One thing though… VVIX - vol of vol - is picking up a bit. We also had a day last week where VIX was up when markets were up, and no one seems to know why. Will keep an eye on this for now.

For now, continuing to hold the UVXY commons (that are bleeding out ever so slowly due to roll over). No options. Waiting for the sleeping giant to awaken.

UVXY call spreads filled yesterday - just noticing it now.

Wide 15C/25C for Jan 2023 for $1.

That we damped out after 1 day of fall, massive put levels are expiring tomorrow, and there is little support now below 3800 seems to suggest that we could have some toasty vol events in the next few months.

Have set 1/2 to sell at $2, will ride the rest.

Btw UVXY rollover loss seeps into options too, so VIX calls are also a way to play this.

The volatility gods are restless today. I’m assuming a large part of this is event vol related to the PCE release tomorrow, with a bit of British shenanigans thrown in.

This then implies that there will be a major vol unwind tomorrow, once PCE is known. Hence have closed out of all UVXY positions noted above. That includes both the call spread and sizeable commons positions, for 25% and 18% respectively.

Expecting to reenter into UVXY sometime in October, as vol should flare up again into the midterms. Assuming Putin or Kwarteng don’t kick the beehive some more, first. Will scale in as VIX goes back to the low 20’s.

Thank you, sir. I bought commons a few weeks back because of this thread and then bought calls the last couple of days.

Was going to hold onto the commons and let an option run but deferring to your brilliance I am all cash (and green!) from the UVXY trades. Very grateful for the trade ideas

And haha yeah… vol can die faster than a fish out of water in the Sahara. There’s midterms, and then should be some “main event” vol explosion in Q1-Q2 2023… so we’re just getting warmed up.

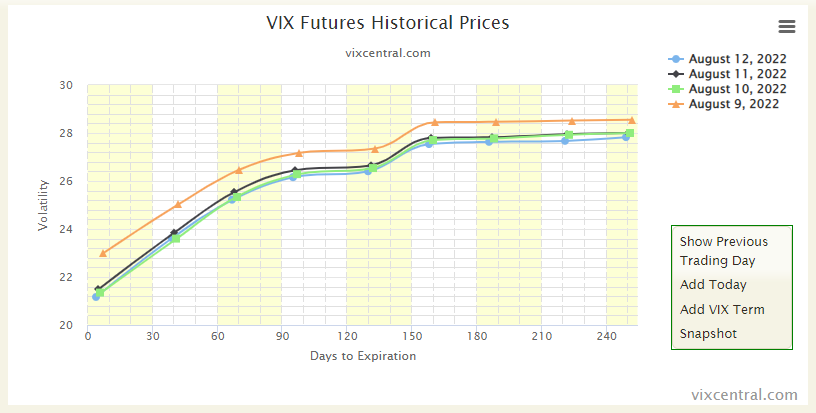

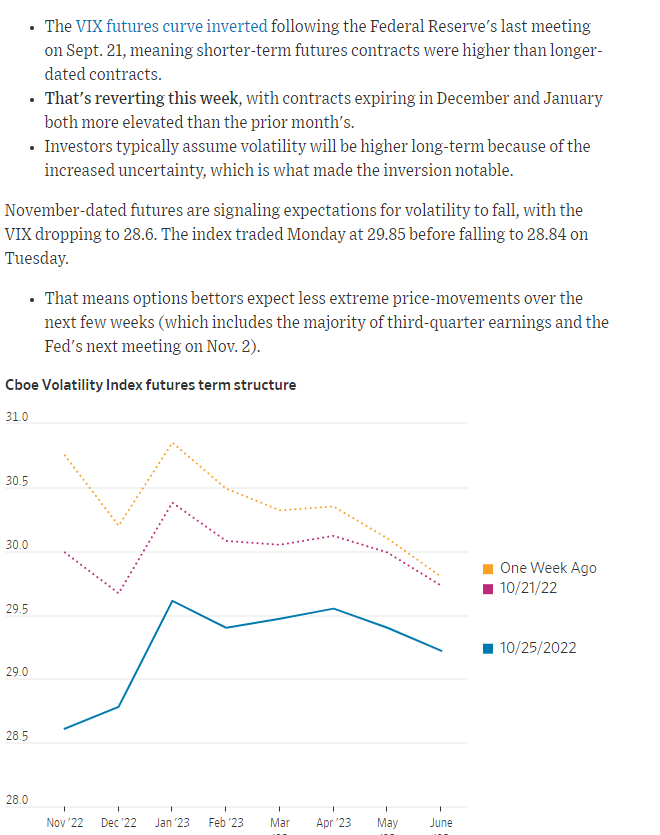

Unlike last week, the entire term structure seems to be elevated. In other words, markets expect bad things to happen “soon” but its not clear how soon “soon” is.

This is probably some combination of CPI next week, the Brits barely keeping their financial sector together with duct tape, and Putin and his tactical nukes.

One other reason to keep an eye on this - we are sitting under a ton of puts. Any reduction in vol will make MMs dehedge, and the resulting vanna rally will be glorious.

Folks have been “long vol” (i.e. expecting stuff to blow up) for months now, and nothing is happening. Institutions are no longer taking those bets to the same degree, and hedge funds that relied on this long tail event are running out of runway.

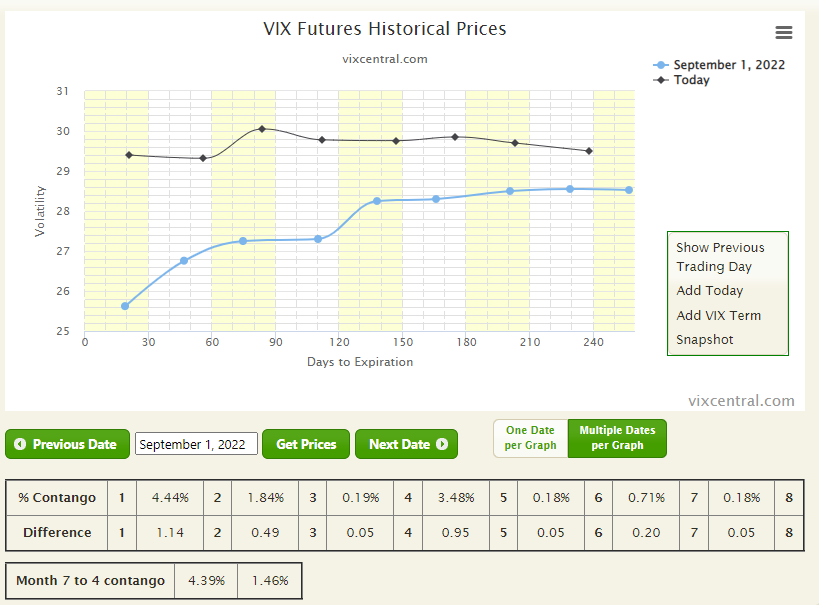

You can see the weird funk we’re in by comparing the vol structure with about two months ago (no significance to the date):

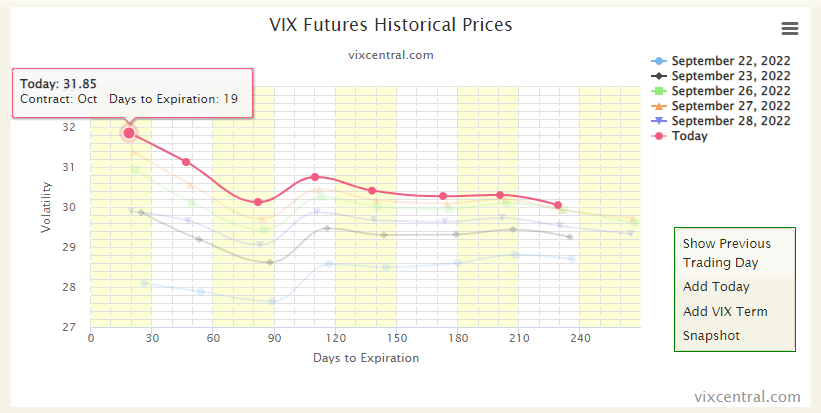

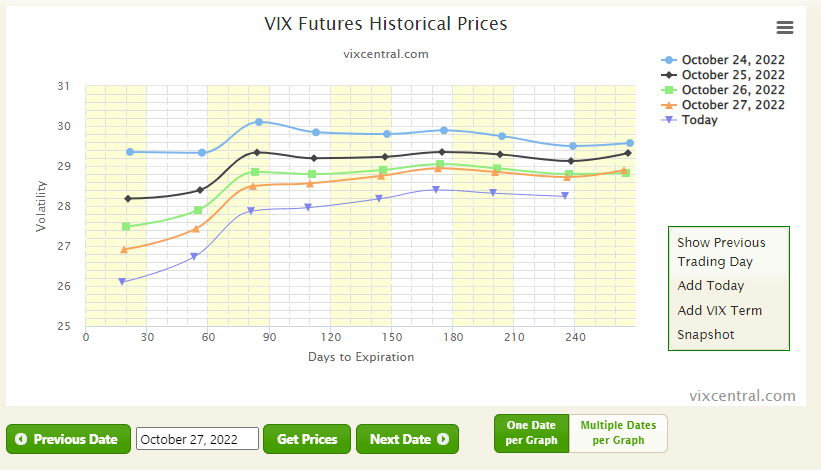

Volatility is falling off a cliff (Images 1 and 2). Presumably because a lot of it was tied to earnings, and less so to FOMC and midterms. Both the bond and stock markets seem to be quite positive. Yet it’s not like we actually have good news on the inflation front, and the Fed Whisperer is sounding rather pessimistic. So going to start building some protection.

Got:

UVXY commons at $9.93

10/18 10C/12C call spread at $0.36/ea - this is risky, as vol could keep falling into midterms

Also setting up additional buy orders for UVXY commons at $9 and $8.

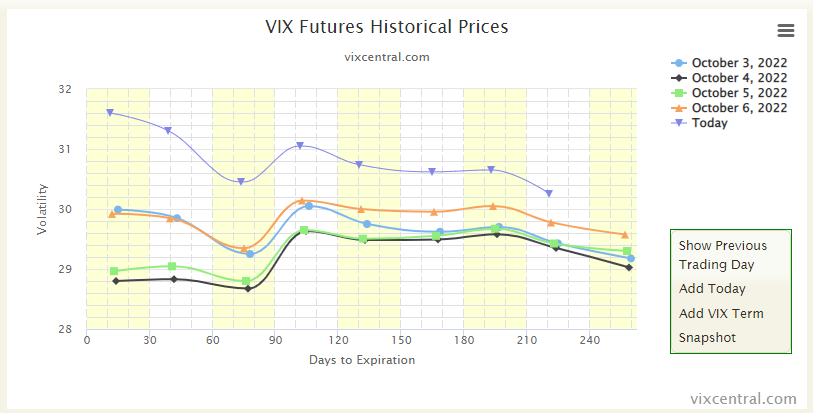

Note that like all leveraged ETFs, UVXY suffers decay (Image 1 vs 3). So $10 now doesn’t represent what $10 represented even a month ago.

There should be vol unwind after the election results are known, will load up then for Dec or Jan expiries on the cheap, unless vol remains high on account of CPI Thu.

Another masterclass from Cem Karsan. Main takeaway - puts are disappearing as people get complacent, but also, puts are providing less by way of protection as VIX is much lower. So once market starts gliding down again and people realize puts are not protecting them to the downside as much, they’ll start selling more to get out. Setting up a feedback loop of selling.

This is all to say that the market is not expecting any bad surprises in the near future whatsoever. This is bullish. If CPI is anything close to what is expected - a high 5-handle - we might be looking at a nice setup for a nice bull run.

Will play next week with this bias in mind.

Now… this is also the perfect setup for things to unravel very quickly when a shock happens, so I did get Aug '23 VIX call spreads just in case we wake up one day to find something really big went bump at night. It will keep its value for months, and will make it more comfortable to partake in bullish plays overall.

On the Eve of FOMC, all is super quiet in vol land. Term structure is appreciably lower across the board, and this is reflected in VIX and VVIX. (The very recent uptick is likely due to FOMC, and likely to fall even more, barring some shock.) MOVE (the bond index) has also not been this low since June, suggesting bonds are not feeling my uncertainty either. This may be a good time to start considering long dated VIX call spreads.

“Volmaggedon” and the impact of 0DTE options has become all the rage after JPM’s chief global market strategist dished out some good old-fashioned fear mongering spree yesterday. Markets seldom do what consensus amongst “chief strategists” and the like suggest it has to do. Nevertheless, sharing these two resources that note some of challenges that 0DTE has brought to the markets: