Thank you @SuckyMayor - that looks like a great approach! The market has been reacting well to this kind of macro news, and would be nice to ride it until its no longer a thing (like Fed staff jawboning about).

Big picture, bond yields are going up across the board. From the short end to the long end. We see that period of confusion in the bond market in the middle between mid-June and end-Jul, but since then, there does not seem to be much doubt in the mind of the bond market.

In comparison, the equity market is still at a much higher level than it was in mid-June, having retraced back only half of the way from its highs. If anything, it should be lower than where it was in mid-June because the short end is even more elevated now.

On top of that, some think the bond market is still being dismissive of the Fed, assuming that rates will not have to rise above 3.5%, and that the Fed will be ok with a 3% inflation rate in the long term. MacroAlf fleshes this out in detail:

All in all, while we might enjoy brief rallies, all this makes it hard to see how the rate-related downward adjustments stop here. Personally, I think we’ll see another low around opex.

(And we haven’t even started modelling the economic slowdown related market adjustments yet. )

This is a really great convo here. I wanted to share some insight from the retail side of things. So typically the two largest ticket items consumers spend money on are housing and autos. Meaning a larger percentage of their disposable income goes to these things above all else.

I hadn’t noticed much of a slowdown from demand aspect of things or gross profit… So I went back and looked at our organizations 9 locations total sales gross profit for the months of May and the months of August ending yesterday. Now these numbers are only sales numbers not including any parts and service revenue. Also to be noted May is perennially in any economic times one of the strongest months of the year. August typically sees a slowdown from summer months due to back to school etc.

May 2022 4.9 million

August 2022 4.8 million.

Also keep in mind there have been nearly 2 points on a car loan increase between those two months. And demand has not slowed.

Our biggest issue is from the supply segment. I always think of supply and demand like it’s on a tilting scale.

Supply side falls the demand side goes up. Currently supply isn’t any better in fact slightly worse than it was a year ago this time. That means the demand side has not had a chance to level out to supply. My thought here is more from a positive standpoint that I’m not so dead set on an imminent recession. If demand is still rampant and supply slowly catches up it eventual leads to the scale sitting level but will be more of a slowdown than an instantaneous catastrophic collapse.

Yea the auto industry has been somewhat of a juggernaut this year, something you called months and months ago. This has surprised me, but I believe as you have mentioned is really driven by the supply side and what I believe is American’s cultural appetite for vehicles as generally the preferred status symbol of choice.

The counter argument would be that auto financing is at levels never before seen in history while auto monthly payments are as high as they have ever been. My bear case for the auto industry is based on sustainability. We know American household budgets are being squeezed, with the majority of Americans not prepared to cash flow a $500 unexpected expense all while the average new vehicle monthly payment is over $700. This is madness to me. But we keep financing like we cant help ourselves. Broad market defaults in mortgages, credit cards, and auto loans are already ticking up and I dont see any reason why they would slow down now.

Thats not to say the strong wont survive or actually do alright during tougher times, while demand may eventually cool, slowdowns are where market share really changes. Those that go in strong come out stronger, usually with a little less competition. Always appreciate your input and insights, your perspective earlier this year helped me immensely with my AN trade.

My caution here was to say I believe we are all in the right thinking that there is a downturn. However I am of the belief that it isn’t going to be some rapid fall from graces.

Much of the market has given up its covid gains however the economy has remained resilient to the inflation. In regards to auto repossessions they are in fact on the rise from 2021 largely in part to many lenders not wanting to be the villain during a pandemic. However they are not approaching pre covid levels. Here is an article from Cox automotive the industry leader in automotive data.

Largely in part my thoughts are what’s really an increase in a car payment in comparison to wage increases. Is the actual percentage of the everyday consumers net take home pay going to an auto payment out of line or is it consistent with their increase in expendable income.

For a recessionary climate to take hold we need to see the middle and upper middle class have some kind of strain from the current economic conditions and largely that has been unimpeded. Frankly the reason a car payment is now an average of 700 a month isn’t because Joe down the road buying a 2010 Corolla making 15 bucks an hour is signing up for a 500 dollar payment. It’s because the farmer outside of town is buying a 100k dollar truck.

I truly believe there is a likelihood in slowdown in the economy in fact I’ve been telling my employees at work it’s not always going to be this good for a year now.

We are in store for some down turn in the market but I think it will be more of a correction with many over inflated companies coming back to reality as opposed to some 08 or 20 drop of a cliff. Now I could be wrong there. But it is seemingly to me that the broader US economy is much more resistant maybe to an almost arrogant nature of current inflation and economy. Jobs are strong still for the most part decreasing but not some mass layoff other than in large over saturated tech companies. Demand is still obsessively strong. Supply is still dramatically low in many aspects oil food auto. Hell even in housing it’s still not even close to previous levels of supply.

But really who knows. Looking forward to all of us collectively navigating our ways through it. I have no doubt we will be ahead of the game.

Stocks are set for a third straight week of declines ahead of key US jobs data that could stir expectations for another sharp Federal Reserve interest-rate hike. A dollar gauge slipped from a record high and the euro strengthened.

US futures fluctuated on Friday, while European stocks rose and Asian shares fell.

The jobs update is expected to show healthy payrolls growth and follows a stronger-than-expected US manufacturing report. Traders increasingly anticipate another large 75 basis points Fed rate rise to cool inflation.

Concern that rising rates will hurt growth has weighed on markets, pushing global bonds into their first bear market in a generation. The Bloomberg Global Aggregate Total Return Index of government and investment-grade corporate bonds down more than 20% from a 2021 peak.

Investors are also exiting global stock funds at a fast pace, with the fourth-largest weekly outflows of the year in the week through Aug. 31, according to BofA citing EPFR Global data.

“We don’t have a lot of reasons to be bullish in this type of environment for the next couple of weeks and months,” Meera Pandit, global market strategist at JPMorgan Asset Management, said on Bloomberg Television. “Yet when we think about the longer term perspective and the longer term investor, these are the types of level that can be fruitful in the long run.”

Like you said, it sounds like we will be “coming back to reality” and likely won’t see a drop like in 2008 or 2020. Perhaps raising the interest rates has been the right thing to do.

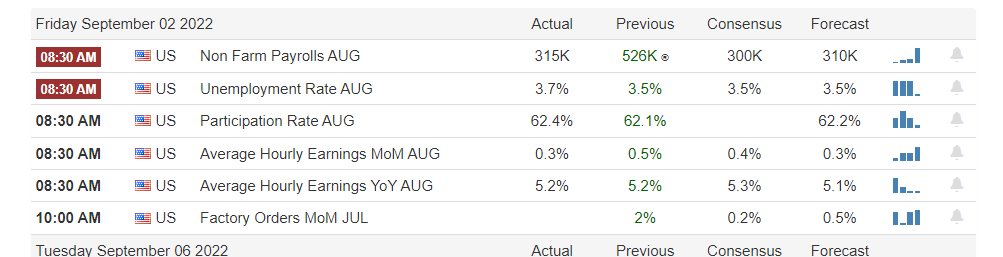

Unemployment came in .2% higher than expected

NFP came in less than expected

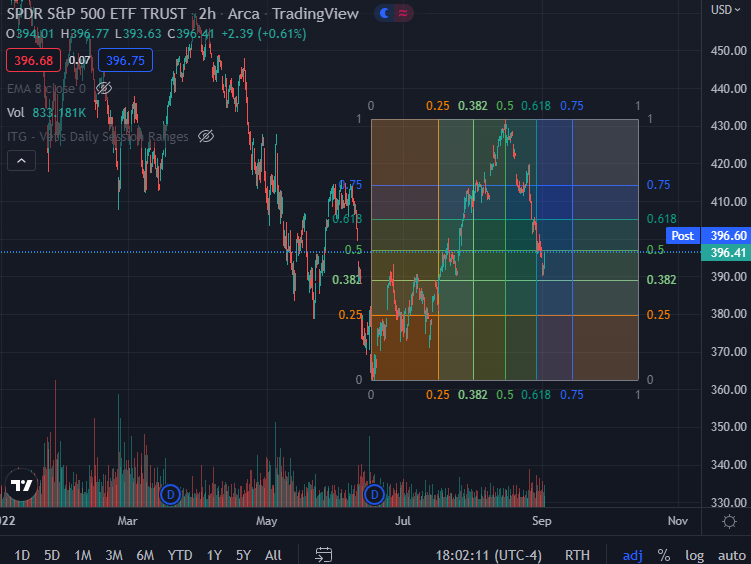

Looking at the color wheel I put up this was expected to be a strong bullish movement from the market and that’s what we’re getting. When looking at SPY today I’m watching 400, 405 and 410. I like $5 intervals personally. If there’s major resistance at any of these levels I will begin to position for the downside for two weeks out.

The U.S. added 315,000 jobs last month (down from last month) beating average economist estimates of 298,000 jobs. Unemployment up a small bit to show some slowing and slowing from last month. After comparing to previous month and the market already dropping all week, think we see sideways or stay fairly green today if this keeps up and no major news, which I would not think we see any. Could also explain the runup yesterday and major buying right before close. So should be green then.

Rounding out the week for those keeping score we predicted downward momentum yesterday that would be short lived followed by recovery which was spot on. Then today we predicted green followed by a selloff which again was spot on.

Heading into next week admittedly the selloff was stronger than would’ve been anticipated, however, I’m not 100% convinced it’s due to any particular change in market sentiment and think it’s likely more related to the “risk-off” behavior we’d all thought was likely earlier this week. In perfect Valhalla we’re not bears or bulls but instead some strange bull/bear hybrid so I don’t honestly give a flying fuck if this is real or not so the game plan is to wait until next week when additional data drops on Monday to see how the market is reacting and position accordingly.

Should the data point towards inflation easing I would still expect the market to react bullishly as it did earlier today, should that change our strategy will definitely change accordingly.

Wanted to stir up some convo about what the market is reacting too and also what is going to change sentiment.

Looking at this it seems like the market is pricing in words and not actions. We are still in a bearish sentiment from Powell’s speech and that seems to be the overall feeling of what’s going on. There’s a lot of people watching the fed rn and it’s all speculation at this point.

Kinda feel like we’re heading towards that $380 mark within the next couple weeks maybe a bounce back to 400 but still in a down trend. Looking at the daily chart Ill be seeing if we hold that level

What happens when we get there. Sept 20th correct? Feels like we’re pricing in the fed coming in hot. If that happens I don’t know that I see this going too much farther down and we may see some reaction to something other that Powell to drive sentiment. Possibly a nice little climb from SPY after with good or bad news and maybe have that change is sentiment that the worst is behind us.

Also looking to break the top of this downtrend after that date.

I’m always bias bullish and I’m trying my best to be non bias. I’ve sold a couple of the rips on spy in the last few days viewing this as more overall market sentiment rather than events that drive that sentiment.

Again, I think this is a small window where the market is reacting from words and not actions.

The selloff started a bit before but I definitely think that the amount that was sold off could have potentially been related to the gazprom news. With that said however, gazprom news really hasn’t been seemingly affecting the markets very much since then.

For those confused by the price action today I would certainly suggest circling back around and re-reading the balloon analogy. While it’s become somewhat infamous now you can see it at work easily when combined with our analysis of market sentiment the last few days as it related to news/data coming out.

By understanding what the market has priced in and how it prices in additional news we’ve been able to somewhat accurately predict daily movement before it happens. As stated yesterday:

10AM numbers have landed BEARISH. They show a slight increase MoM which is not what the market is looking for in its pursuit for evidence that inflation is easing. This wasn’t a huge jump so again we’re probably looking at a quickly priced in scenario but based on our strategy of playing catalysts we should be out of these trades quickly anyway.

Once that bearish data was priced in (quickly) we’d reached “baseline” where most all the bearish news of the current cycle was priced in therefore today the market was able to resume it’s normal state of floating upward. I’ll elaborate more on this in the near future but what is essentially going on is likely a combination of dip buying and covering as a “near term” bottom has been reached. That buying will likely continue to some extent until the next time you have a bearish catalyst and the “balloon string” is pulled.

Spy/Qqq are currently touching the 200MA again. last time was on august 26th. the last time JPOW spoke and spy was at the 200MA it got rejected and had one hell of a drop. JPow is speaking tomorrow right before market open. spy is at that 200MA again. lets see how this plays out. im thinking spy gets rejected and finishes the week out super bloody. but it all depends on what is said tomorrow. we are still looking at a super bearish trend.

As I looked back on market the last few days or weeks since the balloon thesis seems to be a very accurate depiction of the current times. Bad news that may not even be that bad air out of the balloon. Good news maybe not great news sometimes the balloon floats a little more sometimes it doesn’t.

But no news and as I’ve seen stated many times the balloon is naturally going to rise. Definitely something I will continue to keep an eye on. Seemingly everyday without something utterly important we are drifting upward. So no catalyst to either direction seems to be buyers market.

Not sure where to add this… but several reports coming out RE her Majesty’s [US] worsening health conditions. we’ll see how the US markets react to this…

As if we did not have enough confounding factors in the mix already, QT also kicks off in earnest this month, with this week providing clues as to the potential scale of its impact.

Sep is when the Fed is scheduled to take QT to max pace - $95B is expected to run off, of which $60B is in Treasuries and $35B is in MBS. (We had been doing half that these last three months.) This is expected to shave off a cool $380B from the $8.8T of Fed assets.

This week is important because bond auctions and MBS auctions happen mid-month. The Fed will not engage in purchases of bonds and will greatly reduce the purchase of MBS. This reduced demand from the Fed should be reflected in the bids these auctions attract.

As with most things, opinion is split on whether this QT will matter.

The “will matter” group basically makes the case that “QT will matter because QE mattered. And the effect will be inverse QE - .” Liquidity is already thin in the markets, so we should see yields rise sharply.

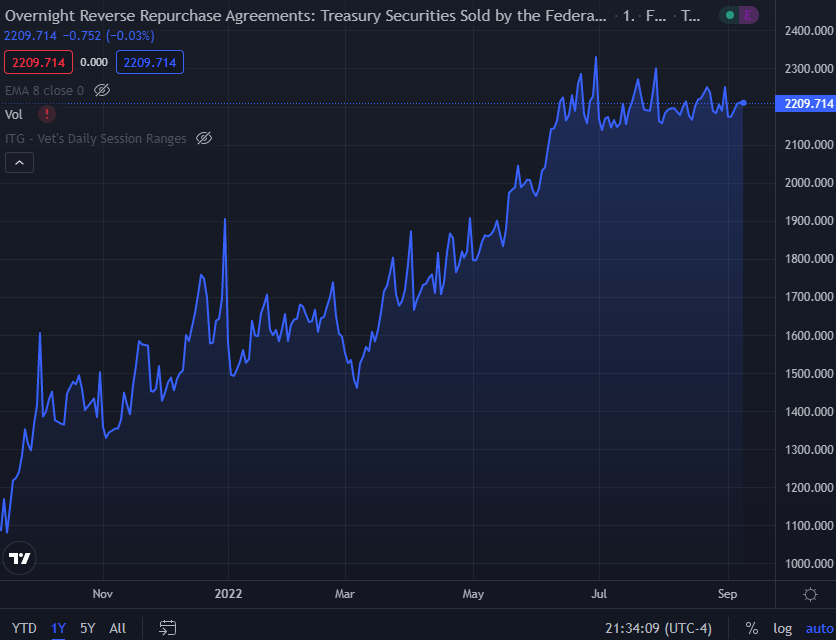

The “won’t matter” group point out that the reverse repo market is still a bloated 2.2T, with no signs of being drawn down despite half-QT having been underway for a few months already. They expect markets to respond with a .