With all the banking shenanigans occurring I was wondering if there is any potential for a downside play with the recent news of UBS buying out CS. Not only are they buying them out, but the Swiss government is manipulating its laws to bypass a shareholder vote, mainly to expedite the buyout, that’s essentially screwing its shareholders.

The countless Mimir spams on TF and one of the many articles popping out today serve as reference.

Update:

I have seen various conversations on TF talking about the banks and whatnot, but they typically get lost with all the fluff and shitposting AH. Adding tickers discussed on TF.

Deutsche Bank: DB

Swiss Bank: UBS

Signature: SBNY (FDIC takeover)

Silicon Valley Bank: SVB (FDIC takeover)

First Republic: FRC

There are few ETFs as well, but I will list those later.

Sidenote: It was discussed in VC that we have backslidden in our use of the forums and the point was made that this is where catalysts/plays/news, etc. should be posted to provide proper documentation instead of it being lost on TF. I will be spamming the shit of these forums to keep continuity, obviously with pertinent info.

Good discussion on the Think Tank thread in respect to banks. Read from the post above to the most recent.

And this CS one.

Discussed tickers.

[size=4]Individual bank Tickers[/size]

Deutsche Bank (DB)

Swiss Bank (UBS)

Credit Suisse (CS) - UBS buyout in the works

First Republic (FRC)

Ally Financial Inc. (ALLY)

Signature (SBNY) - FDIC takeover

Silicon Valley Bank (SVB) - FDIC takeover

Any thoughts on how you can potentially play this, whether it be short term or long term, are welcome. Saw a couple of you play some calls on the FRC dip and made profit, congrats!

Also, if any of you can provide your take of Powell’s speech and the effects of what it means, that’d be great.

First Republic Bank (FRC) is down about 90% from concerns that it might keel over from the ongoing concerns around upsized deposit withdrawals and bad asset-liability management. It got emergency injection of deposits from other banks, and took loans out from the Fed facility, to the tune of over $100B. After losing > $70B to withdrawals. (Decent smattering of articles on SA, if one wants more details.) The Fed loans need to be paid back in 60 days, which almost forces FRC to come to some kind of arrangement.

Unless something shocking happens, I think it’s a little unlikely that the bank just keels over and dies, at this point. Partly because it has been able to stabilize things, and partly because the Fed really does not want there to be additional contagion. Also could not find anything egregious about its accounting or other dealings, unlike other banks that are struggling similarly.

I see three possibilities, two in the next two months, and one longer term:

FRC limps along and is in a worse state by mid-May, when the Fed loans need to be paid back. The uncertainty punishes the stock price, but doesn’t take it down another 90%.

FRC gets bought out. Maybe by JPM, which has been leading the charge on the bank consortium side to keep it afloat. Earnings are out on Apr 14 so we will know the current book value (i.e. assets - liabilities) for sure shortly. As of Dec 2022, assets were $213B to $195B of liabilities. Current market cap is $2.5B, but it’s entirely possible it has negative book value at this point. So I kinda expect a CS treatment if it gets bought.

Then, there is the possibility that FRC makes it, and comes out on the other side ok. Not back to its glory days, but half way back? Even a quarter of the way there? This will need time though, and we might not know for many months.

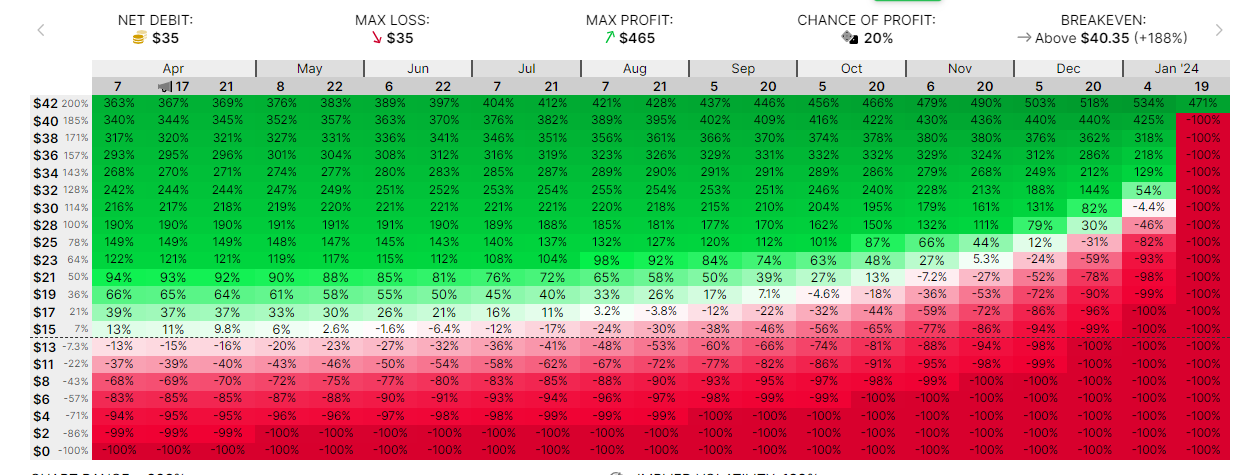

I express these scenarios using spreads as follows:

The puts are 43DTE, the calls are 288DTE. Am assuming that if something bad happens, it happens in the next two months because of the Fed loan trigger. And there’s about equal $$ value in calls and puts.

Btw the 40C/45C might seem a little absurd, but the good news is we can lock in decent profits way before then. For example, $25 by August gets us 180% return.

It’s just that there’s a real chance that price could halve from here or more(second scenario), and breakeven for that play would be over $10, so perhaps a bit too risky for me.

But perhaps am being too risk averse - what do you think?

Hmmm. Tried putting an order for a single put and got an error message. Anyone else getting the same thing? Seems like only share orders are working. Tradestation

I might add it has been designated a hard to borrow status.

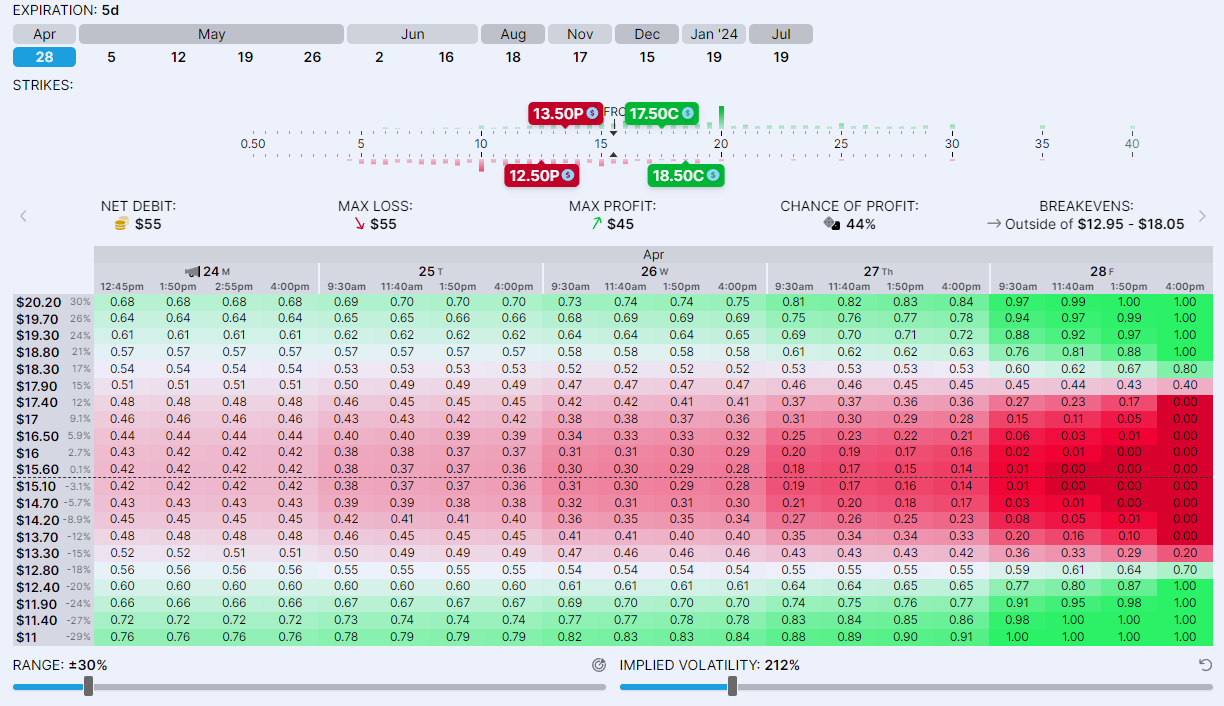

Risky trade, as that is looking for a +/- $3 (~20%) move on $15.50 price by the end of the week. IV is 370% atm though, which suggests a +/- $5 (~32%) move. If this does not materialize, IV crush will obliterate value. Price still moving around a bit and ideally would have gotten it later in the day, but going afk shortly.

Reviewed their financials some more, the gist of it is, they have a $100B hole, backstopped by the govt and $30B of deposits from other banks. Their assets earn less than their liabilities now, so they will also have negative earnings for the foreseeable future. Since a decision seems to have been made to keep it alive as a zombie bank, they could limp on for a while yet. The rational thing to do would be to wind them down in an orderly manner, selling off their assets as much as possible.

Closed the put legs out for $0.80 (+45%). Call legs will likely expire worthless - didn’t feel like wasting commission to close them at a cent or two.

Closed the first out for $0.73, the second for $0.50. Will roll these out a bit.

Various outlets reporting the receivership could be imminent, making this a tricky play in case they shut down overnight. Will have to get broker’s help to get out of this if that happens

Took this still as IV is so fat though that the spread costs only $0.36, while if it craters to near 0, should be able to lock in the full $1 spread. Got 5/5 instead of 4/28 because I might need extra time to unf*ck this with the broker - they are no help if the puts have expired. And used today’s profits from FRC only for this to limit downside.

PacWest Bancorp (PACW)'s earnings came out today, and things don’t look anywhere as dire as FRC:

FIRST QUARTER 2023 HIGHLIGHTS

Net loss available to common stockholders of $1.21 billion, or a loss of $10.22 per diluted share

Adjusted earnings of $89.4 million, or $0.66 per diluted share, which excludes non-cash goodwill impairment, and severance and contract termination expense (non-GAAP measure)

Goodwill impairment of $1.38 billion recorded due to decline in our stock price as a result of recent market volatility. Goodwill impairment is a non-cash charge and has no impact on our regulatory capital ratios, cash flows, or liquidity position

Severance and contract termination expense of $8.5 million accrued related to our efficiency initiative

First quarter results were marked by enhanced liquidity following market volatility

Total deposits increased $1.1 billion to $28.2 billion at March 31, 2023 compared to Company’s most recent update of $27.1 billion as of March 20, 2023. Deposit balances further increased approximately $700 million as of April 24, 2023

Total insured deposits, including accounts eligible for pass-through insurance, represented approximately 73% of total deposits as of April 24, 2023 up from 48% at December 31, 2022

Immediately-available liquidity (on-balance sheet liquidity and unused borrowing capacity) of $12.4 billion, which exceeded uninsured deposits of $8.1 billion, with a coverage ratio of 153% at March 31, 2023

All risk-based capital ratios increased from December 31, 2022, with CET1 increasing from 8.70% to 9.22%

Credit metrics remain steady with nonperforming assets ratio declining 3 basis points to 35 basis points

Unrealized losses on the Company’s investment portfolio improved, declining from $791 million at December 31, 2022 to $736 million at March 31, 2023

They had to get $11B in loans to prop up their $44B balance sheet

$8B in uninsured deposits

Have access to $12B in liquidity - $6B in additional borrowing facility and $6B in cash/cash-equiv

Losses of ($1.2B) were entirely from goodwill impairment of ($1.4B) - likely done so they didn’t need to borrow another $1.4B to prop up the BS, and has the benefit of lowering taxes.

They will still have to cycle out the $5B of the FHLB loans soon, which could cause some stress.

Probably worth keeping an eye one as its down ~60% and could catch a bid.

Closed this out for $0.60 (+67%). Had it at $0.70 for the longest time, but even though FRC fell to $5, the insane IV of > 400% made sure there was enough extrinsic on the $7 short leg to miss that target. FRC is up today to $6.29 atm, and FDIC often acts on a Friday, so decided to close this trade out.

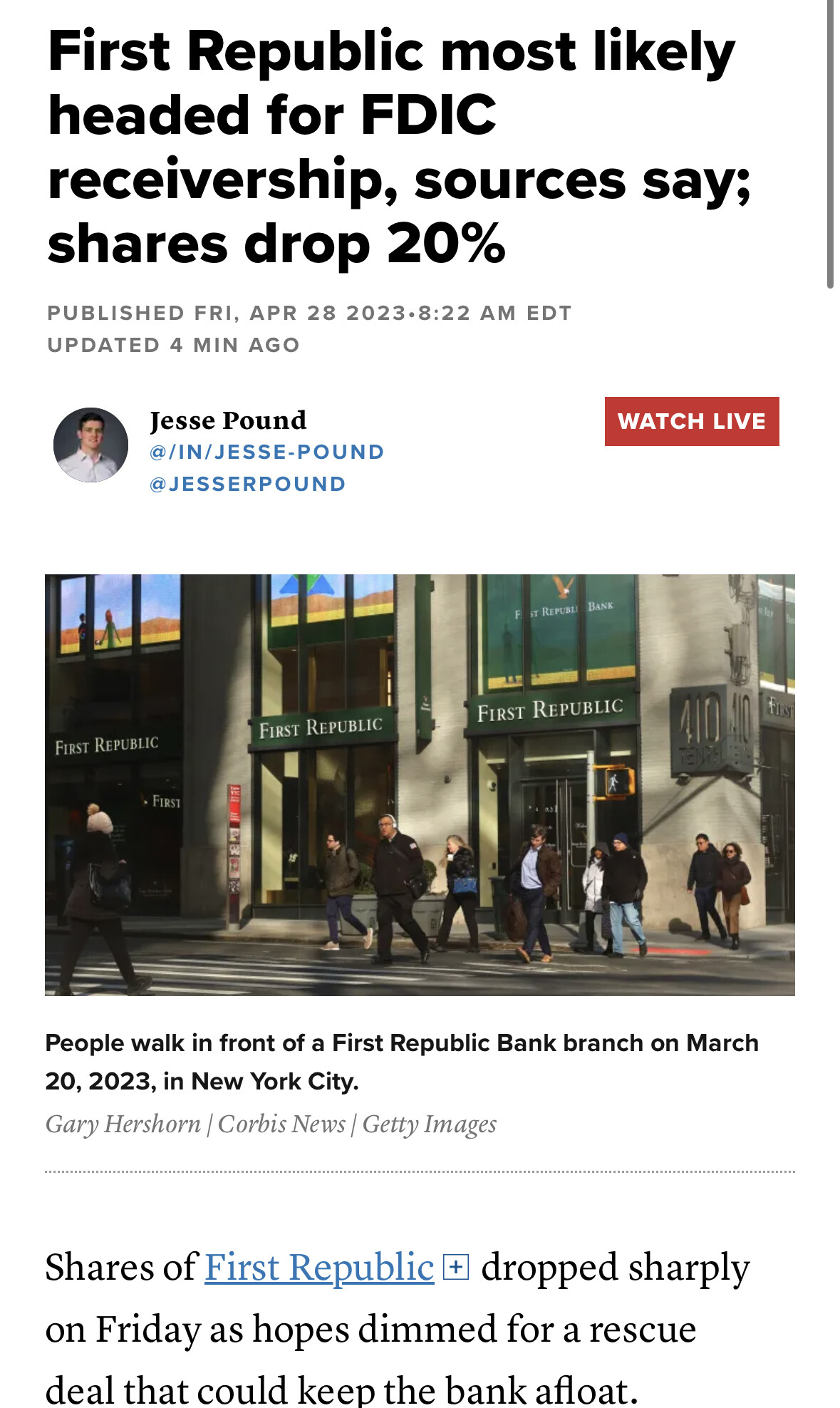

It’s looking more like the rumors will come to fruition.

Wrong link. Cant seem to find the article online.

If you click on the breaking news link when you open it it should take you to the receivership article.