We have had a number of indicators that have played out as expected. We have had months of valuable descussion talking about the risks of a stagflation and recession, most of which came before any financial institution or media outlet started talking about it. I think the case has been made and we are moving quickly in that direction.

What Im currently trying to understand better are what pain points the market has and how are those vulnerabilities express themselves.

One pain point I have been focused on recently is low liquidity. Yesterday was a low volume deep selloff. This tells me buyers are not showing up, this can quickly lead to further selloffs and increased volatility.

I think we test 385 again soon. Bounce and retest 395/400 or break through. Not sure where we will find support after that, but I would expect increased selling pressure.

I still think the travel industry is one of the best targets right now. Currently holding June/July/September positions with my go to tickers:

CCL, DAL, AAL, ARKK, SPY, AND HYG

Will cut most if we re test and break through 395 spy resistance.

What does this have to do with the topic of this thread?

Is this a sign of the economy strengthening, or slowing down?

Will this add to inflation, or take away from it?

I suspect from the “LOL” that this contribution may be better suited in the #community:politics section, but just wanted to offer another opportunity to clarify your views. Thanks!

Found this neat comment on a YouTube video that explains the polarizing effect of the ETF-ization of our current stock market.

For backdrop basically everyone has been encouraged to just buy ETFs, and sure that works great when the fed is printing money and the market is bullish. But what does all this money in ETFs mean in a bear market?

I’ve worried about the ETF effect for years, since it should have the effect of amplifying market movement / trend - to the upside during good times (QE), but also to the downside in bad times (QT). In the past, it used to be that a similar company might be hit in sympathy when a peer reported poor results - guilt by association… but ETFs make the association structural, so that stocks become tethered / bound to each other through liquid ETFs that bundle them together. Then, consider the potential for network effects and feedback loops between various ETFs, since popular stocks may be listed in multiple ETFs. Who even has a full graph of the ETF network of the market? Like a vast spiderweb, a big shock in one area can propagate through the web, via all the ETF’ized connections. One stock could pull one ETF down, dragging down other stocks in that ETF, and those other stocks could be in other ETFs, dragging those other ETFs down along with the other stocks in them. Add stop loss orders and margin calls to the mix, and you have potential for unexpected and unpredictable flash crashes in the market.

Small article about spot shipment rates and how they’re down significantly, but still high. Curious to see what happens as shipping costs come down - will companies lower prices proportionally or keep prices high? Spot rates dropping isn’t universally good either, because we’re still in a driver shortage and if rates are down that’s less money to pay everyone.

Browsing around news etc, this article on REITs came up and made me think of this thread. It’s a Morningstar article with a Morningstar editor questioning a Morningstar analyst, so probably some bias there to say the least lol. But it goes into ‘moats’ for different types of REITs and the sort of balance of give and take needed between these REITs and the larger companies they cover. I’m catching up on the real estate stuff currently so not sure how much of the info is new or actionable, but still, thought someone might find something useful out of this (account walled but free articles, can use a throwaway email if you want…was gonna copy/paste the full thing, but it’s a bit long for that):

TL;DR, the guy’s recommendations are Federal Realty (shopping center trust), Realty Income (triple net lease REIT) and Ventas (Healthcare REIT), though the conversation really seems to be more on the associated dividends. Realty Income looks like it has a monthly payout.

Again, just posted this up as I knew REITs had been being discussed a bit lately, I don’t know a lot about them myself yet, just the basics. After reading the full thread and these articles, I do see their appeal though

After loosing some money playing a reversal that didnt happen I cut my positions and did nothing for a bit. Re assesed, zoomed out, checked indicators.

Big thing I saw was low volume. I have had success playing “relief” rallies based on low volume. If its high volume, it may be a bear market rally, and they will absolutely rip your face off, so it can be risky so I dont make big trades on spy, qqq, or iwm typically. Its usually my losers that had a green day, so I wait until eod and open small positions to hold overnight. If the trend confirms I expand on the positions. Best case scenario it was a relief rally and I can hold these through this trend, but if it starts swinging too much ill have to go back to shorter positions.

I like my basket of losers, looking to add a few new names. If green trend forms in the morning I will cut, but im willing to be patient. If red trend confirms Ill try to find the best entries to add to the same strikes watching IV.

Lots of uncertainty right now in the global financial markets with low liquidity. Unless we see the bullish trend from today continue in the morning, im prepping to retest 385 if housing numbers are weak, which Im betting they will be.

It def feels more like “sell the rip” more than “buy the dip” lately, but one fed member can cange that in a sentence so keep that in mind when you see them on the calander. Unless the market is drilling, Im taking any plans from J Pow of easing monetary policy as a sign to cut any of my put positions instantly. If they go forward with their plans to continue to tighten, then I believe we will be in a recession, Technically we only need to have one more quarter with negative GDP growth to be in a recession, but my opinion is we still have a ways to go. Also started diving into the auto lending world, I think there are definitely some challenges there and prob some plays, Im working on updating some more info on it.

Not really directly to inflation, but the cause of that spike, which is excess of cash in the system, is also contributing to inflation by strengthening demand (haha money printer go brrr). Repo market will get impacted during Fed’s reduction of balance sheet so still should keep an eye on it. Read what I typed about balance sheet reduction here/ read up on 2018 QT’s effects on Repo market for more info.

With earnings coming to an end, thought I’d post the summary of the updated earnings trends (continued from the earnings trends I posted a few weeks ago):

Highlights:

Earnings Scorecard: For Q1 2022 (with 97% of S&P 500 companies reporting actual results), 77% of S&P 500 companies have reported a positive EPS surprise and 73% of S&P 500 companies have reported a positive revenue surprise.

Earnings Growth: For Q1 2022, the blended earnings growth rate for the S&P 500 is 9.2%. If 9.2% is the actual growth rate for the quarter, it will mark the lowest earnings growth rate reported by the index since Q4 2020 (3.8%).

Earnings Revisions: On March 31, the estimated earnings growth rate for Q1 2022 was 4.6%. Ten sectors have higher earnings growth rates today (compared to March 31) due to positive EPS surprises and upward revisions to EPS estimates.

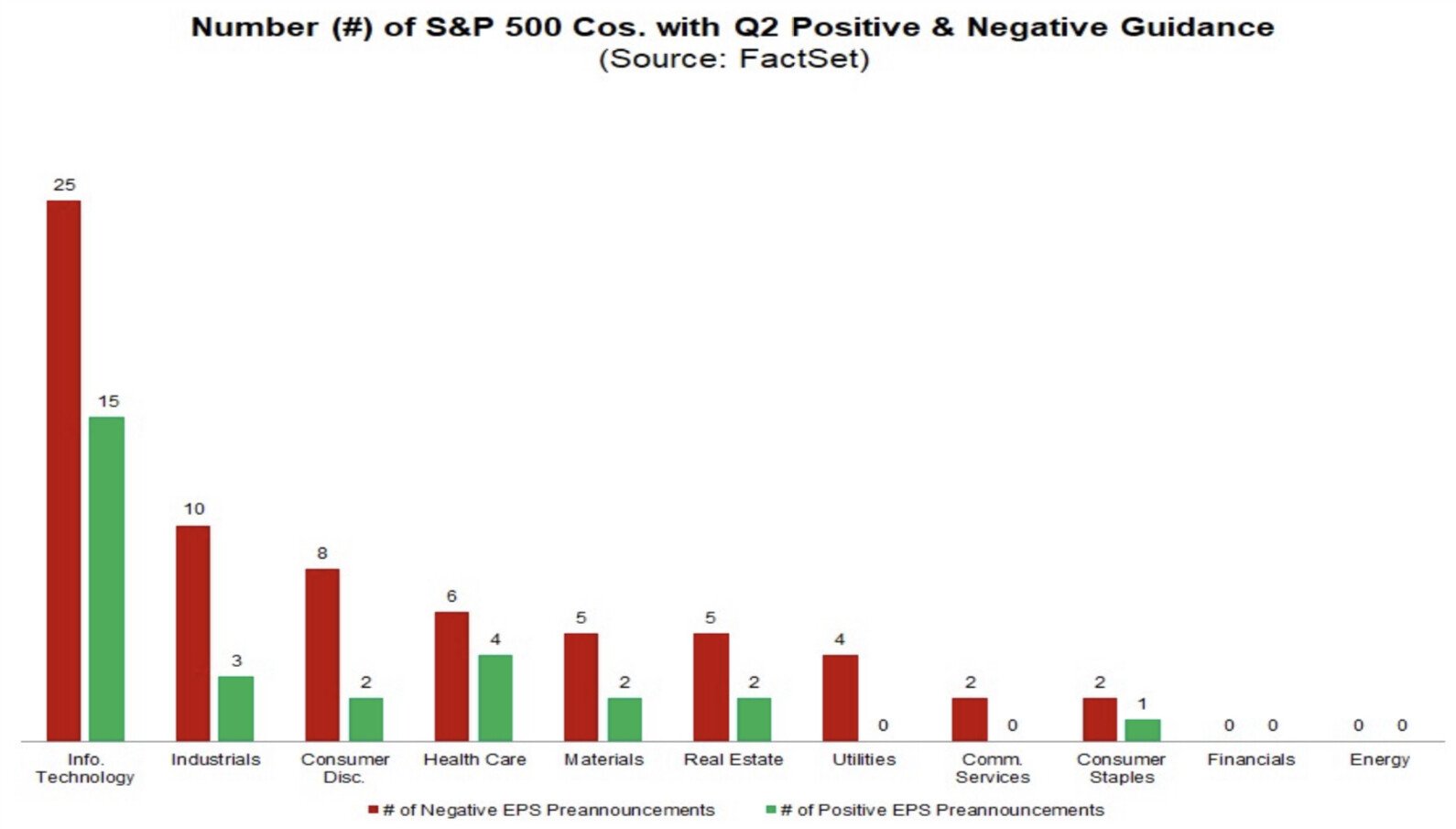

Earnings Guidance: For Q2 2022, 67 S&P 500 companies have issued negative EPS guidance and 29 S&P 500 companies have issued positive EPS guidance.

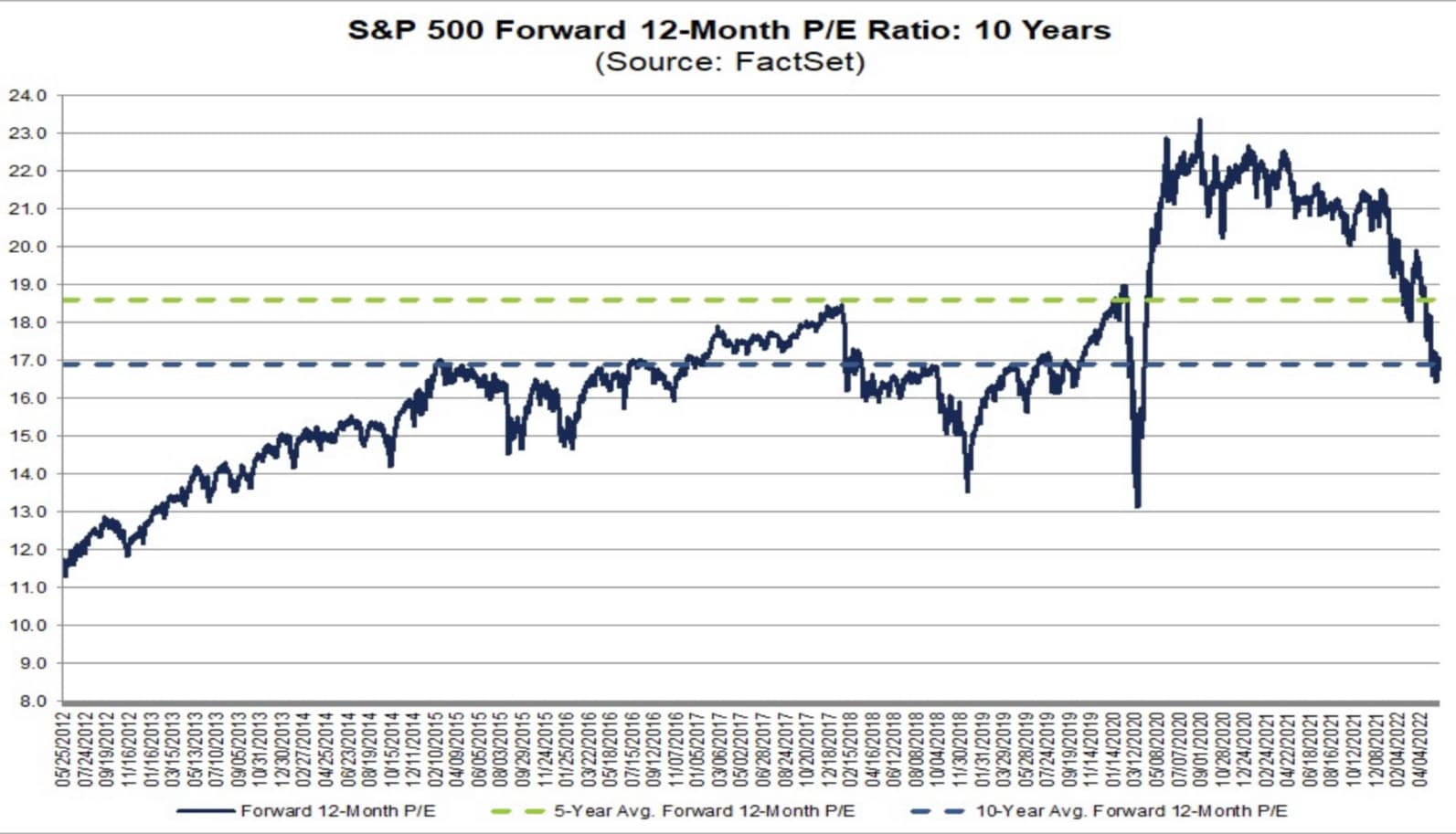

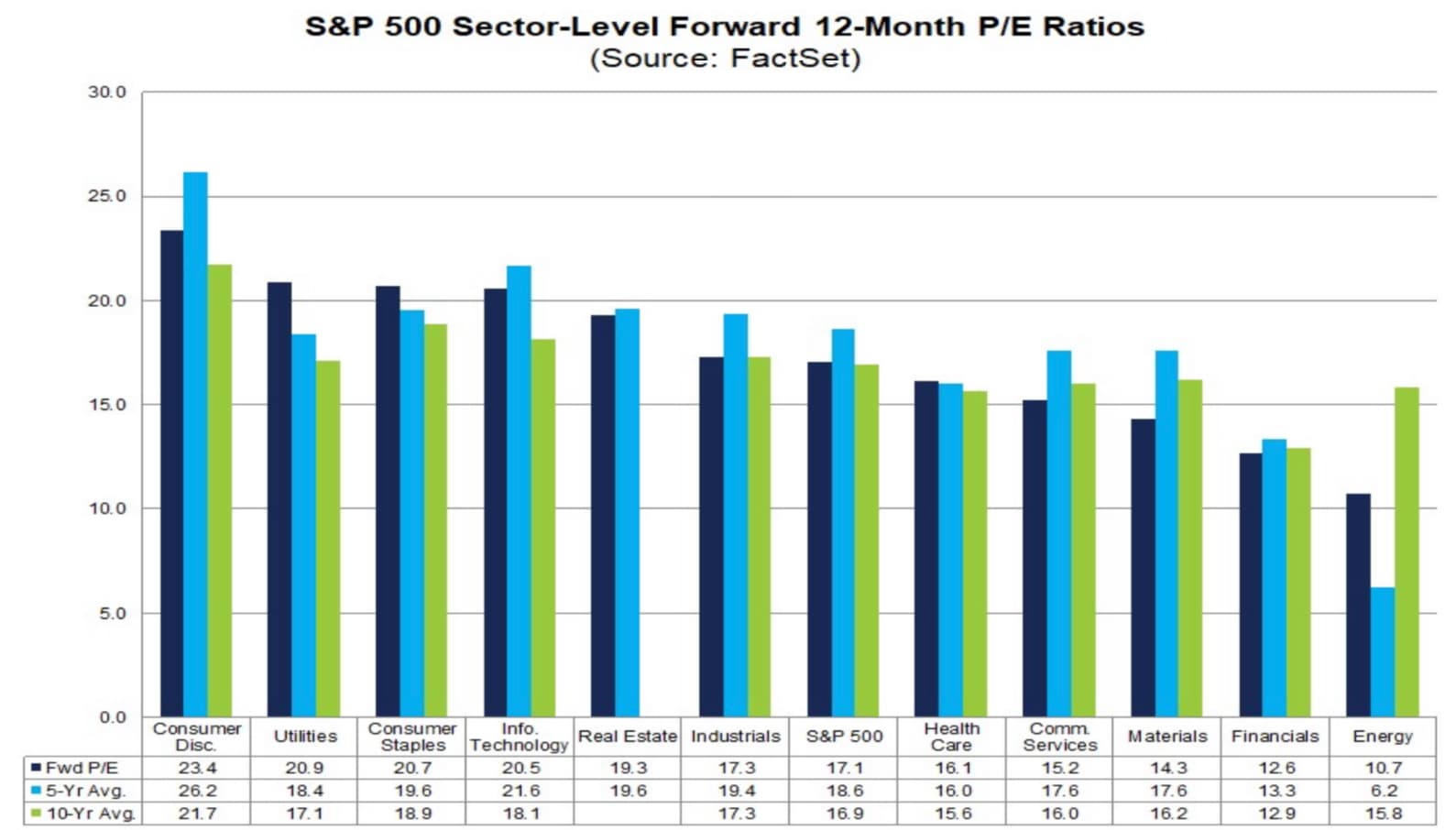

Valuation: The forward 12-month P/E ratio for the S&P 500 is 17.1. This P/E ratio is below the 5-year average (18.6) but above the 10-year average (16.9).

The first quarter marked the highest percentage of S&P 500 companies citing “Ukraine” on quarterly earnings calls going back to at least 2010 at 59% (281 out of 476). By comparison, 85% of S&P 500 companies (406 out of 476) have cited “inflation” on earnings calls for Q1, while 74% of S&P 500 companies (352 out of 476) have cited “supply chain” on earnings calls for Q1.

“As a matter of fact, although we saw a bit of a slowdown focused mostly on Europe at the onset of the invasion of Ukraine, we saw a bounce back and we really exited Q1 with momentum. -Autodesk (May 26)”

Overall, 97% of the companies in the S&P 500 have reported actual results for Q1 2022 to date. Of these companies, 77% have reported actual EPS above estimates, which is equal to the 5-year average of 77%. In aggregate, companies are reporting earnings that are 4.7% above estimates, which is below the 5-year average of 8.9%.

The index is also reporting single-digit earnings growth for the first time since Q4 2020. The lower earnings growth rate for Q1 2022 relative to recent quarters can be attributed to both a difficult comparison to unusually high earnings growth in Q1 2021 and continuing macroeconomic headwinds.

The blended (combines actual results for companies that have reported and estimated results for companies that have yet to report) earnings growth rate for the first quarter is 9.2% today, compared to an earnings growth rate of 4.6% at the end of the first quarter (March 31). Positive earnings surprises reported by companies in the Health Care, Information Technology, and Financials sectors, partially offset by a negative earnings surprise reported by a company in the Consumer Discretionary sector, have been the largest contributors to the increase in the earnings growth rate since the end of the first quarter (March 31).

If 9.2% is the actual growth rate for the quarter, it will mark the lowest earnings growth rate reported by the index since Q4 2020 (3.8%). Nine of the eleven sectors are reporting (or have reported) year-over-year earnings growth, led by the Energy, Materials, and Industrials sectors. On the other hand, two sectors are reporting (or have reported) a year-over- year decline in earnings: Consumer Discretionary and Financials.

In terms of revenues, 73% of S&P 500 companies have reported actual revenues above estimates, which is above the 5-year average of 69% (hehe nice funny number). In aggregate, companies are reporting revenues that are 2.7% above estimates, which is also above the 5-year average of 1.7%.

Due to these positive revenue surprises, the index is reporting higher revenues for the first quarter today relative to the end of the quarter. The blended revenue growth rate for the first quarter is 13.6% today, compared to a revenue growth rate of 10.7% at the end of the first quarter (March 31). Upward revisions to revenue estimates and positive revenue surprises reported by companies in the Energy and Health Care sectors have been the largest contributors to the improvement in the revenue growth rate since the end of the first quarter (March 31).

If 13.6% is the actual growth rate for the quarter, it will mark the fourth-highest revenue growth rate reported by the index since FactSet began tracking this metric in 2008 (These are my own thoughts, but I would guess revenue is being inflated by 40-year high inflation given Energy is the biggest contributor in revenue & earnings growth, per the article). It will also mark the fifth-straight quarter of year-over-year revenue growth above 10% for the index. All eleven sectors are reporting (or have reported) year-over-year growth in revenues, led by the Energy, Materials, and Real Estate sectors.

The blended net profit margin for the S&P 500 for Q1 2022 is 12.3%, which is above the 5-year average of 11.2%, but below the year-ago net profit margin of 12.8% and below the previous quarter’s net profit margin of 12.4%.

If 12.3% is the actual net profit margin for the quarter, it will mark the third straight quarter in which the net profit margin for the index has declined. On the other hand, it will also mark the fifth-highest net profit margin reported by the index since FactSet began tracking this metric in 2008, trailing only the previous four quarters.

Looking ahead, analysts expect earnings growth of 4.1% for Q2 2022, 10.2% for Q3 2022, and 9.9% for Q4 2022. For CY 2022, analysts are predicting earnings growth of 10.1%.

The forward 12-month P/E ratio is 17.1, which is below the 5-year average (18.6) but above the 10-year average (16.9). It is also below the forward P/E ratio of 19.4 recorded at the end of the first quarter (March 31), as prices have decreased while the forward 12-month EPS estimate has increased over the past several weeks.

To date, the market is not rewarding positive earnings surprises and punishing negative earnings surprises more than average.

Companies that have reported positive earnings surprises for Q1 2022 have seen an average price decrease of -0.3% two days before the earnings release through two days after the earnings release. This percentage decrease is well below the 5-year average price increase of +0.8% during this same window for companies reporting positive earnings surprises.

Companies that have reported negative earnings surprises for Q1 2022 have seen an average price decrease of -5.1% two days before the earnings release through two days after the earnings. This percentage decrease is larger than the 5-year average price decrease of -2.3% during this same window for companies reporting negative earnings surprises.

At this point in time, 96 companies in the index have issued EPS guidance for Q2 2022. Of these 96 companies, 67 have issued negative EPS guidance and 29 have issued positive EPS guidance. The percentage of companies issuing negative EPS guidance is 70% (67 out of 96), which is above the 5-year average of 60% and above the 10-year average of 67%.

I think the key aspect is that the insight reinforces the DD that many of us have been stacking in this thread: The cost of revenue is outpacing actual revenue growth.

This seems to be an effect of inflation and worker compensation.

Net profits are decreasing:

If 12.3% is the actual net profit margin for the quarter, it will mark the third straight quarter in which the net profit margin for the index has declined. On the other hand, it will also mark the fifth-highest net profit margin reported by the index since FactSet began tracking this metric in 2008, trailing only the previous four quarters.

What does this lead to? Hiring freezes, lay offs, and rising unemployment. Hint: we are already starting to see this in many companies recently.

My takeaway is this and has always been this: The Fed should raise rates aggressively NOW while they still have a somewhat strong labour market. The longer they stall and delay the inevitable, the more pain they will cause in the future.

Time is running out:

Consumers are dipping into their savings, which are now at record lows, to meet demand to sustain the cost of living. This is terrible. What happens when savings run out?

However this ‘expert’ economist says it’s not a cause for alarm:

Dipping into savings to keep spending isn’t necessarily cause for alarm, says AnnElizabeth Konkel, economist at Indeed. It may even have positive effects for the labor market.

“This recent drop was largely driven by continued negative views on current buying conditions for houses and durables, as well as consumers’ future outlook for the economy, primarily due to concerns over inflation. At the same time, consumers expressed less pessimism over future prospects for their personal finances than over future business conditions.”

“Looking into the long term, a majority of consumers expected their financial situation to improve over the next five years; this share is essentially unchanged during 2022. A stable outlook for personal finances may currently support consumer spending. Still, persistently negative views of the economy may come to dominate personal factors in influencing consumer behavior in the future.”

-Joanne Hsu, director of the consumer survey.

Households Spent More In April, But Used Savings To Do So

U.S. households boosted spending for a fourth straight month in April, but the savings rate fell to the lowest in 14 years, suggesting many Americans are tapping savings to offset cost increases from inflation.

Consumer spending rose by a seasonally adjusted 0.9% last month, the Commerce Department said Friday, with households spending more on services and autos. The savings rate fell to 4.4%, from a downwardly revised 5% the prior month.

“We have finally reached the point where households are dipping into their $4 trillion of excess savings,” said Stephen Stanley, chief economist at Amherst Pierpont.

The Commerce Department said personal income rose a seasonally adjusted 0.4% last month. Adjusted for inflation, disposable income was flat during the month, showing that wage increases are struggling to keep up with price rises and that consumers are drawing on their savings to make purchases.

Spending figures aren’t adjusted for inflation, meaning higher prices constitute part of the picture. When taking inflation into account, personal-consumption expenditures rose 0.7% in April, with durable goods spending up 2.3%, nondurable goods spending up 0.2%, and services spending up 0.5%.

GDP Revised Downward, Worse Than Expected

First-quarter GDP declined at a 1.5% annual pace, worse than the 1.3% Dow Jones estimate and a write-down from the initially reported 1.4%. The pullback in gross domestic product represented the worst quarter since the pandemic-scarred Q2 of 2020.

Downward revisions for both private inventory and residential investment offset an upward change in consumer spending. A swelling trade deficit also subtracted from the GDP total.

Labor Market Still Hot, But Showing Signs of Weakness Possibly Due to Lower Corporate Profits

Initial claims for state unemployment benefits decreased 8,000 to a seasonally adjusted 210,000 for the week ended May 21, the Labor Department said. The decline partially unwound some of the prior week’s surge, which had pushed claims to their highest level since January. The number of people receiving benefits after an initial week of aid increased 31,000 to 1.346 million during the week ending May 14.

Some economists believe the recent increase in applications is due to some retailers laying off workers. High inflation, with annual consumer prices increasing at their fastest pace in 40 years, is squeezing profits.

That was confirmed by a separate report from the Commerce Department on Thursday showing corporate profits from current production fell at a $66.4 billion, or 2.3% rate, in the first quarter, the first drop in nearly two years.

The decline was across financial and nonfinancial corporations as well as overseas operations. After tax profits dropped at a 4.3% rate after rising at only a 0.2% pace in the fourth quarter. Still, profits increased 12.5% from a year ago. Some retailers are still thriving in the high inflation environment.

Contracts to buy U.S. previously owned homes dropped to a two-year low in April, the latest indication that rising mortgage rates and higher prices were dampening demand for housing.

The National Association of Realtors (NAR) said on Thursday its Pending Home Sales Index, based on signed contracts, fell 3.9% last month to 99.3. That was the sixth straight monthly decline and pushed contracts to the lowest level since April 2020, when activity was depressed by COVID-19 lockdowns.

According to the NAR, rising mortgage rates have raised the cost of purchasing a home by more than 25% from a year ago, with the steeper home prices adding another 15%.

The 30-year fixed-rate mortgage is averaging 5.25%, according to data from mortgage finance agency Freddie Mac.

Sales of Newly Built Homes Plunge Over 16% in April

Sales of newly built homes sank to the slowest rate since the start of the Covid pandemic to 16.6% in April from March, far more than expected, and were down 26.9% from April 2021, according to the U.S. Census. The median price of a new home sold in April was $450,600, an increase of nearly 20% from the year before. Slower sales caused the inventory of newly built homes to jump sharply as well to a nine-month supply. A six-month supply is generally considered balanced between buyer and seller.

Mortgage rates, which have been rising since January, really shot up in April. The average rate on the 30-year fixed loan began the month at 4.88% and ended it at 5.41%, according to Mortgage News Daily.

PCE Inflation Report Showing Signs That Inflation Could Be Slowing

The report showed that Core PCE rose 4.9% in April from a year ago. That increase in the core personal consumption expenditures price index was in line with expectations and reflected a slowing pace from the 5.2% reported in March. The number excludes volatile food and energy prices that have been a major contributor to inflation running around a 40-year peak.

The 0.3% increase on a monthly basis was the same as March and in line with Dow Jones estimates. The monthly gain was held back by a decline in energy prices during April that has since reversed.

Including food and energy, headline PCE increased 6.3% in April from a year ago. That also was a deceleration from the 6.6% pace in the previous month. However, the monthly change showed a more marked pullback, with an increase of just 0.2% compared with the 0.9% surge in March.

While the lower level of inflation generated some relief, gas will be a factor again when the May numbers come out next month. Prices at the pump have jumped again in May, surging more than 11% from a month ago and 51% from this time last year, according to AAA (source: https://gasprices.aaa.com)

Durable Good Orders Rose Slightly in April

Orders for long-lasting goods such as appliances, computers and cars rose in April, driven by an increase in new aircraft orders.

New orders for products meant to last at least three years increased by 0.4% in April following a revised 0.6% rise in March, the Commerce Department said Wednesday. April marked the sixth increase in seven months.

Nondefense aircraft and parts orders were up 4.3%, rebounding from an 8.1% decline in March. Excluding defense, orders of durable goods rose 0.3%.

Strong consumer spending has boosted manufacturing demand, despite continuing supply-chain disruptions due to the war in Ukraine and Covid 19-related shutdowns in China, which have contributed to rising prices.

But a pullback in manufacturing orders and output could be coming. Major retailers such as Target Corp. and Best Buy Co. reported slower sales in some categories, which could be a sign that consumers are becoming wary of buying big-ticket items.

U.S. business activity slowed moderately in May as higher prices cooled demand for services while renewed supply constraints because of COVID-19 lockdowns in China and the ongoing conflict in Ukraine hampered production at factories.

S&P Global said on Tuesday its flash U.S. Composite PMI Output Index, which tracks the manufacturing and services sectors, fell to a reading of 53.8 this month from 56.0 in April.That growth pace, which was the slowest in four months, was attributed to “elevated inflationary pressures, a further deterioration in supplier delivery times and weaker demand growth.”

“Companies report that demand is coming under pressure from concerns over the cost of living, higher interest rates and a broader economic slowdown,” said Chris Williamson, chief business economist at S&P Global Market Intelligence.

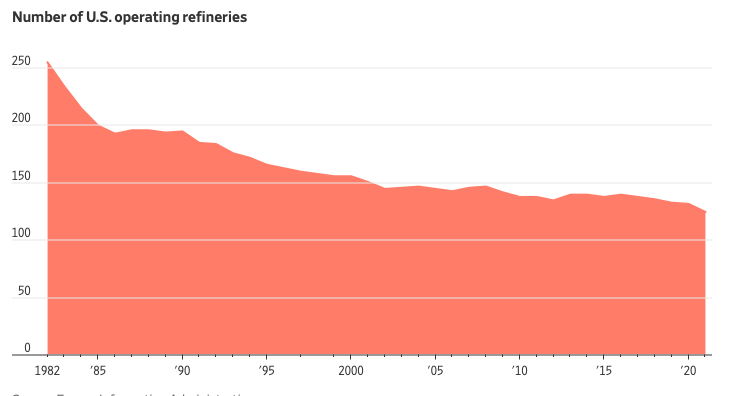

Fuel Reaches Record High Due to Shortage of Fuel Making Facilities

Gasoline prices topped $4 a gallon in all 50 U.S. states in recent days for the first time ever, even though global crude oil prices have pulled back from highs reached during the early days of Russia’s invasion of Ukraine. U.S. oil prices are hovering around $115 a barrel, down from more than $120 a barrel in March.

Higher crude oil prices are contributing to the cost of gasoline, but the primary reason for the record highs in gas prices is a lack of global refining capacity, say energy executives and analysts.

The refining bottlenecks are prompting fears about global shortages of gasoline and diesel. The world hasn’t invested enough in maintaining or adding refineries, leading to huge gaps between the price of oil and gasoline, according to Saudi Arabia’s energy minister, Prince Abdulaziz bin Salman.

Executives and analysts say the situation could worsen because there are no plans to add significant refining capacity, and fuel demand will grow throughout the summer as drivers hit the road and more economies loosen Covid-19 restrictions.

Fed Minutes Show Little to No Surprise

Minutes from the Fed’s May 3-4 meeting, released Wednesday, showed that officials discussed the possibility they would raise interest rates to levels high enough to deliberately slow economic growth as the central bank races to combat high inflation. Highlights from the minutes included:

Most Fed officials back 50 bps hikes at “next couple” meetings

Many see Fed as “well positioned” later this year following tightening

All back plans to begin shrinking balance sheet

All agree economy is “very strong” & inflation is “very high”

US Goods Trades Deficit Shrinks

The US merchandise-trade deficit shrank in April by the most since 2009 as imports fell amid lockdowns in China while exports increased to a record. The shortfall narrowed by 15.9% to $105.9 billion last month, following a record level in March, Commerce Department data showed Friday.

US merchandise imports decreased 5% from the prior month to $279.9 billion, reflecting declines in industrial supplies and capital goods. Inbound shipments of consumer goods fell 7.9% – the most since March 2016 – to $76.2 billion.

Exports rose 3.1% to a record $173.9 billion in April, driven by foods, capital goods and industrial supplies.

The Commerce Department’s report also showed wholesale inventories rose 2.1% in April, while stockpiles at retailers climbed 0.7%.

More complete April trade figures that include the balance on services will be released on June 7.

Microsoft Joins Group of Companies Implementing Hiring Freezes

Microsoft Corp. said it would be reducing the pace at which it hires people for its software group that develops its Windows, Office and Teams applications. The group had been one of the company’s fastest-growing divisions in recent years.

The move is in response to growing economic uncertainties as the company approaches the end of its financial year that goes through June, a company spokesman said.

“As Microsoft gets ready for the new fiscal year, it is making sure the right resources are aligned to the right opportunity,” a Microsoft spokeswoman said. “Microsoft will continue to grow head count in the year ahead, and it will add additional focus to where those resources go.”

Microsoft joins Coinbase, Twitter, Peloton, Carvana, Netflix, Robinhood, Meta Platforms, Uber, Better.com, Scotts Miracle-Gro, and Wells Fargo amongst companies that have recently implemented hiring freezes in some of their divisions.

To me, the news coming out this past week shows that the Fed’s plan is working. I think @The_Ni posted this a while ago earlier in the thread, but now we’re seeing it unfold in real time:

@juangomez053 thanks for sharing, this is a great Q1 recap that will come in handy when we compare QoQ ER in a few months.

@Kevin summarized perfectly our believe that

the “real” economy has been facing headwinds for over a decade such as population and productivity growth cooling (structural drivers) . While Fiscal and monetary policy (cyclical drivers) have been synthetically propping up our markets during this period. We see this in asset bubbles like housing, crypto, equities, Auto, and ofcourse inflation, mainly on non discretionary goods like energy, housing, and food. These are the reasons we believe demand for most goods will effected in a negative way, thus being reflected ER.

"The cost of revenue is outpacing actual revenue growth"

-Kevin

While the financials in alot of cases showed strong revenue, there has been significant increases in cost of goods, labor, and general expenses. This impact to the bottom line forces the equity market to take a more fundamental approach to evaluating companies, while companies need to manage money and growth expectations in a more deliberate way. In some cases like netflix, this means tough descisions.

So a question we should all be asking ourselves is:

Where is the money/demand going to come from that allows companies to post stronger earnings in the near future?

We have seen unprecidented credit expansion that is coming to an end while real wages decline. It appears Americans simply have less money to spend because they are spending more money on goods and services.

As Kevin pointed out, saving rates are near all time lows, but Ill also add that credit card usage is at an all time high. You dont have to be a math wizard to see this is a painful combination. This amplifies the effect of inflation because now american families will be paying credit card bills on top of their already shrinking discretionary income.

I have many opinions about the fed and their responsibility to the American people to keep inflation under control. That is after all one of only 2 mandates the fed is supposed to be responsible for, but to put it simply, I believe they are still not doing enough. And historically outside of the extreme Volker moment in the late 70s, this is just business as usual.

I believe we are currently in a stagflation environment, and that will eventually lead to a recession. Timing since the beginning of this research has always been the hardest variable, but I think we can assume as of now that Q2 earnings generally speaking will be a little more painful than this last round.

If you got some time to lend your ear, they cover a lot of good touch points for the way ahead. Daniele seems to think the recent drop is not the one we are looking for.