I thought this was a good read. And fitting to the context. Also @TheHouse good to see you as always!

But the magnitude of deterioration in the labor market is likely to disappoint investors, says strategist

Investors in the U.S. stock market will be watching Friday’s jobs report closely with a hope that any signs of

weakness in the labor market could give the Federal Reserve more room to go easy with its next interest-rate hike in two

weeks.

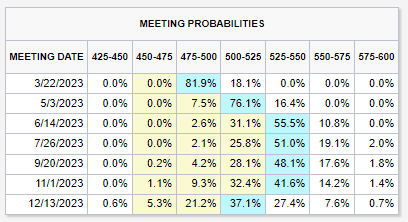

Investors currently expect the Fed to re-accelerate the pace of rate hikes at its March 21-22 meeting, which could

lift the terminal rate above the 5% to 5.5% level officials had forecast in December. The views deepened after Fed Chair

Jerome Powell’s semiannual monetary policy testimony before Congress earlier this week.

Powell said Tuesday that the central bank may need to raise interest rates higher than expected in response to recent

strong economic data, while emphasizing that monetary policy decisions will remain “data dependent.” A day later, he

said no decision has been made on the potential size of interest-rate hike in March.

Powell’s comments put more focus on a flurry of economic data due between now and March 22, which includes Friday’s

February jobs report, next week’s consumer-price index, and updated readings on the producer-price index and retail

sales.

See: Want to know the precise number of jobs that would push the Fed to hike by 50 basis points? There isn’t one.

Investors hope a “softer” employment report on Friday could alter monetary policy expectations and get the Fed to take

a lighter touch in raising interest rates.

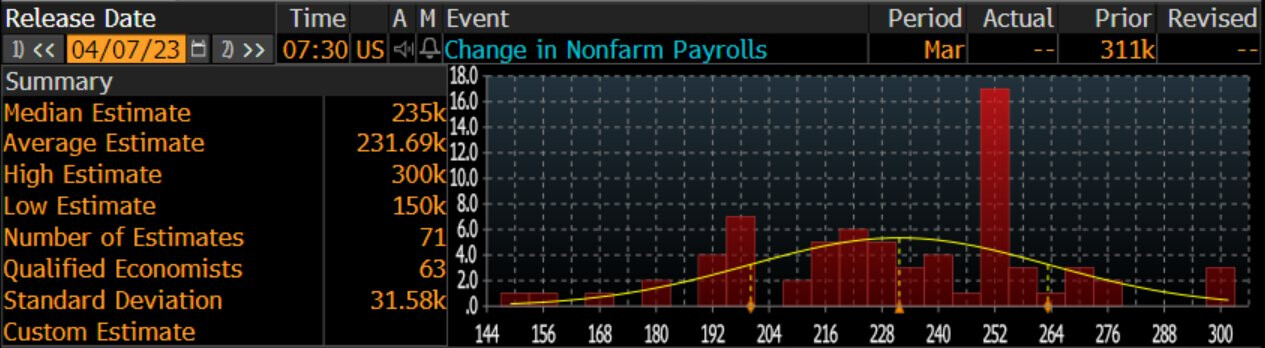

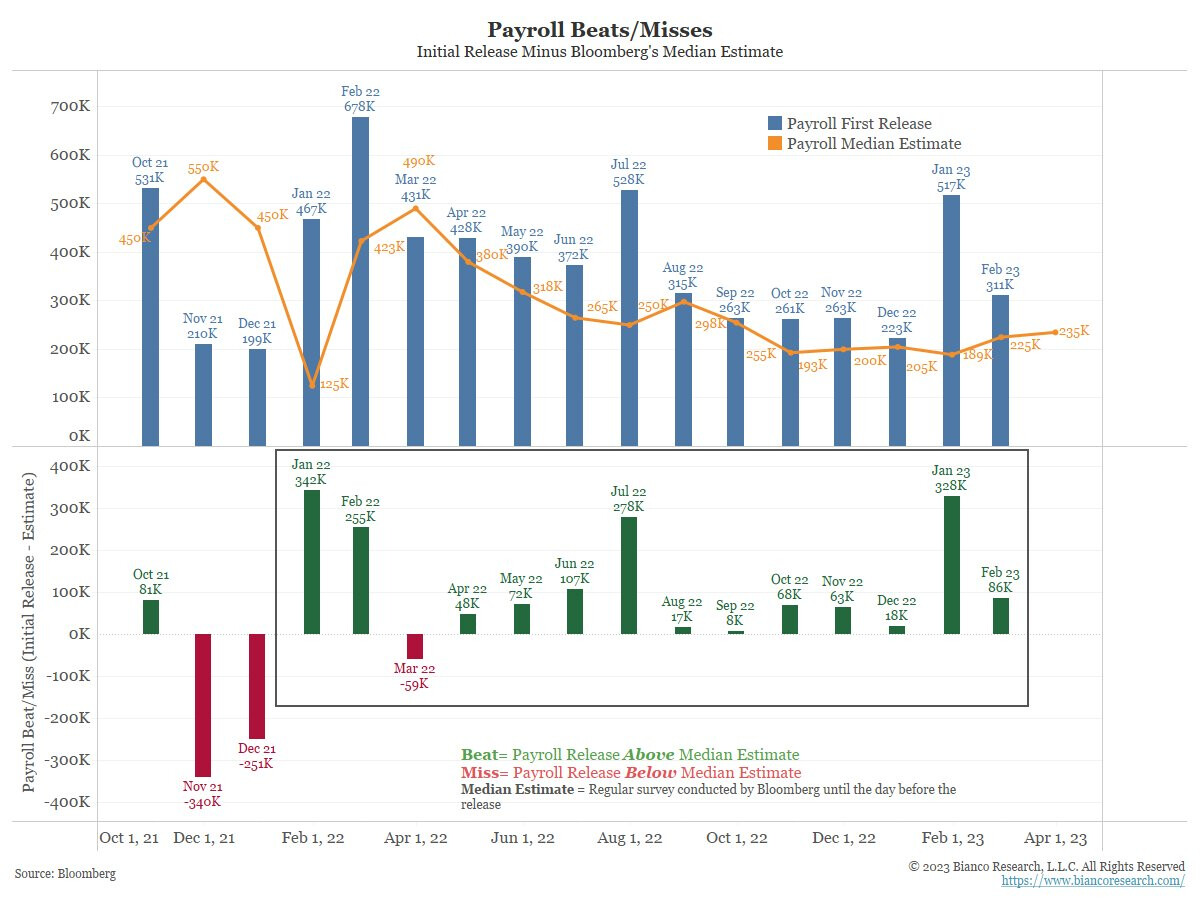

The U.S. economy likely added 225,000 jobs in February, according to economists polled by The Wall Street Journal.

While such an increase would be historically strong, it would mark a slowdown from an originally reported 517,000 spike

in employment in January.

See: Big U.S. jobs report for February could decide size of next Fed rate hike. Wall Street expects 225,000 gain

“The potential for a ‘soft’ jobs number or cooler inflation trend can work to reset the narrative into the upcoming

Fed meeting. We see a good chance of those two indicators surprising to the downside,” wrote Dan Victor, an associate at

Posto Asset Management, in a Thursday note.

“In this scenario, stocks could get a boost higher as interest rate forecasts roll back with a confirmation of the

disinflationary process and evidence the Fed’s policy strategy is working.”

However, Victor said the problem stock-market bears face is the challenge of reconciling a view that inflation is re-

accelerating, while also predicting economic conditions to collapse. That juxtaposition comes into play with the

upcoming jobs report because any signs of slowing job gains could undermine the view that the labor market is still too

hot, as a core inflation driver.

Meanwhile, the magnitude of deterioration in the labor market might not be large enough to alter the rate consensus or

even reset market policy expectations, said Sven Schubert, head of macro research of Vontobel’s Vescore Boutique in

Zurich, Switzerland.

“We already see signs that the labor market is softening. Quit rates, for example, those people that are on their free

will leaving the labor force, are dropping to a two-year low,” he said. “We have already seen a softening in wage

growth, which is still not in line with the 2% inflation target by the Fed, but it’s indicating that we are close to the

peak, maybe passed it already,” Schubert told MarketWatch on Thursday.

U.S. stocks finished sharply lower on Thursday. The Dow Jones Industrial Average slumped 543 points, or 1.7%, to

32,254. The S&P 500 shed 1.9%, while the Nasdaq Composite dropped 2.1%.