Historically, major declines have happened right after VIX was low, and high VIX typically marks bottoms (in fact, VIX typically peaks right at the bottom). The reasoning for this is relatively straightforward. Low VIX means there’s not a lot of people hedging so demand for options is low (eg. people are exposed and complacent). It also means that there’s more gamma exposure on the MMs who sold these low priced options. So when the negative news does come out, there’s a rush to hedge positions and/or sell off. Whereas if everyone’s well hedged, there’s not a lot of panic selling that occurs.

I would keep an eye on this, if VIX goes down even more before Friday’s CPI release, a negative surprise could cause a huge move.

But at the same time, we have a very large 06/17 options expiry with 3.2 trillion expiring. Doesn’t this conflict with the low VIX idea that people are not hedged? Seems like the opposite is true? But then idk why VIX is so low.

Was watching a YouTube video and saw this graph about an indicator that has been correct at calling a VIX spike the last 9 times or so. Idk what the indicator is because I couldn’t find it on tradingview, but it seems something to do with bonds. From this graph (indicator at top, SPIP middle, VIX bottom), it seems like VIX is about to spike.

This does make sense at the broader picture too because more puts are flooding into the markets again, a huge bearish divergence on SPY, VIX is failing to close lower again, and fear about CPI data next week and FOMC 2 weeks from now could cause a massive sell off - increasing volatility.

Might add this into my thread later, but looking at volume profile, there’s basically no volume until the 393 area on SPY. There is some volume at the 407 - 405 range, but beyond that, it just seems like a free fall to 397 and then most likely buying at 393. This will prob change as time goes on, but interesting to note now that we broke below the huge volume area above the 411 range. This lines up about more volatility incoming as we could just see a freefall starting Monday.

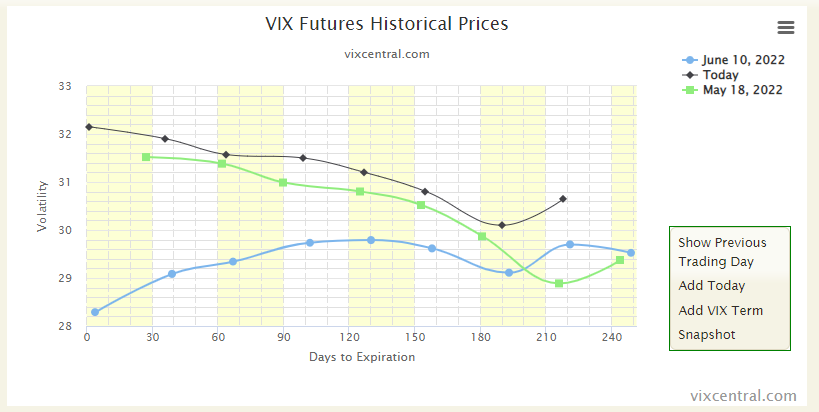

There is a prevailing sense that the market is rather well hedged now, both with puts and with VIX calls.

VIX technically isn’t supposed to be able to be pinned the same way as other tickers are, but when enough money is at play… It’s happened before, and the CBOE has adapted calculations at least somewhat as a result of this.

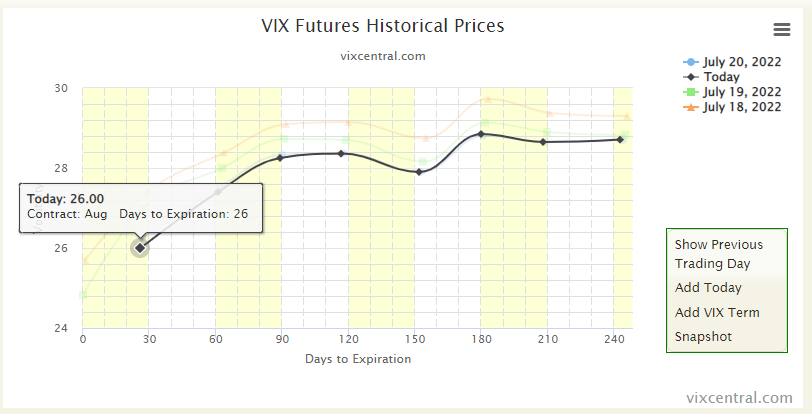

VIX currently being at 25 puts it in the middling area of where it’s been the last few months. ~25 has worked as both support and resistance in the past.

While I do think the market will continue to decline, I don’t like the idea of trying to time a spike on something decaying extremely quickly.

Earnings season is coming up but I think we’ll see more modest declines of 10-20% on things instead of a bunch of -50% blowouts on earnings. The news will likely be bad for a lot of growth companies, but their valuations have come down to fairly reasonable levels now.

The priced-in CPI projections to be released next week are also on the high side IMO:

With expectations this high it’s very easy for the numbers to come in lower than expected next week.

Main takeaway was, yes vol is low because everyone is hedged to the gills.

However, over time people get complacent, and that hedging dies away. Especially if market is moving up.

That is when vol, as measured by the VIX, shoots up. When folks are not hedged as much, anymore.

He also notes that while VIX is pretty steady because of how it is measured off of SPX options, the underlying stocks are quite a bit more volatile. Something not evident from the index itself.

UVXY buy orders for $12 hit; holding now. Not getting calls, not just because VIX is down, but because VVIX - vol of vol - is at historically low levels:

I bought about 1K worth of ATM VXX call options today, expiring in about 3 weeks. I’m thinking that the next GDP release will be negative, putting us into a recession and potentially catalysing the next leg down in the bear market.