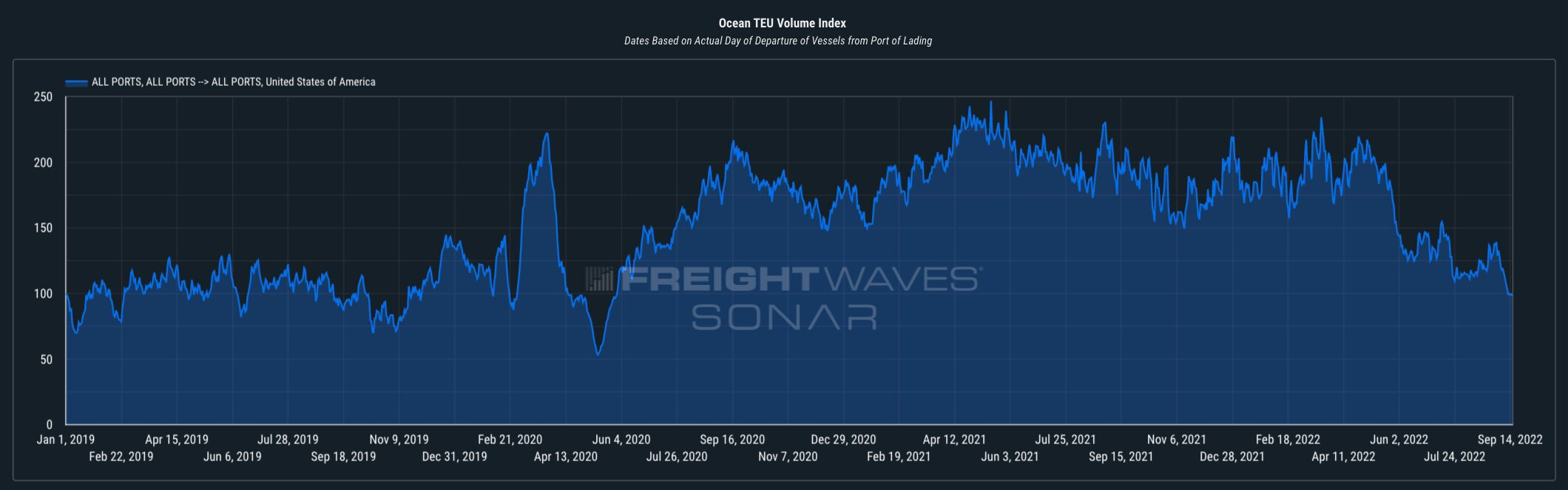

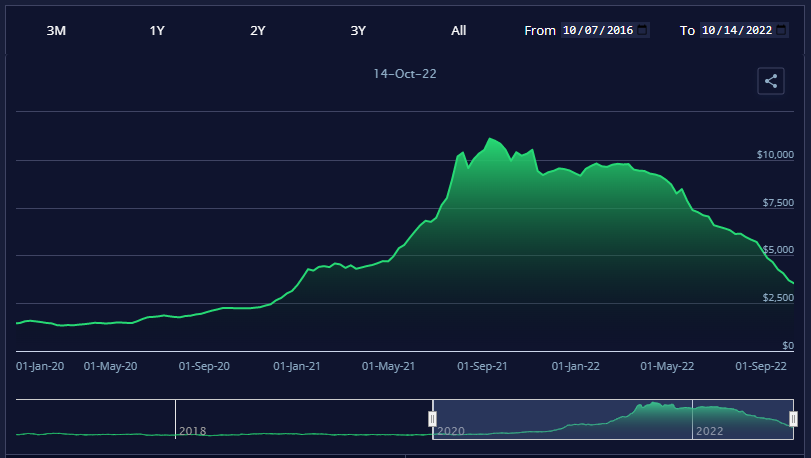

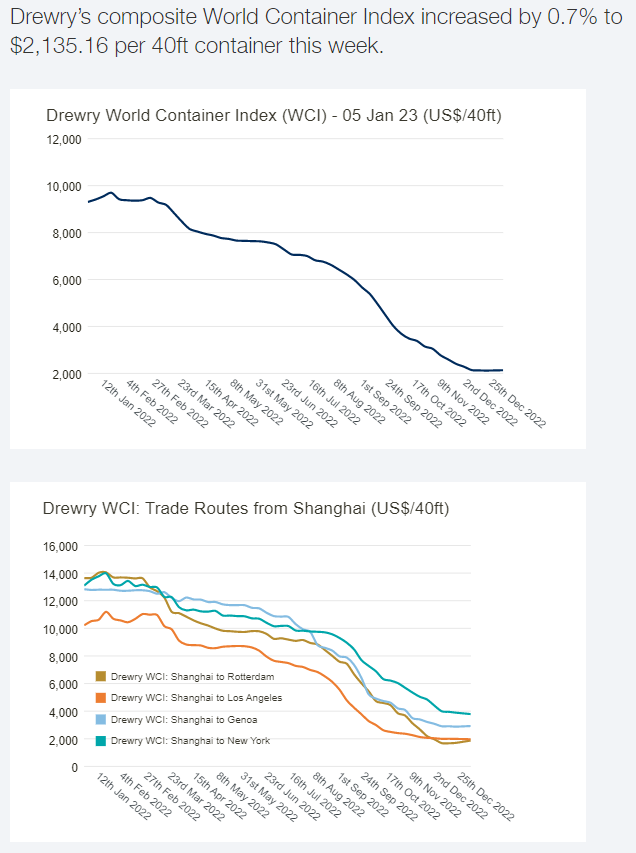

Container freight bound for the US (leaving port of origin) have now dropped below summer 2019 levels. It will take a few months before this shows up in US import numbers, but the outlook is very negative (note: this is supposed to be peak season).

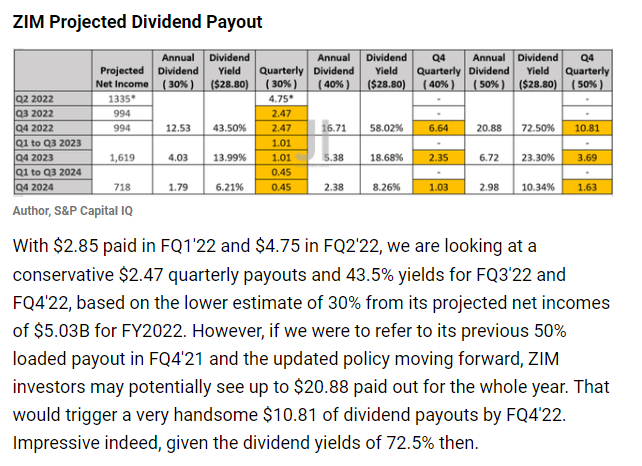

ZIM is expected to pay out $13.28 in dividends still, in Q3 and Q4. About 1/3 of that for Q3, and the remaining in Q4. That’s a 54% return in two quarters, and > 100% yields in annualized terms, given the current price of $24.87.

There is no real support here, so will just have to let it fall until it stops.

ZIM is out of its doghouse, but its not clear if it’ll fly yet. Will wait till end of next week to initiate a position, as CPI will determine the market, and ZIM will likely move with the market as much as anything else.

Just a quick update on ZIM - even though it’s outside its “window of weakness” and we are approaching earnings, it looks like this time is different. Reason is weaker container-based movement, as noted by @TheMadBeaker above, and as reflected in the freight rates (below), which are still falling.

Q3 dividend would have been modest, so staying out of this trade for now. If ZIM reaffirms guidance for 2023, then we could revisit this play again for Q4 earnings.

ZIM’s share price remained a slave to falling container fright rates, and showed very weak pre-earnings appreciation. Dividend was $2.95 for Q3, which is still quite respectable considering a $20 share price.

Am still expecting a nice make-up dividend in around March 2023. Was supposed to be around $10, but given macro conditions, ZIM might hold on to some more cash. Still, a $5-$8 dividend on a $20 stock is very nice.

Having said that, not going to double down on the position I have in commons. There seems to be this one-month wide window of weakness after dividends are paid. Ex-dividend date was today, so we’re probably looking at weakness into Jan 2023. Will consider loading up some more, then.

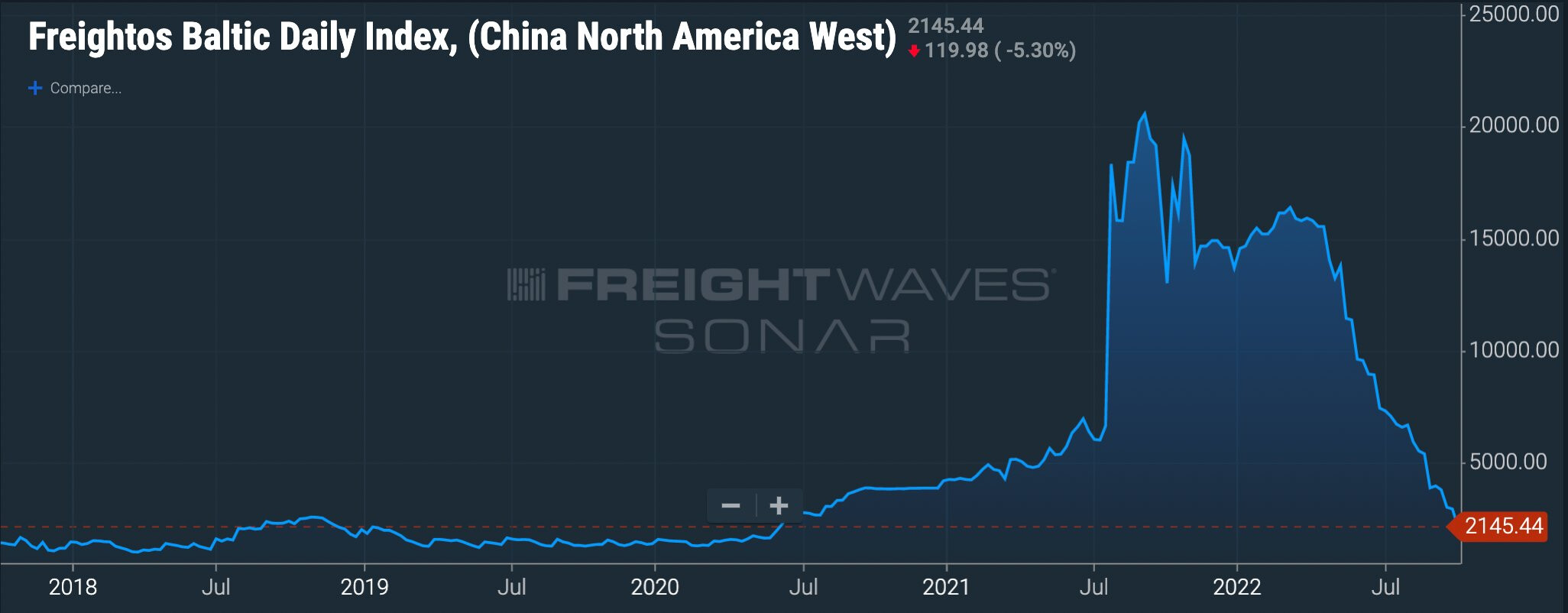

The one confounding factor could still be freight rates. They are at pre-pandemic levels already and port congestions are no longer a thing, so hard to see how they get “worse” for the stock, but this gives us another month to keep an eye on things before considering a play for the Q4 dividends that will be paid out in Mar 2023.

Incidentally, you’ll see articles quoting ZIM dividend yield at 50-150% - these are all looking at the past, and the future will decidedly not look like that. This March dividend is the last remnant of a very, very good time we are unlikely to see in a long while.

Making no changes current holdings. Will update right after New Years.

This may give us a window of opportunity to go long to capture the dividend bump. Recall that the dividend was anticipated to be around $10 until Q3 results came out, but even if it is a bit lower than that, it should result in some price appreciation given the stock price is $17 now (!).

Still a little early as next earnings are 2 months out, but initiating positions in case China reopening affects container rates too:

Sold 4/21 $12.5P for $1.50. Interestingly, prices went up today and the put buy order from last week still hit, as IV is going up. If this gets assigned before earnings in March, I’m more than happy to own more ZIM at $11. Otherwise, will play for expiry.

ZIM is curling up now. We’re still 1.5 months out from earnings, but container rates holding, so we could be looking at a bottom. Might see additional movement after Chinese New Years holiday ends next week.

Buy order of $17 hit day before. Sold puts have lost about a third of their value.

ZIM has 30M shares short and seems to be enjoying a bit of a short covering rally. Up 30%+ from recent bottom. No change in container rates, which seem to have bottomed. Complicates the earnings related play a few weeks out.

ZIM earnings are now expected on Mar 8, 2023 - we could see some appreciation during this time as this has happened the last few times during the 2-3 weeks prior to earnings

ZIM bounced off of the 20SMA, which is encouraging

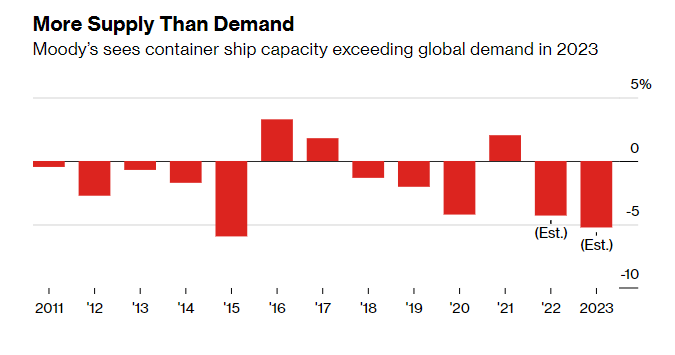

Zim Integrated Shipping Services (NYSE:ZIM) -7% in Monday’s trading after Barclays downgraded shares to Underweight from Equal Weight with a $15 price target, cut from $26.50, foreseeing a global shipping downcycle in 2023-24.

Analyst Alexia Dogani said she believes the container shipping industry is entering a period of “significant oversupply” in 2023-24, estimating capacity will grow by 10%/year while demand is tracking at negative 3% compared with 2019.

Dogani thinks freight rates will go below pre-pandemic levels or, at best, back to where they were pre-pandemic given current trends, which “creates a challenging earnings outlook for the container shipping lines as unit costs are currently 45%-70% above pre-pandemic levels,” leading her to expect “EBIT losses and balance sheet re-leveraging as capex is committed and free cash flow generation is challenged.”

Zim Integrated Shipping Services (NYSE:ZIM) +5.5% in Friday’s trading after J.P. Morgan upgraded shares to Overweight from Neutral with a $30.40 price target, after the stock price has been cut in half during the past six months.

JPM’s Samuel Bland said even after forecasting materially negative cash flow during 2023-25, he still expects Zim (ZIM) will have $2.3B of net cash (ex-leases) at trough, and believes buyside expectations are more similar to his forecasts.

Despite a high level of ongoing lease debt, “we are increasingly confident that the 46 newbuild charters may turn out to be quite competitively priced,” so Bland said he excluded the leases from his valuation, which leaves the stock price looking cheap, although with high near-term sensitivity to any continuing decline in freight rates.

The overall orderbook stood at 7.69 million TEUs as of Feb. 1, just under 30% of the on-the-water fleet capacity, according to Alphaliner.

Of the total, 2.48 million TEUs (32%) was set for delivery this year, 2.95 million TEUs (38%) next year, and 2.26 million TEUs (30%) thereafter.

Most of ZIM’s ships are chartered so it can manage some of this massive margin compression by right-sizing, but with depressed rates, seems like dividends will be under even greater pressure.

Ship owners (like DAC) will deal with this by scrapping. Because of immense demand, scrapping was very slow these last two years, and can be expected to pick up as newbuilds replace old relics. However, it is not expected to be enough to make up for the impending glut.

ZIM earnings are Monday after next (3/13). Price action has been doing what we have expected it to do (Image 1), and should keep climbing at least till Mar 13, when earnings are. And possibly for another week and change, which is how far ex-dividend dates tend to be.

Am looking at touching $26 on or after earnings. Could go as high as $30, which is where I am leaving sell orders.

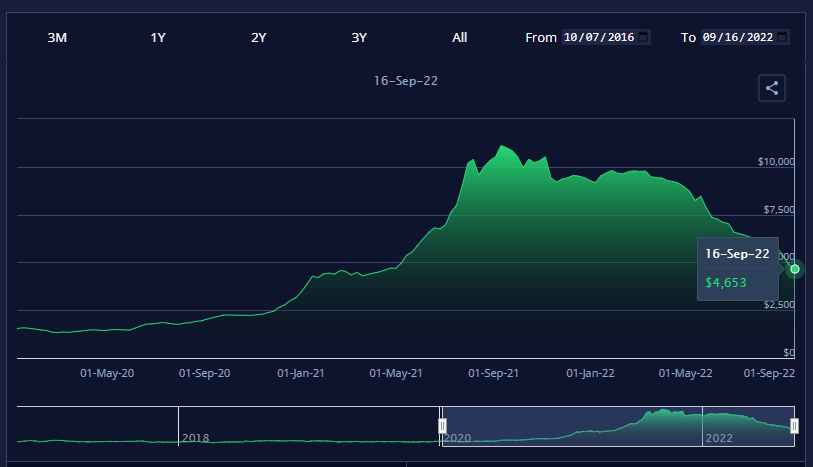

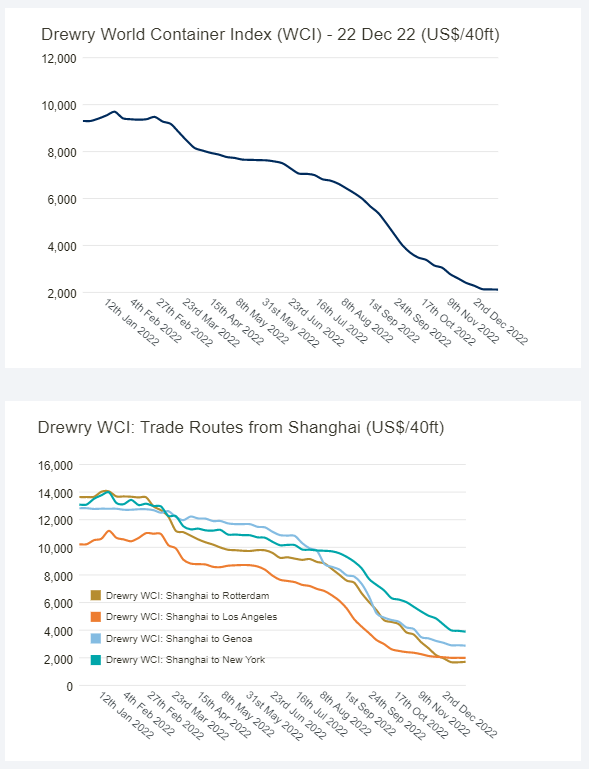

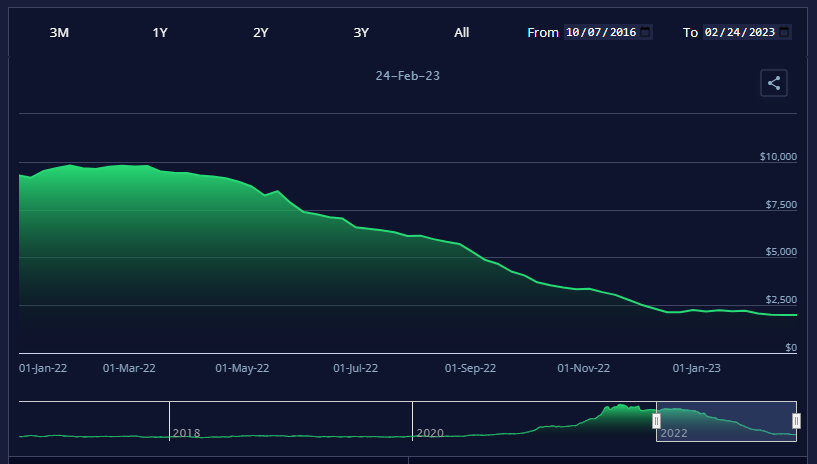

However… all good things come to an end, and ZIM is a slave to spot container rates. Those continue to bottom. (Image 2) I therefore expect prices to revert back to the $17 level, or even lower, in the roughly 30-odd days after dividend payment. Which is the end of April. Once earnings are done, I look forward to loading up on the downside.

Not now though, even though levels are lower than where we are, because IV is jacked. There is much uncertainty on this earnings in particular. ZIM will guide on their blockbuster dividend policy, which is expected to take a hit. And their future plans, around letting leases expire, but taking on LNG contracts etc.

Thus, we can expect ZIM to keep giving for one more round yet.

Nope, this is it. ZIM had very good earnings and guided better than the dour projections from analysts:

ZIM Integrated Shipping Services press release (NYSE:ZIM): Q4 GAAP EPS of $3.44 beats by $1.23.

Revenue of $2.19B (-36.9% Y/Y) beats by $100M.

Adjusted EBITDA for the fourth quarter was $973 million, a year-over-year decrease of 59%;

Carried volume in the fourth quarter was 823 thousand TEUs, a year-over-year decrease of 4%; carried volume in the full year was 3,380 thousand TEUs, a year-over-year decrease of 3%

Average freight rate per TEU in the fourth quarter was $2,122, a year-over-year decrease of 42%; average freight rate per TEU in the full year was $3,240, a year-over-year increase of 16%

Net leverage ratio of 0.0x at December 31, 2022, similar to December 31, 2021; reached positive net cash position of $279 million as of December 31, 2022

2023 Guidance: In 2023, the Company expects to generate Adjusted EBITDA of between $1.8 billion and $2.2 billion and Adjusted EBIT of between $100 to $500 million.

Folks who want to get the juicy $6.40 dividend on a ~$20 stock have to hold into April 4 though, so there’s a possibility for some continued price appreciation.