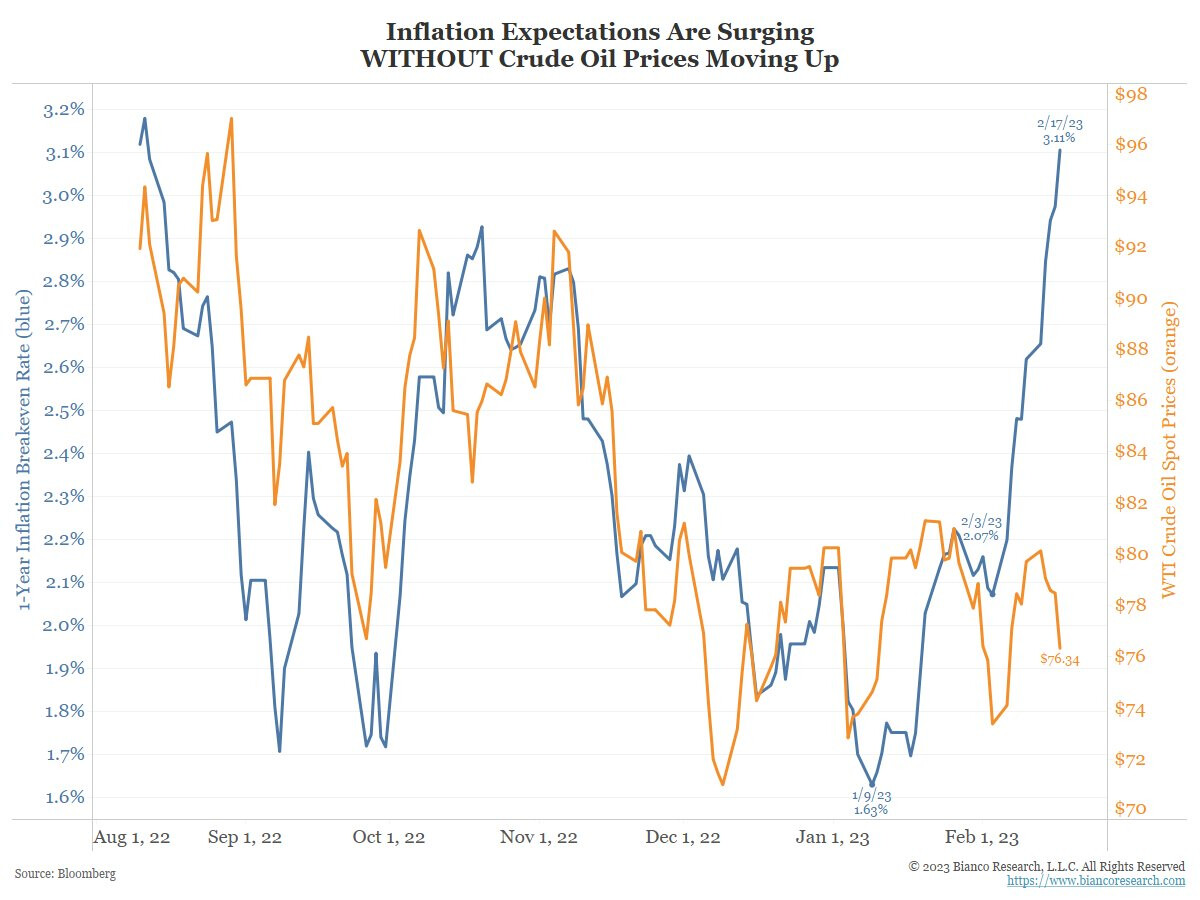

- Oil prices are no longer seen to be driving inflation, given divergence with crude. Given this reaction to payroll numbers, seems like wage-price spiral is the key driver. (Image 3). UMich research noted this possibility 11 months ago, and we took a closer look at this in Dec.

- 1 year inflation expectation went from 1.6% in Jan, to 2% 2 weeks ago, to 3.1% now (Also image 3 - left axis).

Apart from the impact on the stock market in general, what specific plays could we see out of this? Especially considering the fact that the equity market has not responded to this like bond markets have?